When Imagination Runs into Physics

Published May 12, 2026

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- As AI shifts from training to inference, investors are increasingly focused on infrastructure—memory, optics and power—where physical constraints are driving durable demand.

- The transition from copper to optical networking and rising AI energy needs are creating tailwinds for semiconductor, fiber optic and grid infrastructure companies.

- Despite software volatility in 2026, the WisdomTree Artificial Intelligence and Innovation Fund (WTAI) maintains balanced exposure to both AI infrastructure leaders and enterprise software platforms positioned for long-term adoption.

Same Theme, Different Maps

Artificial intelligence, at its core, is a physics problem. It needs memory that moves data fast enough to keep transformers fed. It needs interconnects that can carry information across distances that copper simply cannot handle efficiently. It needs power, more of it, more reliably, than most grids were built to supply. When imagination runs into physics, physics wins. And the companies that resolve those physical constraints tend to be more durably valued than software names whose stories depend on sentiment and timing.

That thesis is increasingly showing up in how serious AI funds are being constructed. Comparing the current holdings of BlackRock’s iShares A.I. Innovation and Tech Active ETF (BAI) and the WisdomTree Artificial Intelligence and Innovation Fund (WTAI) reveals two portfolios that have independently converged on the infrastructure layer as the most defensible place to be, while diverging, meaningfully, on just how concentrated and how far down the supply chain that conviction should run.

WisdomTree has been tracking the universe of thematic ETFs going back to 2021. In the ‘Artificial Intelligence & Big Data’ category, BAI is the largest strategy on the basis of assets under management, which brings it into focus here.

The Shared Foundation: Infrastructure Over Hype

Before examining the differences, it is worth noting the overlap. Both funds have pivoted in the same conceptual direction. As AI spending shifts from training to inference, the physics of the problem, including memory bandwidth, interconnect speed, packaging complexity, and power availability, become the real constraints. Capital follows constraints, and the companies that resolve them tend to be more durably valued than application-layer software names whose valuations depend heavily on sentiment.

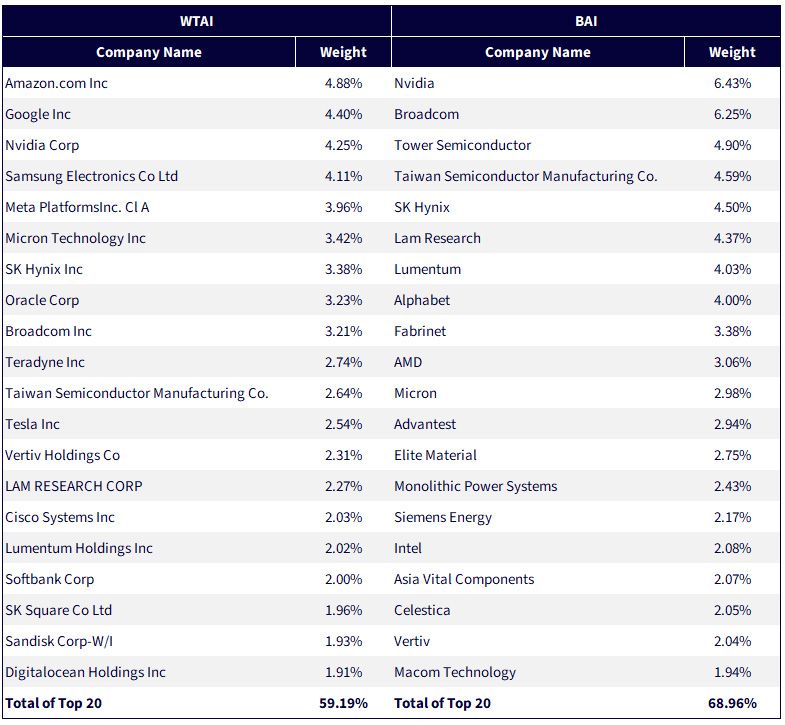

Figure 1: Top 20 Holdings at a Glance

Where the Two Funds Agree—and How Far Each Takes It1

Optical Connections

For years, the servers inside AI data centers communicated over copper wire. Copper is inexpensive and familiar, but AI clusters operate at a scale and speed it was never designed to handle. The more servers you connect and the longer the cables run, the more the signal degrades, and the more heat you generate pushing data through copper at high speed, which itself becomes an engineering problem requiring yet more power to cool.

Optical interconnects solve this by replacing electrons with photons. Light pulses traveling through glass fiber move faster, carry more data per unit of energy, generate less heat, and hold signal integrity over longer distances. As AI infrastructure scales from individual server racks to multi-building campuses and eventually multi-site distributed clusters, the physics simply favor light over electricity. This is not a future transition—it is happening now.

Both funds own this theme. WTAI holds Lumentum (2.02%) and Corning (1.08%), while BAI has taken a more concentrated position in Lumentum (4.03%) and added Fabrinet (3.38%), a contract manufacturer that produces the precision optical assemblies Lumentum and others design. BAI is treating optics as a defining overweight; WTAI is treating it as one important theme among several. Importantly, the directional conviction is shared, and the reasoning is the same: bandwidth is a binding constraint and the companies resolving it are moving from a supporting role in the data center to a central one.

Power and Infrastructure

There is a constraint on AI deployment that does not appear in semiconductor roadmaps or memory specifications, and it may be more binding than any of them right now: electricity.

Training a large language model consumes roughly the energy of hundreds of homes in a year.2 Inference, serving that model to millions of users, continuously, never stops. Data center operators are increasingly finding that the limiting factor on expansion is not capital, not chips and not real estate. It is reliable power, in sufficient quantity, delivered to the right place.

Both funds have exposure here. WTAI holds GE Vernova (1.00%) and Schneider Electric (1.56%), two companies deeply embedded in grid infrastructure and data center power management respectively. BAI builds out a broader picture, including such companies as:

- Siemens Energy (2.17%) addresses the grid itself, including the transformers and high-voltage transmission systems that move power from where it is generated to where AI campuses are being built—locations that are increasingly not the same.

- Delta Electronics (1.74%) brings the story inside the facility, making the power conversion and thermal management equipment that sits between the utility connection and the servers.

- Advanced Energy Industries (1.78%) connects power infrastructure to semiconductor manufacturing, supplying precision power systems to the fabrication equipment that produces AI chips.

- BWX Technologies (1.76%) represents the longer horizon—a nuclear reactor manufacturer whose small modular reactor work reflects a serious bet that always-on, carbon-free baseload power will be part of how the data center industry solves its energy problem at scale.

The underlying thesis is the same in both portfolios: energy availability is a structural constraint on AI deployment, not a temporary inconvenience.

The Memory Trade: A Key Point of Agreement

The shift from GPU-centric training to inference at scale changes the memory equation materially. High-bandwidth memory (HBM) was the first wave; now standard DRAM3 and NAND4 are becoming increasingly important as the KV-cache5 memory wall, which is the growing compute burden of tracking context in transformer models, pushes demand further down the memory stack.

Both funds hold SK Hynix and Micron as significant positions. WTAI adds Samsung (4.11%), SanDisk (1.93%), and Kioxia (1.21%) to build out a comprehensive view of the memory ecosystem. BAI holds Western Digital (1.44%) and SanDisk (1.36%), signaling similar awareness of the NAND opportunity. On this particular thesis, the two funds are essentially aligned.

The Software Question

Everything discussed so far, particularly memory, optics and power, represents examples of AI infrastructure. It is the part of the AI trade where the spending is visible, the contracts are signed, and the revenue is, in many cases, already flowing. Both funds are there, in varying degrees of concentration.

Where they genuinely diverge is on software.

WTAI carries meaningful software exposure, roughly 16% of the portfolio, and it is not accidental. Example companies include ServiceNow, Palo Alto Networks, Snowflake, MongoDB, Salesforce, Datadog and CrowdStrike.

These are names that have been central to enterprise technology for years, and WisdomTree's view is that their AI monetization story, while slower to materialize than the infrastructure buildout, is real. The rebalance trimmed the weakest links to what was a broader overall exposure to software, particularly more seat-based software-as-a-service (SaaS) companies with vague AI timelines, but kept the names with direct claims on AI deployment: security platforms, data infrastructure, enterprise automation systems that sit closest to where AI outputs actually get used.

BAI has largely stepped away from this part of the market. Its software exposure is minimal, concentrated in a small number of names, and clearly not a focus of the portfolio's construction. With the volatility that we have seen in software to start 2026, some might view this as prescient.

Both positions are defensible. The infrastructure bull case is grounded in capital expenditure data that is hard to argue with. The software bull case is grounded in the observation that infrastructure buildout, at some point, has to convert into application-layer revenue, and the companies best positioned to capture that revenue are the ones already embedded in enterprise workflows. The honest answer is that nobody knows whether that conversion happens in twelve months or four years, and the difference in timing is the difference between these two portfolios being right or wrong on this specific bet.

Conclusion: A Thesis Is One Thing, Performance Is Another

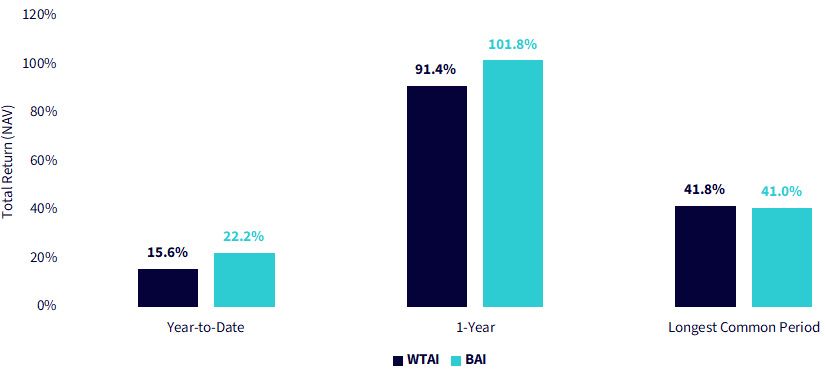

Looking at the period ‘year-to-date’ which references 2026 through April 17, it is not surprising to see BAI ahead of WTAI. WTAI has had more software exposure and continues to have more software exposure. This has been a volatile area in markets. The 1-Year period also has some of this impact. It is also true that there is huge emphasis on the transition from using copper to send signals in the data center to using glass and ultimately light to do so. BAI has been well-positioned there, devoting more of its portfolio’s overall exposure to the theme.

But if we look at the longest common period, which also reminds us that BAI was only incepted in October 2024, the picture is extremely close. As we move forward, we have enumerated the most consequential exposure difference, and based on what we can see today if software names rally, WTAI may be in a better position. If the volatility within software continues, this could favor BAI.

It’s always exciting to break down how two strong strategies are approaching a topic, and we look forward to continuing to track this as the picture continues to evolve.

Figure 2a: What the Short Period of Live Performance has Shown

Figure 2b: Standardized Returns

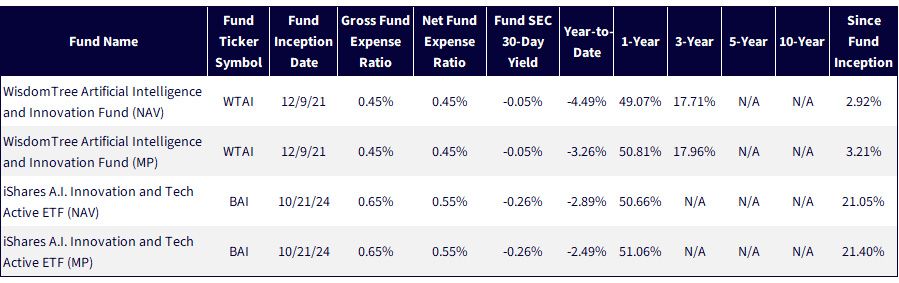

Sources: Morningstar, FactSet and WisdomTree, specifically, data is from the PATH Fund Comparison Tool, accessed as of April 20, 2026, but showing returns for the period ended April 17, 2026 for Figure 2a and March 31, 2026 for Figure 2b. NAV denotes total return performance at net asset value. MP denotes market price performance. The longest common period goes back to the inception date of BAI, in this case 10/21/2024. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: WTAI, BAI.

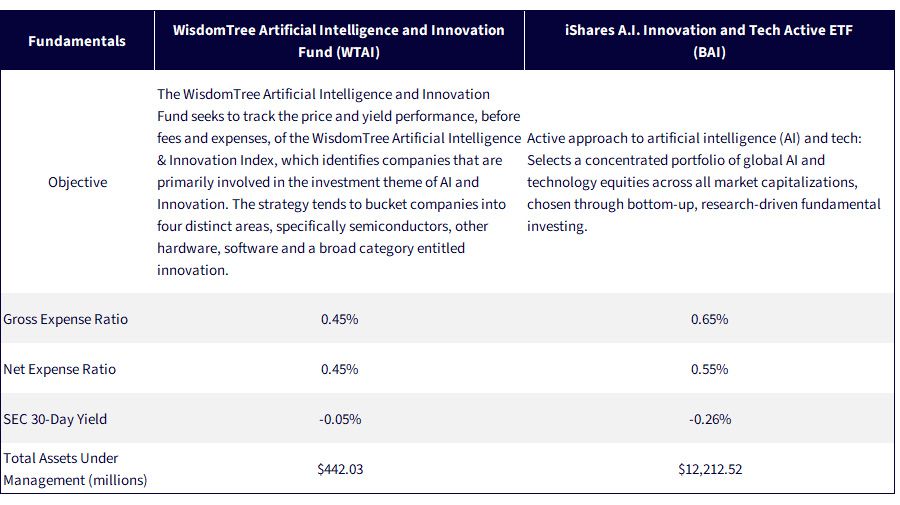

Figure 3: Additional Information

Sources: Respective fund sponsor web pages, with data for assets under management measured as of April 17, 2026. Subject to change.

- As different companies are discussed and weights are specified, the source for constituents and weights is the same as in Figure 1, the specific company websites, and the as of date for data is as of April 17, 2026.

- Source: Patterson, D., Gonzalez, J., Le, Q., Liang, C., Munguia, L.-M., Rothchild, D., So, D. R., Texier, M., & Dean, J. (2021). Carbon emissions and large neural network training. arXiv.

- Stands for dynamic random access memory.

- Stands for Not-And, logical operations, and a shorthand to reference solid state memory.

- The KV-cache is a feature of transformer models, which underlie most large language models in 2026, and refers to how each new token needs to be mapped onto the full context of what was discussed previously in terms of a ‘key’ and a ‘value’ to relate the new tokens to the existing tokens such that responses continue to make sense to the user.

Source: Patterson, D., Gonzalez, J., Le, Q., Liang, C., Munguia, L.-M., Rothchild, D., So, D. R., Texier, M., & Dean, J. (2021). Carbon emissions and large neural network training. arXiv.

Stands for dynamic random access memory.

Stands for Not-And, logical operations, and a shorthand to reference solid state memory.

Important Risks Related to this Article

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

There are risks associated with investing, including possible loss of principal. The Fund invests in companies primarily involved in the investment theme of Artificial Intelligence (AI) and Innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on Innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For BAI’s risk disclosures, click here.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.