Inflation fears meet higher yields

Rising yields overshadow inflation fears

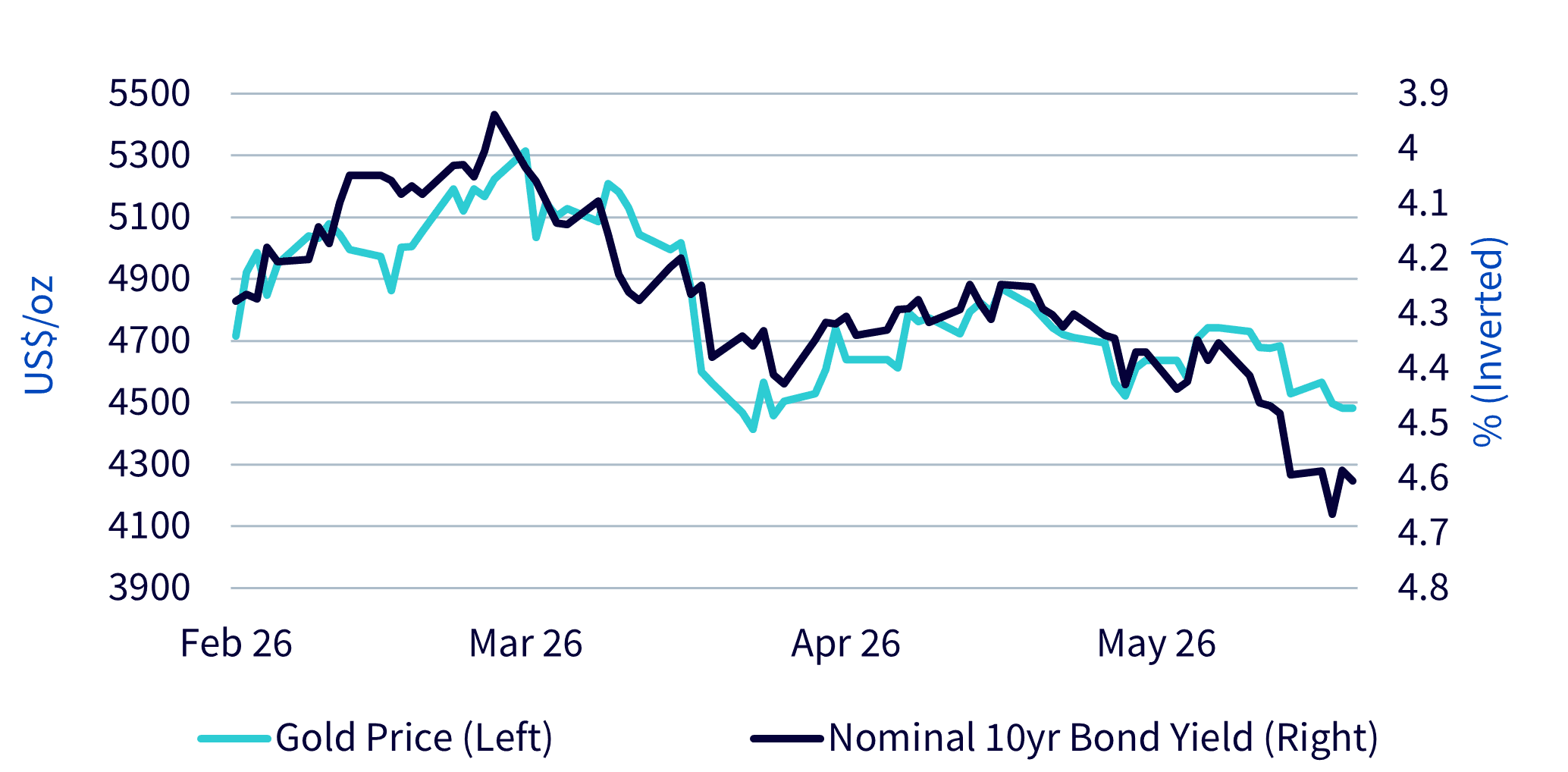

Gold weakened over the past month as a stronger US dollar and rising sovereign bond yields created headwinds for the metal. However, we continue to view these pressures as cyclical rather than structural and believe the medium-term backdrop for gold remains constructive.

The closure of the Strait of Hormuz has triggered broad commodity price disruptions across energy, fertilisers and industrial metals, driving a sharp rise in global inflation expectations. Central banks now face a difficult trade-off: monetary policy cannot resolve supply-side bottlenecks, yet failing to respond risks allowing inflation expectations to become unanchored.

As a result, markets have rapidly repriced interest rate expectations. In the United States, expectations for rate cuts have largely been removed, while markets are now pricing close to three additional hikes in the euro area and almost two in the United Kingdom for the remainder of the year. This repricing has pushed sovereign bond yields higher and created near-term pressure on gold prices.

In the US, the rise in yields has been concentrated at the long end of the curve, resulting in a bear steepening dynamic. This suggests investors are becoming increasingly concerned about persistent inflation, fiscal sustainability and rising term premia, even as expectations for the Federal Reserve policy rate remain comparatively stable. Rising long-term yields increase the opportunity cost of holding non-yielding assets such as gold.

Importantly, inflation itself should ordinarily support gold prices. However, when nominal and real bond yields rise simultaneously, the supportive effect of inflation can be offset, which is the environment currently facing the gold market.