Where Treasury & TIPS Yields May Be Headed

Published March 23, 2022

Kevin Flanagan

Head of Investment and Fixed Income Strategy

The March FOMC meeting confirmed one very important issue for the money and bond markets: rates are going to continue to go up. Through the prism of rate hikes and quantitative tightening, investors are trying to determine where Treasury (UST) yields will be going in the process.

According to the Fed’s “dot plot,” officials essentially see six quarter-point rate hikes for the remainder of this year. (It did not include the possibility of a 50 basis points (bps) rate hike, yet.) This would entail an increase at each FOMC meeting and would leave the target range for Fed Funds at 1.75%–2%. Then another four rate hikes could be on the docket for 2023, bringing the top end of the Fed Funds target range to 3%. Based upon recent comments from Chair Powell, it appears the potential exists for an even more aggressive rate hike path.

U.S. Treasury Yields

We all know that “past is not necessarily prologue” in the bond market, but history can offer some useful insights at times. And this may be one of those times. This is exactly why I took a look at where UST yields wound up during the Fed’s last rate hike cycle. As the graph clearly reveals, the 2-, 5- and 10-Year yields all coalesced around the 3% threshold toward the end of 2018.

Why is that so important, you may ask? Well, some market observers have mentioned that this year’s rise in UST yields already factors in further Fed rate hikes. I would say yes, but only to a certain degree. If the aforementioned Fed outlook plays out even close to script, UST yields will be moving into higher territory from their current readings. For some perspective, here’s where the UST 2-, 5- and 10-Year yields peaked in 2018, and if an encore performance does occur, how much further these yields would have to rise to get there:

- UST 2-Year peak 2.97%; +85 bps

- UST 5-Year peak 3.09%; +76 bps

- UST 10-Year peak 3.24%; +93 bps

In other words, additional increases approaching 100 bps in UST yields could be coming.

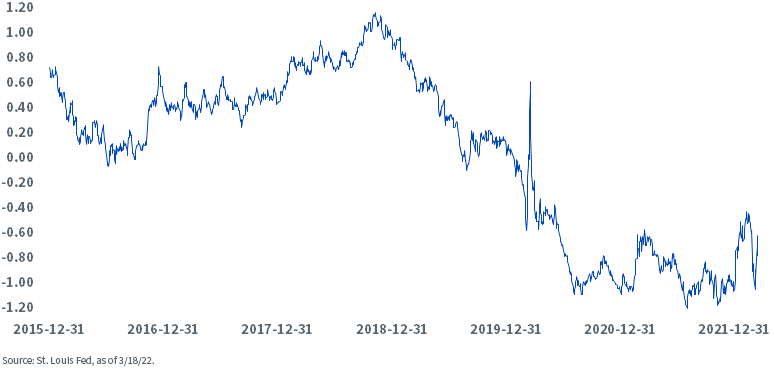

U.S. Treasury 10-Year TIPS Yield

The reason I’m including TIPS in the conversation is because they are often used as a rate hedge. BUT, as you’ll soon see, be careful what type of vehicle you choose for this assignment. Utilizing the same period as above, one discovers that 10-Year TIPS yields hit a peak of 1.17%. Given where its yield level was as of this writing, a move back to this high watermark would require an eye-opening increase of 180 bps.

Conclusion

As I mentioned in last week’s post Fed meeting blog piece, rising rates will likely not just be a 2022 phenomenon, but one that will play out in 2023 as well. Unfortunately for the bond investor, options are quite limited. However, there is one strategy that is actually designed for Fed rate hikes: floating rate Treasury notes (FRNs). These securities are offered in two-year maturities and are reset with the weekly three-month t-bill auction. As a result, the UST FRN yield “floats with the Fed.”

The WisdomTree Floating Rate Treasury Fund (USFR) offers investors a means to tap into this strategy and help mitigate the negative impacts to their bond portfolio from what could be looming ahead over the next two years.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. The issuance of floating rate notes by the U.S. Treasury is new, and the amount of supply will be limited. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

Related articles

A ‘Warsh’ Out at the Fed

Fed Watch: The Changing of the Guard Finally Arrives

Private Credit Beyond the Headlines: Why Diversification and Liquidity Matter More Than Ever

Are Bessent’s Hands Tied?

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.