GDMN

Efficient Gold Plus Gold Miners Strategy Fund

Published February 5, 2026

Global Head of Research

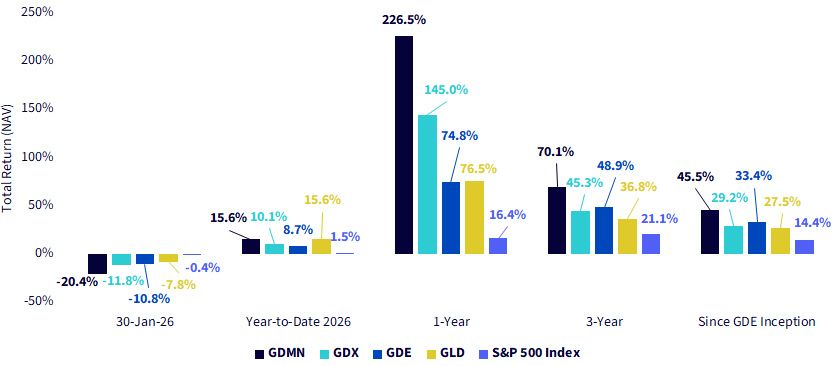

The January 30 selloff in gold's price was not a repudiation of gold's longer-term investment case, but it could have been a violent correction within an already elevated volatility regime. By late January, gold prices had reached levels that reflected not only heightened macro anxiety but also increasingly compressed time horizons. Moves that would historically have unfolded over quarters, or even years, were instead realized over days. After reaching an intraday high near $5,595 per ounce on January 29, gold reversed sharply, falling below $5,000 intraday the following session, highlighting how stretched momentum and positioning had become1.

Placing January 30, 2026 into History

Sitting in January 2026, investors that may have been focused on gold or allocating to gold over the recent strong price performance need to review how different instruments performed in the face of January 30, 2026's market volatility.

So let's consider some of the more popular choices:

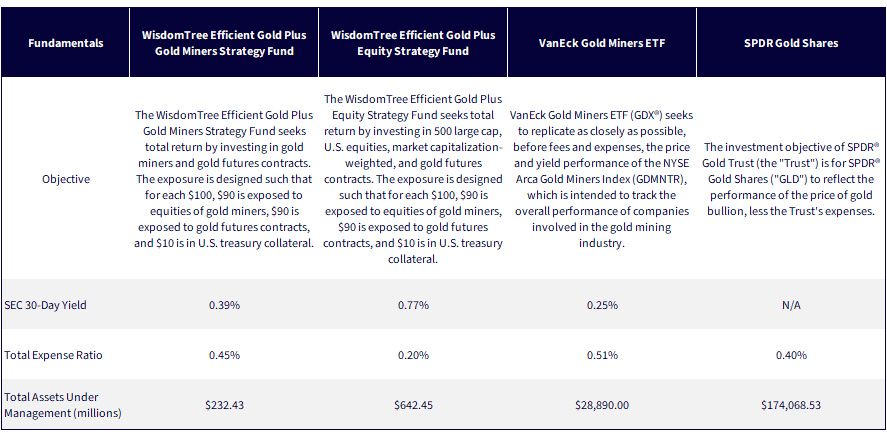

WisdomTree has introduced capital-efficient exposures that combine gold other assets into a single investment strategy. Two such strategies, each of which has been live in the market for more than three years, are:

The primary rationale for WisdomTree's launching these strategies and then investors considering them, in our opinion, is not gold's recent strong performance. Instead, it is meant to help with the allocation decision that many face when thinking about what portfolio assets need to be sold, and therefore exposures given up, to include gold in an overall allocation.

GDE allows investors to allocate to gold without commensurately reducing exposure to a broad portfolio of U.S. equities. Over longer historical time horizons, lower correlations of returns between gold and U.S. equities have been useful in considering such a strategy's potential volatility profile.

GDMN allows investors to avoid having to decide whether gold or gold miners fits their investment thesis—they can allocate to both within one strategy.

To generate these exposures, leverage is used, meaning that for a hypothetical $100 invested, $180 of notional exposure is generated. Leverage can magnify volatility, especially during periods where both underlying exposures are moving in the same direction, either positive or negative.

As we see in Figure 1a:

Figure 1a: Placing January 30, 2026 into a broader Historical Track Record

What January 30 Actually Tells Us

The January 30, 2026 selloff was extraordinary in magnitude, but not extraordinary in meaning. History suggests that gold's sharpest drawdowns rarely signal the end of its investment case; they tend to mark moments when markets are forced to reconcile crowded positioning, compressed time horizons, and rapidly shifting expectations. What made this episode distinctive was not simply how far prices fell, but how quickly the adjustment occurred. Moves that once unfolded over quarters were compressed into a single trading session.

Sources: WisdomTree, VanEck and SPDR. Assets under management as of January 30, 2026.

1 Sources: Financial Times. (2026, January 31). Gold and silver prices plunge as rally goes into reverse; Barron's. (2026, January 31). Gold and silver prices fall sharply as Trump picks Warsh as Fed chair. Here's why.

2 Source: World Gold Council. (2013). Market update: Q2 2013.

3 Sources: Duffie, D. (2020). Intermediation of U.S. Treasury markets after the COVID-19 crisis. Federal Reserve Bank of New York, Liberty Street Economics; Office of Financial Research. (2023). Flight to safety and the dash for cash: Market dynamics in March 2020. U.S. Department of the Treasury.

4 Sources: Baur, D. G., & McDermott, T. K. (2010). Is gold a safe haven? International evidence. Journal of Banking & Finance, 34(8), 1886–1898; Reuters. (2026, January 30). Gold set for steepest daily drop since 1983 as bets of a more hawkish Fed rise. Reuters.

5 The investment objective of SPDR® Gold Trust (the "Trust") is for SPDR® Gold Shares ("GLD") to reflect the performance of the price of gold bullion, less the Trust's expenses. It is the largest fund ranked by assets under management that provides exposure to movements in the price of physical gold.

6 Source for Assets under management is SPDR website, specifically the GLD page.

7 VanEck Gold Miners ETF (GDX®) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the NYSE Arca Gold Miners Index (GDMNTR), which is intended to track the overall performance of companies involved in the gold mining industry. It is the largest fund ranked by assets under management that provides exposure to movements in the share prices of a group of gold mining companies.

8 Source for assets under management is VanEck website, specifically the GDX page.

9 The WisdomTree Efficient Gold Plus Gold Miners Strategy Fund seeks total return by investing in gold miners and gold futures contracts. The exposure is designed such that for each $100, $90 is exposed to equities of gold miners, $90 is exposed to gold futures contracts, and $10 is in U.S. treasury collateral.

10 The WisdomTree Efficient Gold Plus Equities Strategy Fund seeks total return by investing in a basket of 500, large capitalization U.S. equities, weighted by market capitalization, and gold futures contracts. The exposures is designed such that for each $100, $90 is exposed to equities of U.S. equities, $90 is exposed to gold futures contracts, and $10 is in U.S. treasury collateral.

11 Source: Bloomberg.

12 Source: SPDR Gold Trust. (2022, October 4). Prospectus: SPDR® Gold Trust (SPDR® Gold Shares) (Registration Statement No. 333-267520). U.S. Securities and Exchange Commission.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

GDMN: There are risks associated with investing, including possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political, or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic, or regulatory conditions affecting that country or region, or emerging markets generally. While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDE: There are risks associated with investing, including possible loss of principal. The Fund is actively managed and invests in U.S. listed gold futures and U.S. equity securities. The Fund’s use of U.S. listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDX: An investment in the Fund may be subject to risks which include, but are not limited to, risks related to investments in gold and silver mining companies, special risk considerations of investing in Australian and Canadian issuers, foreign securities, emerging market issuers, foreign currency, depositary receipts, small- and medium-capitalization companies, equity securities, market, operational, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount risk and liquidity of fund shares, non-diversified and index-related concentration risks, all of which may adversely affect the Fund. Emerging market issuers and foreign securities may be subject to securities markets, political and economic, investment and repatriation restrictions, different rules and regulations, less publicly available financial information, foreign currency and exchange rates, operational and settlement, and corporate and securities laws risks. Small- and medium-capitalization companies may be subject to elevated risks.

Investing involves substantial risk and high volatility, including the possible loss of principal. An investor should consider the investment objective, risks, charges and expenses of the Fund carefully before investing. To obtain a prospectus and summary prospectus, which contain this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.

GLD: Investing involves risk, and you could lose money on an investment in GLD.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Commodities and commodity-index linked securities may be affected by changes in overall market movements, changes in interest rates and other factors such as weather, disease, embargoes, or political and regulatory developments, as well as the trading activity of speculators and arbitrageurs in the underlying commodities.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs.

Diversification does not ensure a profit or guarantee against loss.

Before investing in a fund, consider it investment objectives, risks, charges, and expenses. A prospectus (and/or summary prospectus) containing this and other information is available by calling 1-866-787-2257 (ETFs and Mutual Funds) or 1-877-521-4083). Read it carefully.

The Marketing Agent for GLD, State Street Global Advisors Funds Distributors, LLC, is not affiliated with Foreside Fund Services, LLC, or WisdomTree, Inc.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.