HYZD

Interest Rate Hedged High Yield Bond Fund

Published January 22, 2026

Head of Investment and Fixed Income Strategy

Although U.S. money and bond market ETF yields have returned to what is considered to be historically “normal” levels, investors are still looking to utilize a “plus” component within their fixed income ETF portfolios. Oftentimes, leveraged loans, or bank loan ETFs, are deployed to achieve this objective of generating more income outside of one’s core holdings. However, WisdomTree offers a quality-screened solution in this space for investors to consider.

By definition, bank/senior loan ETFs are typically considered to be in the high yield fixed income bucket and consist of a floating-rate structure—in other words, a high yield solution that mitigates interest rate risk. Enter the WisdomTree Interest Rate Hedged High Yield Bond Fund (HYZD). This potential substitute for bank loan ETFs offers a very similar profile for investors, i.e., a high yield “plus” solution with limited—or, in HYZD's case, no—duration.

However, this is where the similarities end. HYZD is designed to provide a quality solution outside of the investment-grade space, where fears of default can be a major concern. Indeed, in the investment-grade sphere, downgrades are the main concern, while in the high-yield world, defaults are the primary risk. HYZD uses a filter where free cash flow (FCF) serves as the credit risk mitigator while also employing equity momentum factors. The remaining bonds are then given a liquidity score and tilted toward issues that exhibit favorable income characteristics.

Additionally, HYZD uses a professional approach that combines these long positions in high-yield corporate bonds with short positions in Treasury securities to target zero duration on a monthly basis. This helps investors reduce their overall duration at a minimal cost to yield.

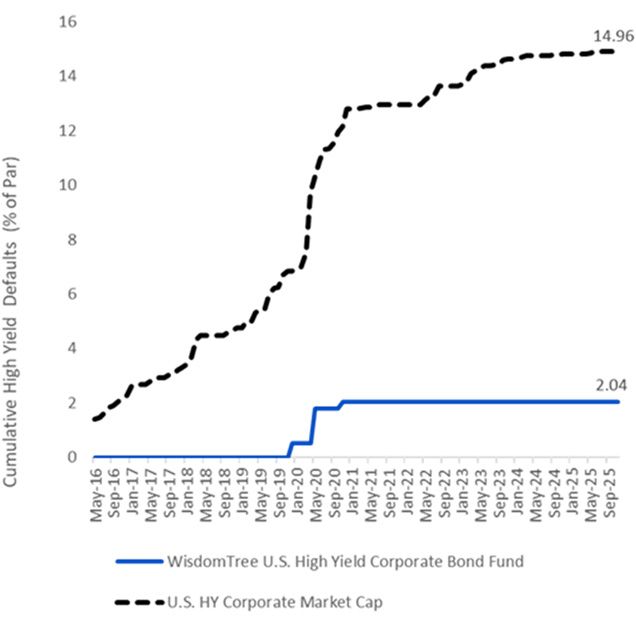

The results essentially speak for themselves. As shown below, HYZD has been able to considerably lessen the risk of defaults compared to the high yield market capitalization measure over roughly the past ten years (cumulative high yield defaults of nearly 15% for the broader market versus only 2% for HYZD).

Source: WisdomTree, for the period 3/31/16–11/30/25.

Another key difference is that bank loan ETFs tend to have less diversification, with holdings concentrated in just a few sectors, while HYZD uses the broader high yield market and spreads exposure across different sectors. In addition, last twelve-month free cash flow data show this key metric is trending lower and has moved into negative territory for bank loan ETFs. Remember, free cash flow is the primary quality-screened factor for HYZD.

For investors looking to add income potential to their core bond ETF portfolio, HYZD provides a quality-screened substitution to the very large bank loan ETF space.

There are risks associated with investing, including possible loss of principal. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. The Fund seeks to mitigate interest rate risk by taking short positions in U.S. Treasuries (or futures providing exposure to U.S. Treasuries), but there is no guarantee this will be achieved. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions.

Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. The Fund may engage in “short sale” transactions where losses may be exaggerated, potentially losing more money than the actual cost of the investment and the third party to the short sale may fail to honor its contract terms, causing a loss to the Fund. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Interest Rate Hedged High Yield Bond Fund

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.