Japan’s Second Act: Shareholder Returns and Global Relevance

Published November 12, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- Japanese equities have quietly outperformed in 2025, and the election of Prime Minister Sanae Takaichi signals a potential new phase of policy continuity and reform. Her pro-growth stance could further amplify momentum in shareholder returns, corporate governance and valuation re-rating.

- Warren Buffett’s growing stake in Japan’s five major trading houses highlights their global reach, disciplined capital allocation and central role in powering the WisdomTree Japan Opportunities Fund (OPPJ).

- Since its July 2025 strategy shift, OPPJ has delivered a greater-than-16% return, nearly doubling that of the MSCI Japan Index by focusing on companies leading Japan’s corporate transformation.

- In early November 2025, Warren Buffett filed for another yen bond issuance, indicating desires to increase his currency hedge or put more capital to work buying more Japanese stocks.

U.S. stocks remain the world's benchmark for innovation and growth but are also the poster child for ‘high' valuations. Are they too high? Many publications are calling out a potential AI-Bubble—driven by strong flows from investors around the world.

Our team likes to call Japan: the Anti-Bubble.

Japanese equities have quietly advanced through much of 2025, supported by deepening corporate governance reforms, rising capital efficiency and a cultural shift toward shareholder value.

Now, with Sanae Takaichi's elevation to leadership, Japan may be entering a new phase of pro-growth and market-oriented policy continuity. Her stance could strengthen the reform momentum already underway, further enhancing shareholder returns and helping valuations—still far more modest than in the U.S.—to catch up with fundamentals. Price-to-earnings (P/E) and price-to-book (P/B) ratios sit at discounts that look increasingly difficult to justify in a world where corporate Japan is finally closing the gap on profitability and return on equity (ROE).

For U.S. investors who instinctively look inward, this contrast is striking. While the domestic market feels expensive, Japan offers a compelling counterpoint: strong performance, improving fundamentals and valuations that suggest the runway is far from exhausted. It is an opportunity often overlooked, but precisely because of that neglect, the potential is greater. In a market environment where global diversification is no longer optional but essential, Japan deserves to be considered not as a curiosity, but as a serious core allocation.

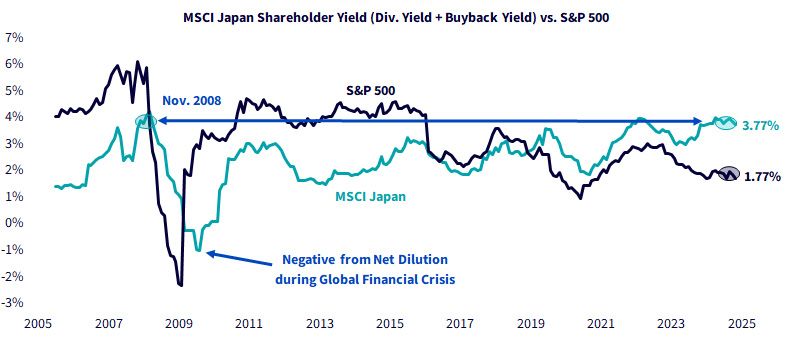

Japan's Shareholder Yield Sends a Clear Message

Japanese equities are sending a powerful signal through shareholder yield. By combining dividends and buybacks, the MSCI Japan shareholder yield now sits near 4%, levels seem a few times as relative peaks, going back to the 2008-09 global financial crisis.

The crucial difference this time is the high yield is not coming from collapsing prices, but from a surge in corporate payouts. Companies across Japan are distributing more cash to shareholders than at any point in the modern era, reflecting governance reforms and an explicit push from policy makers and the Tokyo Stock Exchange (TSE) for firms to prioritize capital efficiency. This stands in sharp contrast to the S&P 500, where buybacks have slowed and aggregate shareholder yield has fallen closer to 2%.

Since 2023, the TSE has pressured companies trading below book value to "explain or comply" with plans to improve capital efficiency, spurring both buybacks and dividend hikes. At the same time, the Government Pension Investment Fund (GPIF), the world's largest pool of retirement assets, has reinforced the case for better shareholder returns through its stewardship expectations.

The data is clear: Japan executed a record level of buybacks in 2024, exceeding ¥9 trillion, and 2025 is on pace to sustain that momentum. With ROE steadily rising and payout ratios climbing, investors are seeing a Japan that looks far different from the capital-hoarding corporate culture of decades past.

Sanae Takaichi's emergence as Japan's new prime minister adds an important political tailwind to this structural shift. Known for her pragmatic, pro-growth orientation, Takaichi has signaled strong support for the corporate reform agenda that has underpinned Japan's equity resurgence.

Her administration is expected to prioritize policies that sustain capital market vibrancy—strengthening governance standards, fostering innovation and attracting both domestic and global investment. Unlike past cycles, this alignment between government leadership, institutional capital and corporate behavior creates a more durable foundation for equity performance. For investors, Takaichi's leadership represents continuity where it matters—on shareholder returns and economic revitalization—but also a potential acceleration in tone and execution. Japan's transformation from a value trap to a value opportunity may now have the political reinforcement it lacked for decades, setting the stage for a reappraisal of Japanese equities on the global stage.

Figure 1: Japan's Shareholder Yield Rivals Crisis-Era Peaks

Sources: WisdomTree, FactSet, with data from WisdomTree's PATH suite of tools and covering the period 6/30/06–10/31/25. Past performance is not indicative of future results.

Following Buffett: Trading Houses as the Core of Japan's Opportunity

Warren Buffett has been unusually vocal about his enthusiasm for Japan's great trading houses, ITOCHU, Marubeni, Mitsubishi, Mitsui and Sumitomo, going so far as to compare their diversified business models to Berkshire itself.

Since first buying shares in 2019, he has steadily increased Berkshire's stake, bringing ownership close to 10% in each. What excites Buffett is not just their global reach but their shareholder-friendly orientation: disciplined capital deployment, sensible buybacks, steady dividend growth and restrained executive compensation.

By 2024, Berkshire's $13.8-billion investment had grown to a market value of $23.5 billion. Even more telling, the annual dividend income expected from these holdings in 2025 is around $812 million, versus only $135 million in interest costs from the yen-denominated debt used to finance them. For Buffett, these companies embody a rare blend of value, governance and global partnership potential, an investment he expects Berkshire to hold "for many decades."

In early November, Buffett recently filed for another yen bond issuance, indicating desires to increase his currency hedge or put more capital to work buying more Japanese stocks1.

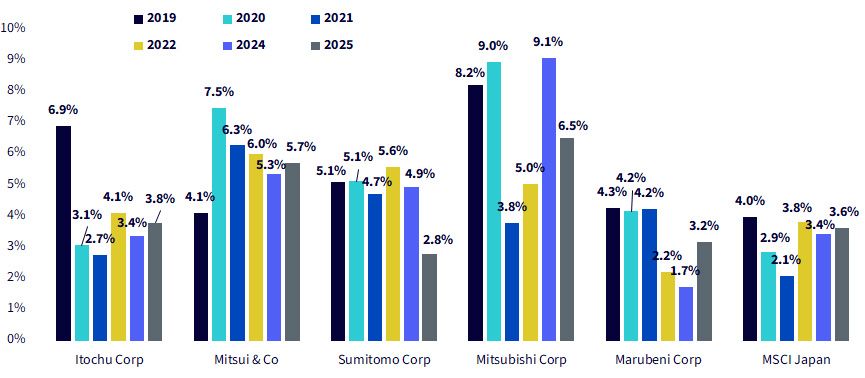

Buffett's Japanese trading houses demonstrate strong leadership and provide examples for others to follow:

- In figure 2a, we see the end-of-year figures for total shareholder yield for the five Japanese trading houses going back to 2019 and carrying through to August 2025. Why did we start in 2019? Because this was the year that Buffett initiated these positions for Berkshire.

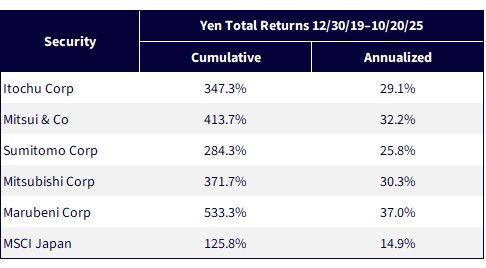

- In figure 2b, we seek to show the actual return of these companies over this period, in local currency terms so as not to dilute the return from any movement in the U.S. dollar to Japanese yen exchange rate. Performance has been very strong relative to the MSCI Japan Index-yet these companies yields remain high despite prices appreciating.

Figure 2a: Shareholder Yield of the Five Trading Houses vs. the MSCI Japan Index

Sources: FactSet, MSCI, with data measured as of 12/31 of each specified year except 2025, where data is measured as of 10/31. Past performance is not indicative of future results.

Figure 2b: Total Returns of the Five Trading Houses vs. the MSCI Japan Index

Sources: FactSet, MSCI. Yen total returns means that these returns do not include any impact of changes in the exchange rate between the Japanese yen and U.S. dollar. Past performance is not indicative of future results.

WisdomTree Japan Opportunities Fund (OPPJ): The strategy is allocated to companies in four different buckets. First, the Index will be allocated to securities of Japanese companies that are strategic holdings of Berkshire Hathaway.2 Second, the Index will be allocated to companies that provide a high "total shareholder yield," evidenced by return of capital to shareholders through either dividend distributions and/or the repurchase of shares ("buybacks"), and positive trends in earnings and dividend growth. Third, the Index will be allocated to companies classified as "corporate governance improvers," evidenced by low valuation ratios (such as a low price-to-book ratio) and favorable earnings and dividend growth characteristics. Four, the Index will be allocated to securities that have exposures to thematic opportunities from developments in the geopolitical space, technology trends and macroeconomic conditions.

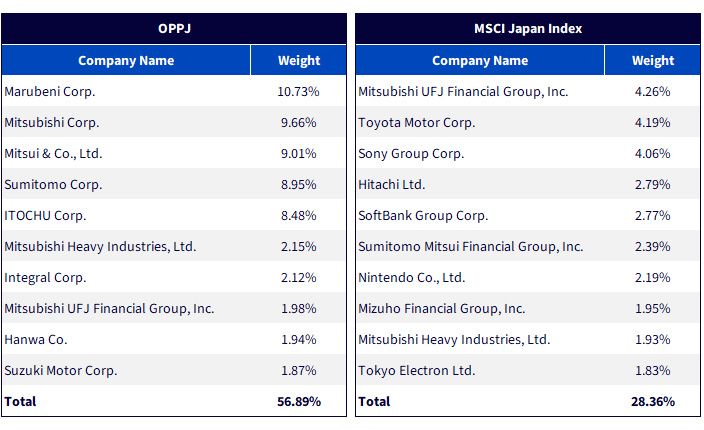

Buffett's conviction in Japan's five great trading houses, Marubeni, Mitsubishi, Sumitomo, Mitsui and Itochu, shows up unmistakably in the Japan Opportunities Fund. This is not an incidental overlap; it's a deliberate concentration in the very firms Buffett has called out for their disciplined capital allocation, diversified business reach and shareholder-friendly reforms. By anchoring OPPJ in these industrial powerhouses, the strategy doesn't just mirror Buffett's bets, it magnifies them, offering investors a focused way to participate in the same shareholder-return revolution that drew Berkshire Hathaway to Japan in the first place.

Figure 3: Showcasing the Prominence of the Five Trading Houses

Sources: WisdomTree, FactSet, with data as of 9/30/25 and from WisdomTree's PATH set of tools. Holdings are subject to change.

Performance: Where the Rubber Meets the Road

Between July 1 and early November 2025, the period for which the current strategy of OPPJ has been in place, the five trading houses that Warren Buffett and Berkshire Hathaway highlighted were the key drivers of performance in OPPJ. Each of these companies contributed positively, with Marubeni, Mitsui, and Mitsubishi standing out as the largest contributors. Together, the group accounted for the bulk of the Fund's nearly 20% return over the period, a result that far exceeded the MSCI Japan benchmark. Their outsized impact reflects not just their weight in the portfolio but also the momentum behind their diversified business models and disciplined capital allocation strategies.

Figure 4a: Standardized Performance, as of September 30, 2025

Figure 4b: Focused Exposure Has Led to Stronger Returns

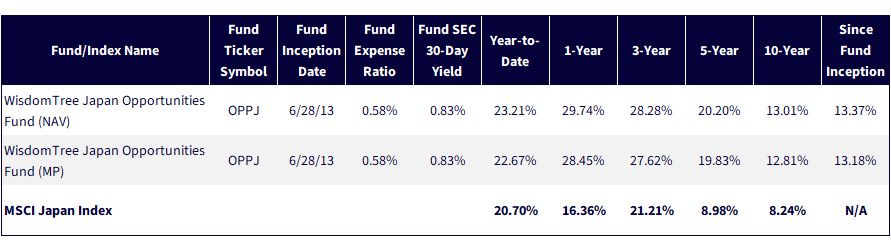

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 11/10/25 with returns as of 11/7/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Prior to 7/01/25, the Fund was known as the WisdomTree Japan Hedged SmallCap Equity Fund (DXJS). On that date, the Fund's investment policy changed. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Conclusion: Japan's Time in the Global Spotlight

For too long, Japan has been treated as a peripheral allocation, an afterthought in global equity portfolios dominated by the U.S. But the story unfolding today is different. Valuations remain compelling, corporate reforms are real and accelerating, and companies are returning record levels of cash to shareholders. Add to this the seal of approval from Warren Buffett's Berkshire Hathaway, and investors have a roadmap that highlights both the opportunity and the credibility of Japan's market evolution.

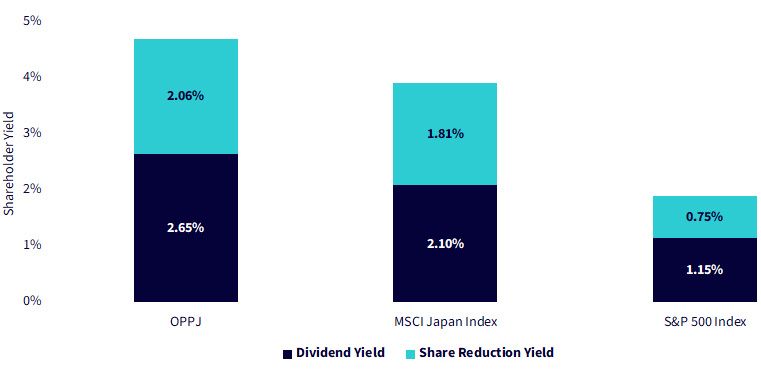

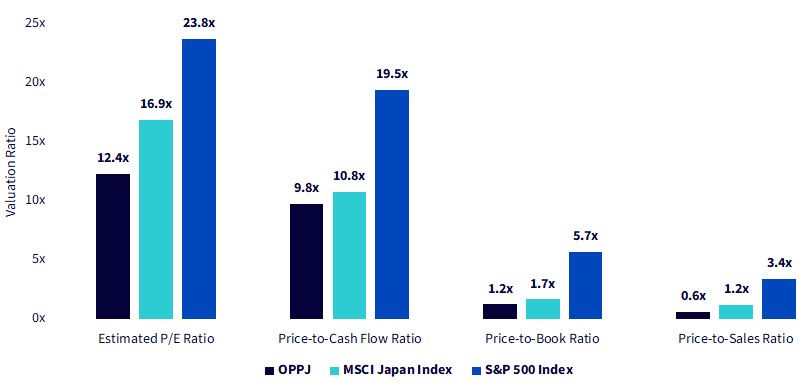

In figures 5a and 5b, we can see Japan's valuation advantage, both from a shareholder yield perspective and a slate of more traditional valuation metrics: estimated P/E ratio, price-to-cash flow ratio, P/B ratio and price-to-sales ratio.

As a reference point, since it comes up so often, we show the metrics for the S&P 500 Index, a widely followed benchmark for U.S. equities.

Figure 5a: Components of Shareholder Yield

Figure 5b: Showcasing Japan's Valuation Advantage

Sources: WisdomTree, FactSet, with data from WisdomTree's Fund Comparison Tool in the PATH set of tools. Data as of 9/30/25. Past performance is not indicative of future results.

In a world where U.S. equities feel stretched, Japan offers a refreshing mix of strong fundamentals, attractive shareholder yield and global relevance. The combination of disciplined corporate behavior, supportive policy shifts and concentrated exposure to the country's most dynamic enterprises has created one of the most underappreciated opportunities in global investing. For investors willing to look beyond their home market, Japan is no longer the market that was forgotten, it is the market that could define the next chapter of global equity leadership.

1 Source: Bloomberg News. (2025, November 6). Berkshire Hathaway plans yen bond amid global debt binge. Bloomberg.

2 Refers to Itochu Corporation, Marubeni Corporation, Mitsubishi Corporation, Mitsui & Co., Ltd., Sumitomo Corporation. The source for these companies being mentioned as strategic holdings is W.E. Buffett, "Berkshire Hathaway Inc. 2024 Annual Letter to Shareholders," Berkshire Hathaway Inc., berkshirehathaway.com, 2/24/25.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations, derivative investments which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.