WQTM

Quantum Computing Fund

Published April 1, 2026

Global Head of Research

There’s a quiet assumption embedded in thematic investing that rarely gets questioned:

Investors agree on what the theme actually is.

Often when speaking to investors, the concept hanging over the discussion is something like this:

What is the ‘benchmark’ for this concept? For example, does AI, the theme, have a benchmark? Defining a benchmark makes it possible to ask how a given strategy is performing against it.

Now, some themes are clearer than others. Topics like ‘Semiconductors’ and ‘Defense’ do at least show up within the GICS classification hierarchy.1 That’s not to say that showing up within this hierarchy is ‘enough’ or ‘perfect’, but at least these topics are represented.

What about something like ‘Quantum Computing’?

This theme is still very early, abstract and rapidly evolving. Defining what it is—more specifically put, what companies should be represented within it—may be the most important investment decision of all.

Two ETFs in the market today attempt to answer that question.

They both claim exposure to the same theme. But beneath the surface, they reflect two very different ways of thinking about where quantum computing lives, how it develops and what investors might actually own in terms of companies exposed to this emerging topic.

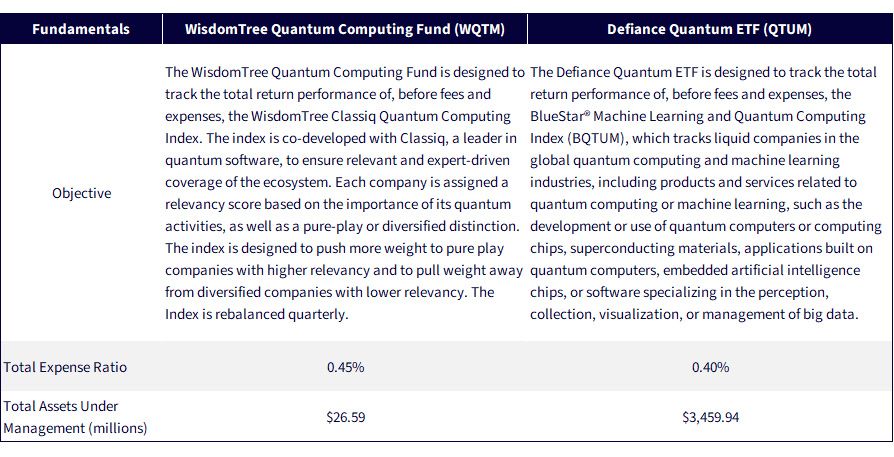

We would note that QTUM is the largest U.S. listed ETF by assets under management that has a focus on quantum computing—more than $3.4 billion as of this writing.4

At the heart of the divergence is a simple but powerful distinction. To truly do this sort of comparison justice, we have to focus on the methodology of the indices that underlie WQTM and QTUM specifically.

From a high level, the BlueStar® Machine Learning and Quantum Computing Index (tracked by QTUM) begins with the idea that quantum computing is part of something bigger.

The WisdomTree Classiq Quantum Computing Index (tracked by WQTM) treats quantum computing more as something that can be isolated, measured and targeted directly.

That high-level philosophical difference ends up shaping everything that follows, from which companies make it into the portfolio to how much weight they ultimately carry.

One is trying to capture a system. The other is trying to isolate a signal.

The BlueStar® Machine Learning and Quantum Computing Index approach looks at quantum computing not as a standalone industry, but as one branch of a broader transformation in how computation works.

In this view, quantum sits alongside artificial intelligence, machine learning, advanced semiconductors and data infrastructure as part of a single, evolving ecosystem. The companies that matter are not just those building quantum systems, but those enabling the next generation of compute more broadly.

That leads to a methodology that is expansive by design. A company does not need to be purely focused on quantum computing or other specific quantum-related technologies to be included. It simply needs to participate in the architecture of modern computing. Semiconductor manufacturers, graphics processing unit (GPU) designers and data-centric businesses all fit naturally into that framework.

Quantum computing companies as well as the topic are present, but they are embedded within a larger narrative about compute scaling and technological convergence.

Once the opportunity set is defined in that way, the rest of the portfolio construction follows almost intuitively. The goal becomes capturing the bulk of that ecosystem rather than isolating a narrow subset within it. Larger companies, by virtue of their scale and influence, tend to dominate the selection process.

The result, at least in our opinion, is something that looks less like a pure-play quantum strategy and more like a next-generation computing index with quantum as one of its components.

The WisdomTree Classiq Quantum Computing Index approach starts from a different premise.

It assumes that proximity to a theme is not the same as participation in it. Instead of asking whether a company belongs to advanced computing broadly, it asks how central quantum computing is to the company’s business.

That shift in perspective changes the entire construction process. Companies are no longer evaluated simply on whether they belong to a category. They are assessed based on how deeply they are involved in advancing quantum technologies and how much of their business is actually tied to those activities.

A company building quantum chips or developing quantum algorithms is treated very differently from a large, diversified firm that happens to have a small quantum initiative within a much broader operation.

What emerges is a more deliberate attempt to separate signal from noise. Some companies are identified as being highly relevant to the progress of quantum computing. Others are recognized as participating in the space but in a more peripheral way. There is also a distinction between firms that are essentially pure plays in quantum and those for which quantum is just one part of many business lines.

This framework introduces something the broader approach does not attempt to capture: degrees of exposure.

Once the universe is defined, the next question is how to build an index of companies from it.

In the BlueStar® Machine Learning and Quantum Computing Index, the ecosystem-driven strategy, the objective is coverage. The portfolio is constructed to capture the majority of the market capitalization within the defined universe. That naturally pulls in large, dominant companies and ensures broad representation across the compute landscape.

The emphasis is on scalability, liquidity and completeness. It reflects where capital and infrastructure already exist.

In the WisdomTree Classiq Quantum Computing Index, the more targeted strategy, the objective shifts from coverage to relevance. The portfolio is built by identifying companies that are meaningfully advancing quantum computing, regardless of their size. This allows for greater inclusion of smaller, earlier-stage firms that might otherwise be overshadowed.

The result is a portfolio that is less about mirroring the current structure of the market and more about expressing a view on where the innovation is actually happening.

The most important difference between these approaches is not what constituents they include, but how they weight them.

In the BlueStar® Machine Learning and Quantum Computing Index approach, companies are generally treated equally, with adjustments for liquidity. There is no explicit attempt to give more importance to companies that are more deeply tied to quantum computing. A quantum-focused firm and a semiconductor giant can sit side by side with similar weights.

Quantum exposure is present, but it is not prioritized.

In the WisdomTree Classiq Quantum Computing Index approach, equal weighting is only the starting point. From there, weights are adjusted based on how relevant a company is to quantum computing and how concentrated its business is in that area. Companies that are both highly relevant and more ‘pure’ in their exposure are systematically emphasized. Those that are less central are scaled back.

This is where the philosophy becomes tangible. The portfolio doesn’t just include quantum computing companies—it leans into them.

And that distinction ultimately determines what drives performance. This does not indicate whether one strategy will outperform the other or whether quantum computing firms will have a strong performance year, but it can help illustrate how sensitive the strategy may be if a quantum-specific thesis plays out.

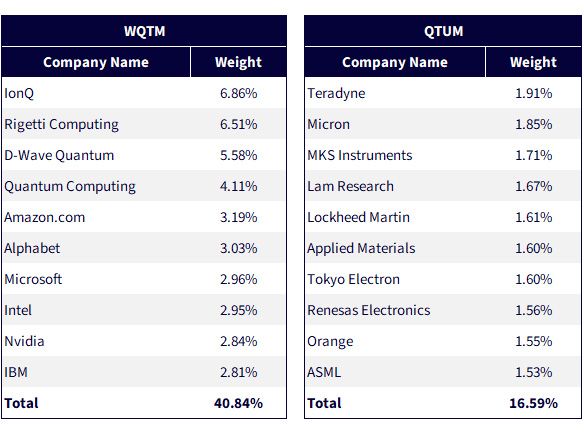

From a distance, both strategies are labeled “quantum.” But functionally, they behave very differently. We can see this presented in Figure 1, where we see the top 10 holdings.

Sources: WisdomTree, FactSet, Morningstar, with data as of February 28, 2026. Holdings subject to change.

Looking at the top 10 holdings in Figure 1, QTUM could be more of a bet on the infrastructure that could enable quantum. WQTM could be a bet on the companies attempting to build it.

The natural instinct is to ask which approach is better. But, in our opinion, that framing misses the deeper point. These strategies are not, in our view, competing answers to the same question. They are answers to different questions entirely.

QTUM, through the methodology of its underlying index, may be asking: how do we gain exposure to the evolution of computing, where quantum may eventually emerge?

WQTM, through the methodology of its underlying index, may be asking: how do we directly target the companies most responsible for advancing quantum itself?

Those are fundamentally different exposures.

In mature sectors, definitions are stable. The boundaries are clear. But in emerging technologies, definitions are still being written in real time.

And those definitions are not neutral.

They determine what gets included, what gets emphasized and what ultimately drives returns.

When you invest in quantum computing, you are not just investing in a technology.

You are investing in a definition of that technology, and a view on how it will take shape in the years ahead.

Right now, that definition is still very much up for debate.

Sources: WisdomTree, Defiance, with assets under management data pulled as of March 17, 2026. Subject to change.

1 MSCI Inc. and S&P Dow Jones Indices LLC. (2023). Global Industry Classification Standard (GICS®) Methodology. Semiconductors is an Industry and Aerospace & Defense is an Industry in this framework.

2 In this piece, the source for any comments on the WisdomTree Classiq Quantum Computing Index methodology is: WisdomTree, Inc. (March 2026). WisdomTree Rules-Based Methodology: Quantum Computing Index.

3 In this piece, the source for any comments on the BlueStar® Machine Learning and Quantum Computing Index methodology is: MarketVector Indexes GmbH. (February 2026). BlueStar® Machine Learning and Quantum Computing Index Guide (Version 1.05).

4 Source: QTUM fund page, with data as of March 17, 2026. Subject to change.

5 Sources: The Quantum Insider. (October 20, 2025). Public Quantum Stocks 2025: From Pure Plays to Tech Giants; Williams, S. (February 18, 2026). Quantum Computing Stocks IonQ, Rigetti Computing and D-Wave Quantum Have Issued a Can’t-Miss Warning to Wall Street. The Motley Fool.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

WQTM: There are risks associated with investing, including potential loss of principal. To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting that country or region. The economic, political, regulatory, and other events and conditions that affect issuers and investments in the United States differ significantly from those associated with other countries and regions. U.S. financial markets have become increasingly globalized becoming more integrated with financial markets around the world and as a result, U.S. financial markets are increasingly vulnerable to the risks that may affect non-U.S. financial markets. The Fund’s investments in the U.S. are subject to the risk that they, and the U.S. economy more generally, will be adversely affected by a decrease in imports or exports, changes in trade regulations, inflation, and/or an economic recession in the U.S. The Fund invests primarily in the securities of quantum computing companies. Companies engaged in the development of quantum computing or machine learning technology may be significantly impacted by rapid technological advancements, product obsolescence, intense competition, consumer demand, and government regulation. Such companies are also heavily dependent upon patent and intellectual property rights. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

For QTUM’s risk disclosures, click here.

Quantum Computing Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.