GDE

Efficient Gold Plus Equity Strategy Fund

Published March 30, 2026

Global Head of Research

New geopolitical events have been arriving fast and furious over the past year. Key events include Liberation Day in April 2025; regime change in Venezuela in January 2026; Trump’s discussion of possibly acquiring Greenland in January 2026; and then the start of the U.S./Israel-Iran war at the end of February 2026.

Figure 1 shows how much gold has risen following past geopolitical shock events. In most cases, gold tended to outperform equities by a significant margin.

Source: Bloomberg, WisdomTree, 1973–2026. Past performance is not indicative of future results. *Not a full year since event, so latest data taken March 13, 2026. Equities refers to the S&P 500 Index, specifically the price return, which does not include the impact of any dividend reinvestment. Gold refers to the LBMA gold price, calculated as of the afternoon fixing. Relative refers to the gold price return minus the equity return. The return is calculated as the 1 year period following the date specified, for example, the Israel-Hamas War was October 7, 2023, so the period would be from that date to October 7, 2024. Others are calculated analogously. No backtested performance is used in the calculation of this table.

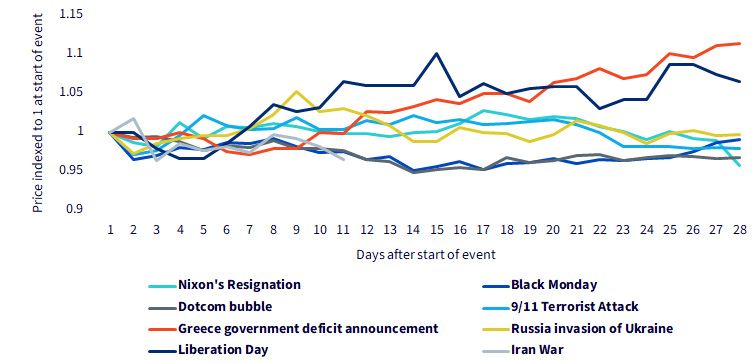

Multiple weeks into the Iran conflict, gold prices have remained below where they were when the conflict began. Is this unusual? Not really. Looking back at historical geopolitical shock events, this pattern has been fairly common.

The figure below is a subset of the table above, focusing on cases where prices initially came under pressure. The 9/11 terrorist attacks, the dot-com bubble, Black Monday, Nixon’s resignation, the Russia-Ukraine war and the Greek sovereign crisis all saw some degree of negative gold price pressure before prices subsequently surged. As we know, these past events cannot guarantee a future outcome, but we find historical patterns important in providing context to better understand the range of possible forward-looking outcomes.

The duration of this initial downside pressure has varied across the different episodes, but the mechanics have been broadly similar:

One factor that may be somewhat unique this time is additional selling pressure from households in the Middle East, who are seeking liquid resources to meet unexpected expenditures, such as purchasing expensive plane tickets to evacuate the region. Bloomberg has reported heavy discounts on gold sold in local markets during the first week of the conflict.1

Source: Bloomberg, WisdomTree, 1974–2026. Past performance is not indicative of future results.

At around $5,000/oz, the price of gold at the time of this writing, gold appears severely underpriced, in our opinion. We believe that many investors will view this period of consolidation as an attractive entry point to increase gold exposure.

Trump has not articulated a clear objective for the specific Iran conflict, and given that this is a mid-term election year, he will be under pressure to deliver some form of closure. However, Iran is unlikely to accept a ceasefire quickly. Trump may decide to declare victory before Iran’s military capability is fully neutralized, leaving significant geopolitical risks lingering for some time. In such an environment, gold is likely to remain well supported.

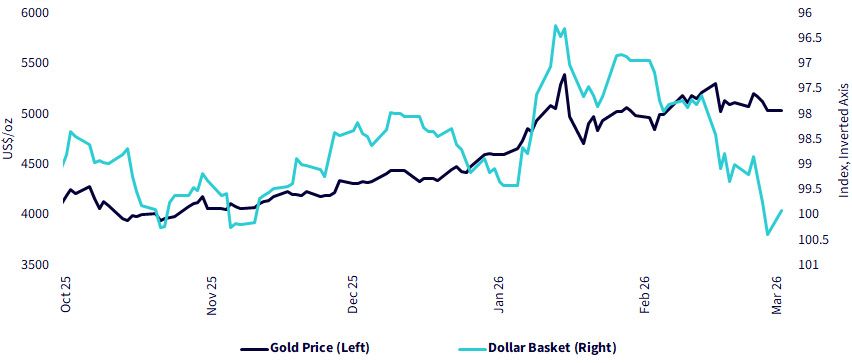

One of the reasons gold has not risen as much in U.S. dollar terms is that the U.S. dollar itself has strengthened, reflecting its status as a safe haven currency relative to other global currencies. The dollar has appreciated more than other traditional haven currencies during this conflict that, as we said, began at the end of February 2026. Other safe haven currencies such as the Swiss franc and the yen face additional challenges, as Switzerland and Japan are net energy importers, in contrast to the United States, which is largely energy independent.

If the current strength in the U.S. dollar subsides, it is possible for gold’s price to move higher. Structural downside pressures on the dollar remain in place, including a widening twin deficit2 and heightened uncertainty around Trump’s acceptance of Federal Reserve independence.

Source: Bloomberg, WisdomTree, October 2025–March 2026. Past performance is not indicative of future results.

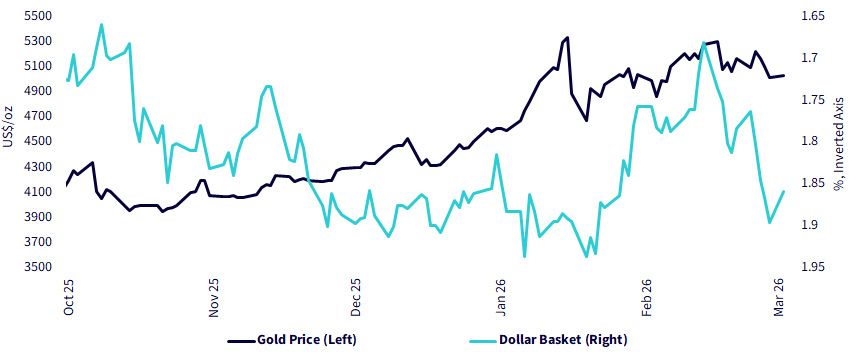

Rising bond yields have also been a headwind for gold. Many traders are reducing their expectations for near-term interest rate cuts as inflationary pressures rise. As a result, longer-term bond yields have increased. Higher bond yields typically exert downward pressure on gold prices.

Source: Bloomberg, WisdomTree, October 2025–March 2026. Past performance is not indicative of future results.

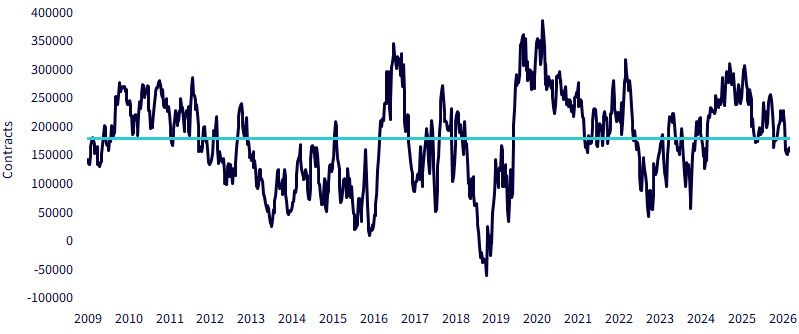

Net speculative positioning in gold futures also appears relatively subdued given the geopolitical backdrop. For some time, we have observed that futures market positioning has not fully reflected the strength of global positive sentiment towards gold.

Source: Bloomberg, WisdomTree, 2009–2026. Past performance is not indicative of future results.

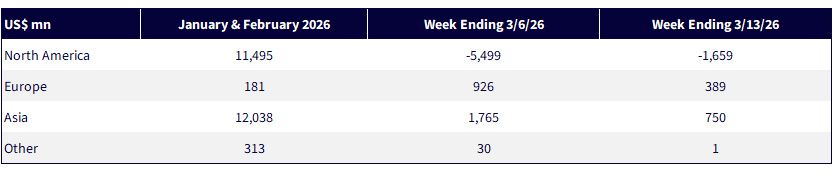

Exchange-traded product (ETP) flows have also shifted abruptly since the start of the war. In January and February 2026, North America saw very strong inflows totaling $11.5 billion. During that period, European flows were relatively muted, while Asian flows were even higher than those in North America.

However, since the start of the conflict, more than $7 billion has flowed out of North American products, while inflows into European products have accelerated. Asian flows remain strong. With consistent inflows, Asia remains by far the largest ETP market by flows this year.

Source: World Gold Council, January 1, 2026–March 13, 2026. Past performance is not indicative of future results.

Taken together, the recent consolidation in gold prices appears to reflect short-term liquidity pressures rather than a deterioration in fundamentals. Geopolitical risks remain elevated, structural pressures on the U.S. dollar persist, and investor positioning remains relatively light given the backdrop. As these temporary headwinds fade, gold’s role as both a geopolitical hedge and a portfolio diversifier is likely to reassert itself. In this context, the current price environment may ultimately be remembered as a compelling opportunity to increase exposure to gold.

If investors are thinking of different avenues through which gold exposure may be achieved, we’d want to remind people about some of our efficient gold exposures that take away the need to make certain allocation of ‘this or that’ and instead open up an option for ‘this and that’ in the same allocation. The two examples that have been live throughout 2026:

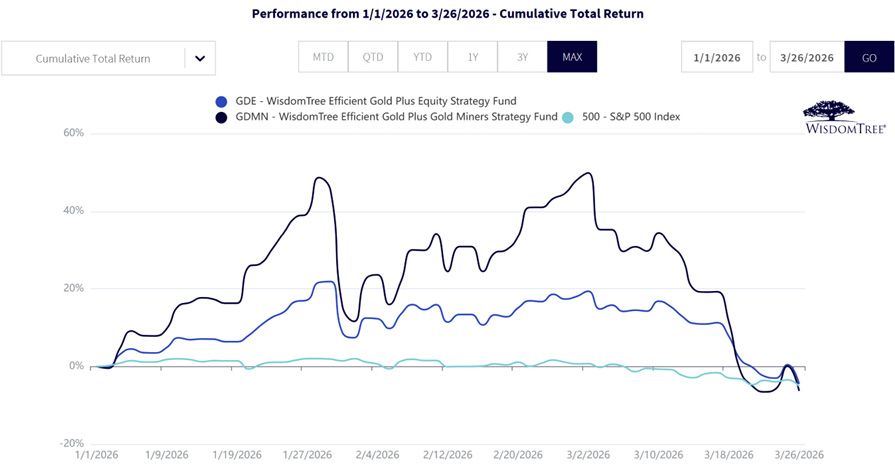

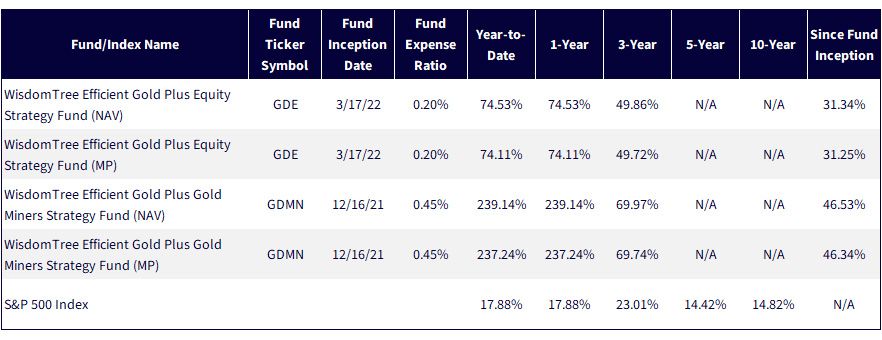

Figure 7a indicates the performance so far in 2026 relative to that of the S&P 500 Index.

Sources: Morningstar, FactSet and WisdomTree. Specifically, data are from the PATH Fund Comparison Tool, showing returns for the period ended March 26, 2026 for Figure 7a and December 31, 2025 for 7b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDMN, GDE.

It’s important to see these strategies during such periods where gold is providing something truly differentiated, by way of returns, versus equities. It makes sense to us that GDMN'sprofile appears more volatile with its specific focus on gold miners relative to GDE, with its focus on a broad basket of 500 market capitalization-weighted U.S. equities. The critical point is that there are different avenues to garner exposure to gold on the investment menu. We also see their behavior amidst a more challenging environment from the standpoint of gold prices.

1 Gold Stuck in Dubai Is Being Sold at Discount as War Widens, Bloomberg March 7, 2026.

2 The twin deficit refers to the U.S. government’s fiscal deficit, meaning it takes in less revenue than it spends, and the U.S. economy’s current account deficit, meaning the country takes in more imports than it exports.

There are risks associated with investing, including possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile. The Funds’ investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains.

The Fund is actively managed and invests in U.S listed gold futures and U.S. equity securities. The Fund’s use of U.S. listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate.

The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political, or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic, or regulatory conditions affecting that country or region, or emerging markets generally.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.