The Stock Market Threw Its Interest Rate Rules of Thumb out the Window

Published April 18, 2022

Jeff Weniger, CFA

Head of Equity Strategy

Something in the market changed about a half-year ago. A dandy old “truism” that had made the rounds for ages got scrapped.

It used to go something like this:

If interest rates are going higher, you should underweight value stocks because that investment style includes large amounts of “bond proxies” like Utilities and Consumer Staples. As rates rise, their dividend yields will lose appeal compared to the income on offer in bonds. You should come back to value stocks only when you think bond yields will fall.

There was just one problem with the old rule of thumb: it didn’t work.

The Fed has, for the better part of a generation, held short-term interest rates at or near zero. The situation has not been much different for longer-dated paper. The 10-Year Treasury note walked into the global financial crisis with a yield north of 5%. Its downtrend persisted for years, slipping all the way to 0.53% during the pandemic. Yet none of that amounted to a hill of beans for value stocks—the investment style has been pummeled by growth in that time.

So much for the old bond proxy rule of thumb.

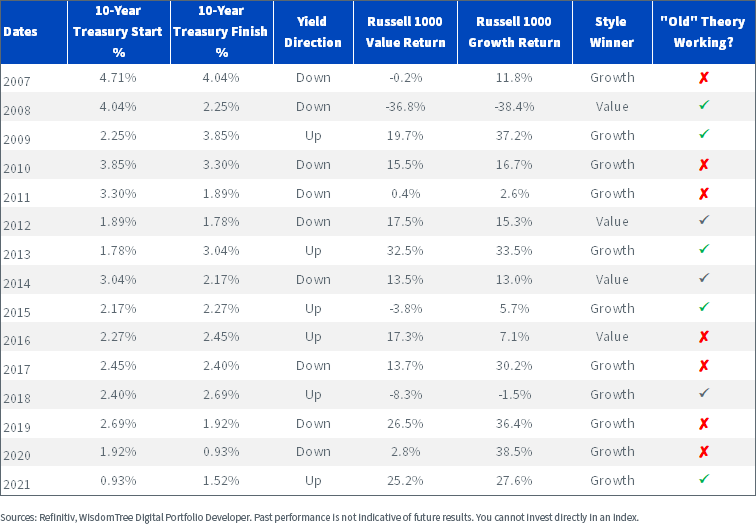

A glance at figure 1 draws only one conclusion, as far as I’m concerned: there has been no relationship between interest rates and the growth/value decision in recent years (figure 1).

Figure 1: Effect of 10-Year Treasury Yields on Value vs. Growth

For definitions of indexes in the chart above, please visit the glossary.

The old rule of thumb needed to die…and die it did.

The catalyst for the market’s change of heart seems to be the inflation scare, which has given rise to a new rule of thumb:

Rising interest rates will be bad for growth stocks because the appeal of such stocks lies in cash flows that will come many years down the road. Because the Fed was expanding its balance sheet all these years, interest rates were held artificially low, flattering the net present value of those distant cash flows. As a new, higher rate regime commences, growth stocks will struggle and value stocks will outperform.

Abracadabra: no longer are rising rates bad for value. Instead, they’re bad for growth.

What we have here is a case of John Maynard Keynes’ beauty contest. The famed economist once postulated that winning in markets was not a matter of identifying the most beautiful contestant in the pageant. No, your success instead lies in your ability to identify the contestant the judges will find most beautiful.

As far as things stand right now for the judges—the collective—it’s all about the discounted cash flow thing.

The market’s #1 rule right now:

Rates Up = Value Good, Growth Bad

Rates Down = Value Bad, Growth Good

I’ve been pinpointing the “top” for growth relative to value as having occurred on November 19, 2021, the day the NASDAQ Composite peaked at a level a shade above 16,000. The index slipped below 13,000 in March and caught a little rally in recent weeks that has lifted it to the mid-13,000 area.

Yet unlike the NASDAQ, most value indexes have held strong.

The Russell 1000 Value is ever-so-slightly in the black since the day the NASDAQ peaked, posting a 1.5% gain, even as the NASDAQ buckled. In that time, the benchmark t-note’s yield shot up from 1.55% to 2.67%, which spooked indexes like the Russell 1000 Growth into a collapse that mirrored that of the NASDAQ. The index hit the 20% loss threshold that marks bear markets a few weeks ago, though the total loss since November 19 currently stands at 14.8%.

That means value has beaten growth by over 1,600 basis points in half a year. And I think there is more to come.

If you suspect the new rule of thumb— “Rates Up = Value Good, Growth Bad” —has staying power, here are two Funds to review:

The WisdomTree U.S. LargeCap Dividend Fund (DLN)

The WisdomTree U.S. Value Fund (WTV)

Both have histories dating to before the global financial crisis, with expense ratios of 0.28% and 0.12%, respectively.

Unless otherwise stated, all data through 4/1/22.

Important Risks Related to this Article

DLN: There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WTV: There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

Related articles

Dividend Growth Is Not One Strategy

Beyond Market Cap: A Nearly 19-Year Case for Dividend-Driven Emerging Markets

Quality as a Foundation in an Uncertain World

The Market's Pendulum May Be Swinging Back to Value

The 2026 Market: A World of Constant Rotation

Value Isn’t What It Used to Be

Are Two Complementary Strategies Continuing to Create a Better Core in 2026?

Don’t Mistake Speculation for Strength: The Mirage of Small-Cap “Junk” Outperformance

From Momentum to Discipline: Navigating Volatility in Emerging Markets

About the contributor

Jeff Weniger, CFA

Head of Equity Strategy

Jeff Weniger, CFA, has been with WisdomTree since 2017 and serves as the Head of Equities. He shapes the firm’s market outlook through a combination of macroeconomic and fundamental analysis. With more than two decades in investment strategy, Jeff is known for his work on market cycles and valuations. Before joining WisdomTree, Jeff was with BMO Private Bank and BMO Global Asset Management for 11 years. At BMO, he sat on the firm’s Asset Allocation Committee and co-managed ETF model portfolios across the U.S. and Canada. In 2013, at age 32, he became the youngest member of BMO’s Global Investment Forum. When he left BMO to come to WisdomTree, his final role was Director, Senior Strategist in the Office of the CIO in 2017.

Jeff is a frequent television guest on networks such as CNBC, Bloomberg, and Schwab, with regular print appearances in The Wall Street Journal, Barron’s and Reuters. He also appears weekly on the Behind the Markets podcast and is a regular on SiriusXM’s The Business Briefing. On X, Jeff has developed one of the larger followings in financial media. He earned a B.S. in Finance from the University of Florida and an MBA from the University of Notre Dame. He has held the CFA charter since 2006.