GEOA

GeoAlpha Opportunities Fund

Published January 28, 2026

Global Head of Research

Macro Strategist, Model Portfolios

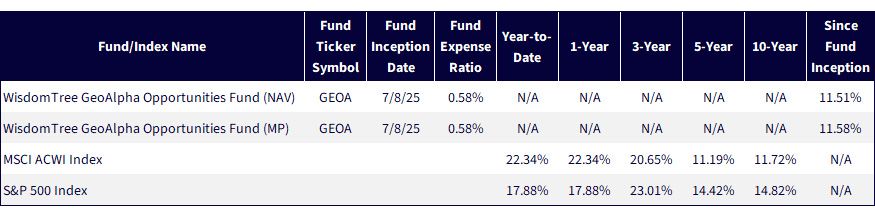

The WisdomTree GeoAlpha Opportunities Fund (GEOA) is up ~6.3% year-to-date. The S&P 500: roughly 1.0%. The MSCI ACWI Index: roughly 2.1%.1 GEOA's early lead in 2026 is large enough that it deserves a real explanation—and that explanation starts with how GEOA is built versus what the S&P 500 is forced to be.

Looking back to GEOA's inception, which we do in Figure 1a, we see a similar picture.

Figure 1a: Turning Geopolitical Complexity into Performance

Figure 1b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 1/23/26, but showing returns for the period ended 1/22/26 for Figure 1a and 12/31/25 for 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

The WisdomTree GeoAlpha Opportunities Fund targets exposure to companies that can capitalize on "emerging strategic and economic realignments" and as a tool for diversifying U.S.-centric allocations.

WisdomTree's GeoAlpha starts by screening the country universe to avoid "geopolitical traps," emphasizing alignment with the U.S. and its allies—North Atlantic Treaty Organization (NATO) members and major nonNATO allies—and explicitly naming Mexico (USMCA2) and India (QUAD3) as included exposures, while excluding countries viewed as not aligned with the U.S. and its allies. Stocks are then scored across geopolitical and policy themes such as supplychain resilience, with additional sleeves tied to fiscal/monetary shifts, consumer preference changes, and technology innovation. Simply, it is engineered to own the policy beneficiaries of a world where governments, security priorities, and trade rules increasingly influence where profits accrue.

The S&P 500 and MSCI ACWI indices are weighted by float-adjusted market capitalization, so the largest names by market cap do dominate outcomes. Current weight tables show that a small set of companies—Nvidia, Apple, Microsoft, Amazon, Alphabet, Meta (and a few others)—representing very large shares of the indices. When that cohort softens, the benchmark can look flat even if many other stocks are doing fine. That has been the narrative in early 2026. In a broadening market, a portfolio that is less dependent on a single U.S. mega-cap trade can look meaningfully better.

A core GeoAlpha idea is that geopolitical stress often turns into government spending—defense procurement, cybersecurity, secure communications, and industrial-base rebuilding. These tend to be multiyear programs and can persist even when consumer demand slows.

GEOA's holdings reflect that posture, including that when markets price in sustained budget-driven demand, those businesses can earn both (a) fundamental support for cash flows and (b) a ‘resilience premium' in risk-off periods.

But it is also companies tied to moving and modernizing physical supply chains—logistics and transport (e.g., UPS, Union Pacific) and industrial equipment/capital expenditure (capex) beneficiaries (e.g., Deere). If investors reward capex, reshoring/nearshoring, and redundancy (rather than purely digital growth), a portfolio holding the enablers can outperform a benchmark tilted toward the largest tech and communication-services names.

The bullish case for GEOA's relative edge against the MSCI ACWI and S&P 500 Index benchmarks is that several of its tailwinds are structural rather than quarterly:

GEOA's edge is durable whether market breadth continues to improve beyond a few mega-caps, defense and industrial-policy budget direction in the U.S. and allied nations remains supportive, or tariff and trade policy shifts.

GEOA's early 2026 outperformance is best understood as a portfolio-design story. It is a systematic, globally diversified basket of companies positioned for defense spending, allied reshoring, supply chain resilience, and strategic technology investment—precisely the areas that can lead when markets broaden beyond a few U.S. mega-caps. This is not ‘mega-cap growth at any price.’ The S&P 500 can retake the lead.

1 Sources: WisdomTree, FactSet, through the Fund Compare tool with data as of 1/22/26. Past performance is not indicative of future returns.

2 USMCA refers to the United States–Mexico–Canada Agreement.

3 QUAD refers to the Quadrilateral Security Dialogue, comprising the United States, Japan, India and Australia.

For current holdings of GEOA, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including possible loss of principal. The economic, political, regulatory and other events and conditions that affect issuers and investments in the United States differ significantly from those associated with other countries and regions. Any event or condition that affects the U.S. economy, whether originating from within or outside of the United States, may have an adverse effect on the Fund’s investments in the United States and thus, the Fund’s performance. Funds focusing their investments on certain sectors and/or regions increase their vulnerability to any single economic or regulatory development. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GeoAlpha Opportunities Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.