WTMF

Managed Futures Strategy Fund

Published May 1, 2026

Global Head of Research

For decades, portfolio construction has revolved around a simple constraint: you have 100% of a total allocation, and every new addition requires taking a portion from somewhere else. That constraint has shaped the dominance of 60/40 portfolios and the difficulty of incorporating alternatives without sacrificing expected return.

To provide asset allocators with a way around this issue, WisdomTree’s Efficient Capital framework launched in 2018 with the debut of the WisdomTree U.S. Efficient Core Fund (NTSX).

NTSX represented the practical implementation of an idea that had largely lived in institutional portfolios and academic journals for decades. By combining a 90% allocation to U.S. equities with a 60% exposure to U.S. Treasury futures, the strategy delivered approximately 150% notional exposure, effectively recreating a traditional 60/40 portfolio, doing so more efficiently, using less capital for the same notional exposure.

The innovation wasn’t leverage for its own sake. It was about solving a structural inefficiency in portfolio construction, thereby freeing up capital without giving up core exposures.

In doing so, NTSX marked a shift from thinking in terms of capital allocation to thinking in terms of exposure construction.

This leads to a fundamentally different question:

Not: what do we remove to add something new?

But: what can we add, once we separate capital from exposure? This is the second of three articles where we will introduce this efficient capital concept and then explore a particular option that could be added with the extra space.

We believe that one of the most compelling uses of that newly created portfolio “space” could be managed futures, an asset class designed to behave differently when traditional assets struggle.

At their core, managed futures strategies (often implemented by Commodity Trading Advisors, or CTAs) systematically trade futures across equities, rates, currencies and commodities, going both long and short to capture persistent market trends. This flexibility is critical. Unlike traditional assets, these strategies are not dependent on markets going up, and they are designed to extract returns from movement itself.

The empirical case is well established. A large body of academic and practitioner research has shown that managed futures, particularly systematic trend-following strategies, have historically exhibited low or even negative correlation to traditional asset classes like stocks and bonds.1

Since these strategies can go both long and short across global markets, they tend to perform best during sustained market moves, including during periods of stress. Research from AQR and others has demonstrated that trend-following strategies have delivered positive returns with ‘little correlation to traditional asset classes’ and often performed strongest during extreme equity market environments.2

This dynamic is often referred to as ‘crisis alpha,’ a term popularized following the Global Financial Crisis to describe the tendency of managed futures to generate returns during equity drawdowns. Empirical studies confirm that CTAs can provide meaningful diversification benefits specifically during crisis periods, helping offset losses elsewhere in a portfolio.3

Importantly, this comes at a time when traditional diversification has become less reliable. In periods of market stress, correlations across equities and even between stocks and bonds tend to rise, reducing the effectiveness of conventional portfolios. In that context, a strategy designed to thrive on dispersion and trends, rather than static allocations, becomes especially valuable.

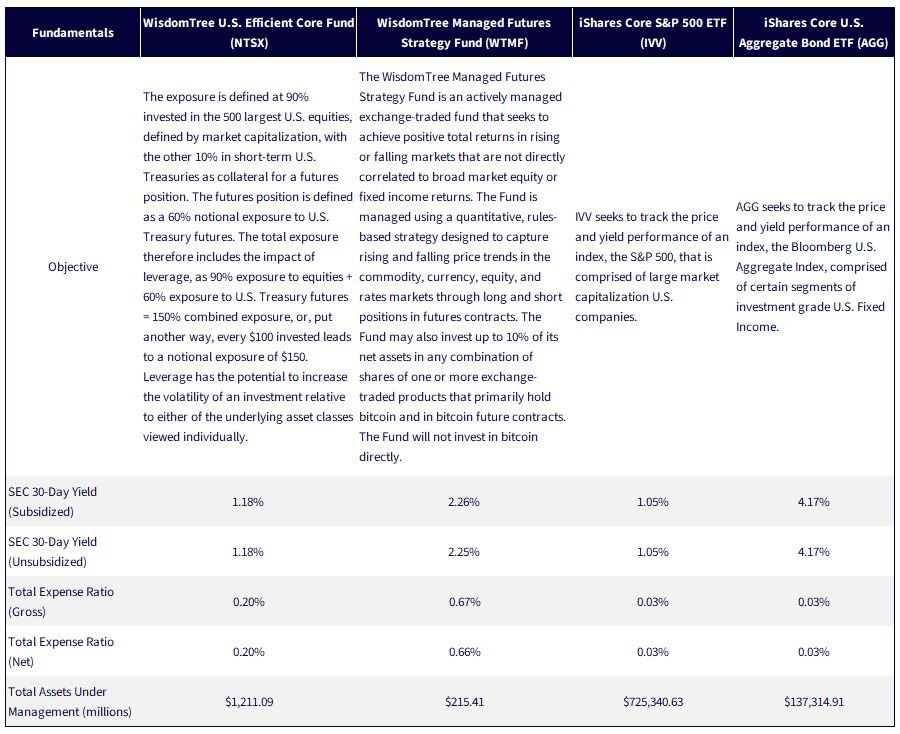

This is where the WisdomTree Managed Futures Strategy Fund (WTMF) fits within the Efficient Capital framework. WTMF implements a quantitative, rules-based approach to capturing price trends across global markets through long and short futures positions, seeking positive returns in both rising and falling environments.

In effect, if Efficient Core frees up space, managed futures offer a way to fill it with something structurally different—a return stream driven not by direction but by dynamics.

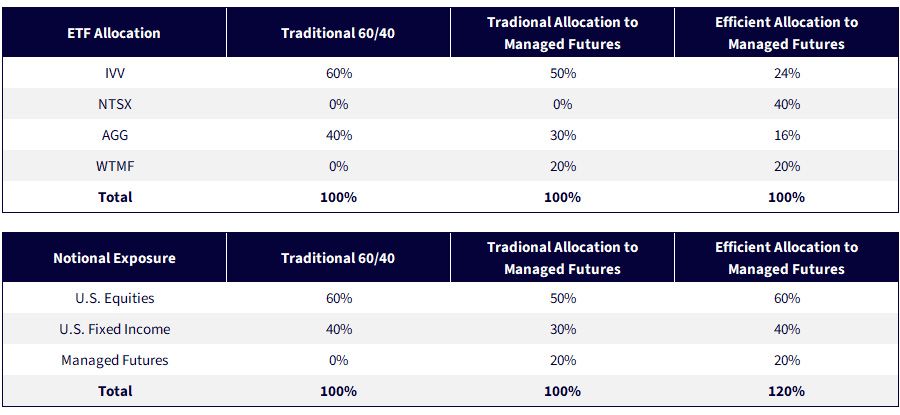

To make this more tangible, we can compare three ways of incorporating managed futures into a portfolio, but first, we must define our different ETF building blocks.

In Figure 1, the starting point is the ‘traditional 60/40’, 60% equities (IVV) and 40% fixed income (AGG). This serves as a familiar baseline, with 100% total notional exposure split between stocks and bonds.

From there is the ‘traditional allocation to managed futures’ approach, which introduces commodities by reallocating capital: 50% equities, 30% bonds and 20% managed futures (WTMF). This maintains 100% total exposure but requires reducing core equity and bond allocations to make room for the diversifier, in this case, managed futures.

The ‘Efficient Allocation to Managed Futures’ takes a different path.

Overall, the idea is to keep the 60% U.S. equities and 40% U.S. fixed income parts of the allocation intact, but to then add commodities over the top. Figure 1 shows how placing:

Leads to notional exposures of 60% U.S. equities, 40% U.S. fixed income and 20% managed futures.

This is the key distinction. The investor keeps the original allocation and adds a potential diversifier over the top.

Source: WisdomTree

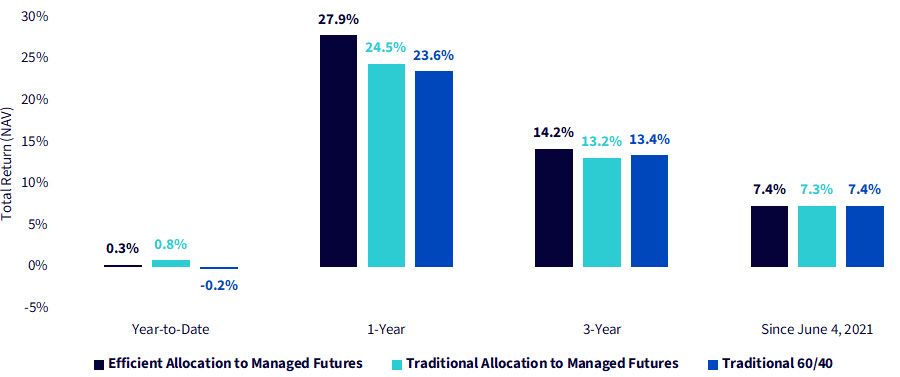

Looking at realized performance, the key question is whether this more efficient structure has actually translated into better outcomes.

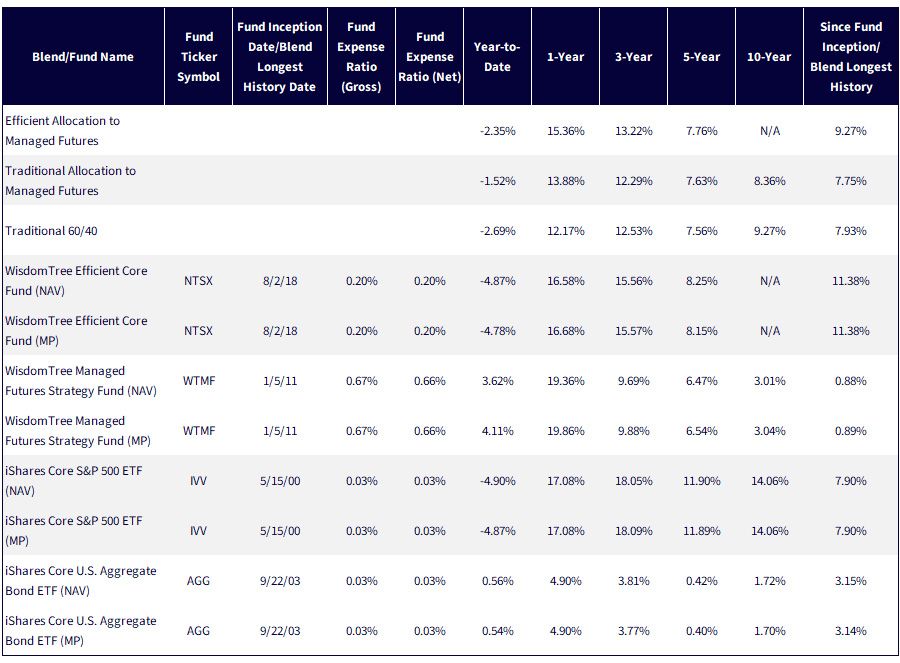

Over the available live history of the current strategy, the Efficient Allocation to Managed Futures, has generally delivered stronger returns than both the Traditional Allocation to Managed Futures and the Traditional 60/40. Over the past year, the Efficient Allocation to Managed Futures returned 27.9%, compared to 24.5% for the Traditional Allocation to Managed Futures and 23.6% for the traditional 60/40. Over three years, it again led at 14.2%, versus 13.2% and 13.4%, respectively.

Even in more challenging environments, such as the current year-to-date period, the Efficient Allocation to Managed Futures delivered 0.3%, which was comparable to the Traditional Allocation to Managed Futures (0.8%), and ahead of the Traditional 60/40 (-0.2%).

Figure 2b: Standardized Performance

Sources: Morningstar, FactSet and WisdomTree. Data is from the PATH Fund Comparison Tool, accessed as of April 10, 2026, but showing returns for the period ended April 8, 2026 for Figure 2a and March 31, 2026 for 2b. NAV denotes total return performance at net asset value. MP denotes market price performance. The Fund's strategy changed effective June 4, 2021. Prior to June 4, 2021, Fund performance reflects the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree Managed Futures Index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: NTSX,WTMF, IVV, AGG.

At its core, this is a shift in how portfolios are built. Managed futures offer a differentiated return stream, one that can diversify traditional assets and potentially add resilience during periods of stress. The challenge has always been implementation: how to incorporate that diversification without sacrificing core exposures.

Efficient Capital changes that equation.

By separating exposure from capital, investors are no longer forced into zero-sum trade-offs. Instead of replacing equities or bonds, they can add new sources of return alongside them. The result is a more flexible, more complete portfolio—one designed not just to participate in markets but to adapt to them.

Sources: Respect fund webpages for each respective ETF sponsor. Assets under management data is as of April 1, 2026. Subject to change.

Source: Lo, A. W., & Pedersen, L. H. (2014). Demystifying managed futures. Journal of Investment Management, 12(3), 42–58.

Source: Hurst, B., Ooi, Y. H., & Pedersen, L. H. (2017). A century of evidence on trend-following investing. The Journal of Portfolio Management, 44(1), 15–29.

Source: CME Group. (n.d.). Managed futures research digest.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

There are risks associated with investing, including possible loss of principal.

WTMF: An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors which contribute to the Fund's performance, as well as its correlation (or non-correlation) to other asset classes.

These factors include use of long and short positions in commodity futures contracts, currency forward contracts, swaps and other derivatives. In addition, bitcoin exchange-traded products (ETPs) and bitcoin futures are relatively new and the markets may be less developed. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. As a result, the markets for bitcoin futures and bitcoin ETPs may be less developed, and at times, potentially less liquid and more volatile, than more established commodity futures and ETP markets. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. Derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions.

The Fund should not be used as a proxy for taking long only (or short only) positions in commodities or currencies. The Fund could lose significant value during periods when long only indexes rise (or short only) indexes decline. The Fund's investment objective is based on historic price trends. There can be no assurance that such trends will be reflected in future market movements. The Fund generally does not make intra-month adjustments and therefore is subject to substantial losses if the market moves against the Fund's established positions on an intra-month basis. In markets without sustained price trends or markets that quickly reverse or "whipsaw" the Fund may suffer significant losses.

The Fund is actively managed thus the ability of the Fund to achieve its objectives will depend on the effectiveness of the portfolio manager. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. The Fund will not invest in bitcoin directly.

NTSX: While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. The Fund invests in derivatives to gain exposure to U.S. Treasuries. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. Interest rate risk is the risk that fixed income securities, and financial instruments related to fixed income securities, will decline in value because of an increase in interest rates and changes to other factors, such as perception of an issuer’s creditworthiness.

Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

For additional fund disclosures, please click the respective ticker: IVV, AGG.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.