Capturing the Evolving AI Landscape: WTAI’s November 2025 Rebalance through Five Core Pillars

Published December 12, 2025

Christopher Gannatti, CFA

Global Head of Research

Blake Heimann

Senior Associate, Quantitative Research

Key Takeaways

- As AI infrastructure demand surges, the November 2025 rebalance of the WisdomTree Artificial Intelligence and Innovation Index sharpened its focus on companies delivering real compute power, including NVIDIA and leading hyperscalers like Alphabet, Amazon and Oracle.

- With memory and networking becoming new bottlenecks, the Index added exposure to firms like SK Hynix, Broadcom and Astera Labs, all critical to AI scalability.

- WTAI is shifting away from speculative AI narratives and toward firms driving measurable adoption, such as ServiceNow, CrowdStrike and Snowflake, reflecting a more disciplined, software-oriented investment thesis.

Artificial intelligence is no longer a single theme; it is a technology ecosystem spanning more of the global economy every day. It stretches from graphics processing units (GPUs) and high-bandwidth memory to cloud infrastructure, data pipelines, observability platforms, enterprise software and security layers. Each part is scaling at its own pace. Each part has its own bottlenecks. And each part contributes differently to the companies positioned to benefit from AI's growth.

The November 2025 rebalance of the WisdomTree Artificial Intelligence and Innovation Index—which the WisdomTree Artificial Intelligence and Innovation Fund (WTAI) seeks to track—reflects this reality.1 The most recent rebalance is best reflected through five key pillars that we believe are shaping how the AI landscape is evolving right now as we approach the end of 2025.

Pillar 1: Compute Scale Remains the Dominant Bottleneck

If AI had a unifying message in 2024–2025, it was this: There is a compute shortage, and it is real. The companies building data centers today aren't speculating on future customers. They are serving current, visible, overwhelming demand.2 Therefore, it is fitting that the most meaningful weights in the strategy sit inside the compute layer.

NVIDIA: Conviction That Remains

NVIDIA has remained among the top exposures, with a weight of 4.50%. Why?

- AI compute demand continues to outstrip supply.

- NVIDIA maintains unmatched ecosystem depth—CUDA,3 networking, inference optimization, full-stack system design.

- Blackwell demand signals show that GPU scarcity will remain a pricing and margin tailwind.

This is not a case of "sticking with what worked." It's a case where every data point reinforces the view that NVIDIA continues to compound its advantage.

Hyperscaler Infrastructure: Alphabet, Amazon, Oracle

To power large-scale models, you need AI-optimized cloud, inference endpoints and the ability to deploy and scale large language model (LLM) workloads for enterprise customers.

This is why each of the following names was among the top weights:

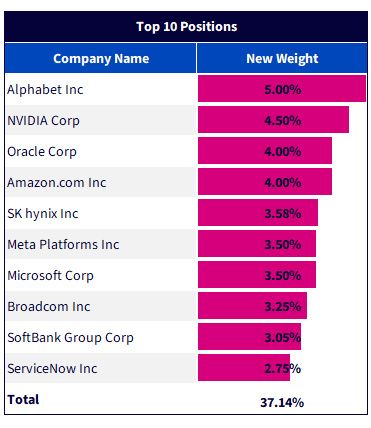

- Alphabet (GOOGL): 5.00%

- Amazon (AMZN): 4.00%

- Oracle (ORCL): 4.00%

Each provides leverage to different aspects of compute infrastructure buildouts:

- Google: training + inference at scale, Gemini's continued improvement, AI-native distribution and their proprietary tensor processing unit (TPU).

- Amazon: AWS's foundational role in enterprise compute, model-hosting economics and accelerating AI workload mix.

- Oracle: rapid AI infrastructure deployments, emerging operating leverage and a pipeline of future revenue tied to model hosting and cloud demand.

Oracle, in particular, has been getting tested by markets in late 2025—debt financing, forward obligations and reliance on customers still scaling profitability are common talking points. But for an informed AI investor, none of this is surprising. The real question is where model capability is moving. If AI becomes "slightly better software," then the thesis breaks. But if scaling remains intact—and recent Gemini results suggest it does—then hyperscaler infrastructure is still early.4

Pillar 2: Memory andNetworking Matter More Than Ever

As AI models grow larger and more complex, GPUs are no longer the only constraint. Memory and networking are becoming more structural bottlenecks.

AI workloads require:

- DRAM/HBM: the ultra-fast working memory that feeds GPUs data in real time. DRAM stands for "dynamic random access memory." HBM stands for "high bandwidth memory."

- NAND: the storage layer for training data, checkpoints, vector databases and model files. NAND stands for "not-and" and is designed to keep data even when the power is off.

AI cannot scale without both. Every new NVIDIA architecture requires more memory per chip, not less.5 HBM and NAND shortages are now delaying system deployments as the industry experiences a supply crunch. Key suppliers of these memory chips are SK Hynix, Micron and Samsung, with weights at 3.58%, 2.66% and 1.5%, respectively.

Networking: The Quiet Enabler of Scaling

GPU clusters don't work without high-speed coherency. To train large models, thousands of GPUs need to communicate as if they are a single machine, synchronizing data and computations in real time. That coordination doesn't just happen within a server, but across racks, entire data center halls and, in some cases, multiple facilities. Delivering that kind of bandwidth and low-latency requires specialized switches, optical interconnects and high-performance cabling: domains led by companies like Broadcom (3.25%), Marvell (2%), Credo (1%) and Astera Labs (1.14%). As AI continues to scale, so do these firms.

In figure 1, you see these pillars reflected within the new weights of the top 10 positions.

One name worth calling out is Meta Platforms. Our standpoint is that there are certain companies, and Meta is one, using AI to enhance their existing businesses, in this case, advertising and content recommendation. As investors search for more linear and direct connections that are AI-specific, we think they might under-appreciate taking new AI technologies and bringing them back to existing profit engines. Advertising and content recommendation has been one of the world's best business models in recent years, and we see differentiated AI capabilities continuing to be an advantage here.

Figure 1: Anchored in Infrastructure, 10Firms Driving AI at Scale

Source: WisdomTree. References the rebalance target weights for the WisdomTree Artificial Intelligence & Innovation Index as of the rebalance that was effective after the market's close on 11/21/25. Subject to change.

Pillar 3: Enterprise AI Adoption Is Finally Real

For years, enterprise AI lived in the realm of promising demos and incremental productivity tools. In 2025, that changed. Companies are finally generating real revenue uplift from AI workflows, copilots, recommendation systems and data-layer integration.

ServiceNow (2.75%)

ServiceNow's Now Assist platform is turning enterprise workflows into automated, AI-driven systems, delivering measurable productivity and cost savings.6 As companies adopt agentic operations, ServiceNow's broad embedded AI footprint gives it one of the strongest monetization runways in enterprise software.

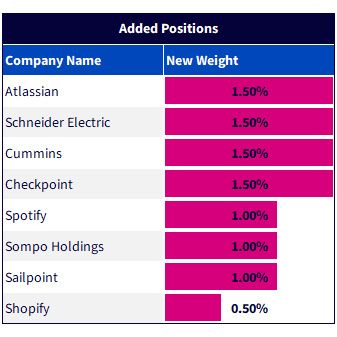

Atlassian (+1.50%, Addition)

Developer workflows are rapidly integrating AI copilots, debugging tools and code recommendations. More code is now written by AI than by humans.7 This warrants more developer tools and pipelines to keep code bases organized and bug-free. Atlassian sits inside these workflows, giving it early leverage to generative AI productivity.

Shopify (+0.50%, Addition)

AI is already transforming merchandising, logistics and storefront optimization—and Shopify sits at the center of that shift. Its data flywheel positions it to monetize AI-driven insights for merchants, especially as LLMs reshape how consumers search for and purchase products.

Snowflake (2.00%)

Snowflake continues to be the backbone for data pipelines, vector database integrations and the enterprise AI data layer. The company's native LLM integrations give it leverage as AI adoption accelerates.

Salesforce: (1.00%)

Agentforce brings autonomous agents into frontline workflows, while Data Cloud unifies enterprise data to power them. Enterprises want AI embedded in the workflows they already use, and Salesforce is delivering exactly that.

The story here is clear: Enterprise AI is no longer an idea—it is a budget line. The rebalance acknowledges where that spend is landing.

In figure 2, we see the additions. Atlassian and Shopify are there, as are Sailpoint and Checkpoint, two cybersecurity companies emblematic of our next pillar.

We'd also note Schneider Electric and Cummins for their key positions in building out the energy grid, another important AI bottleneck, and Sompo Holdings, which is a very interesting Japanese insurance conglomerate that uses AI to enhance the services it can provide to an aging population. Sompo has also historically been a user of Palantir's software to get the AI job done and is improving expense and loss ratios, indicating improved efficiency and profitability.

Figure 2: Anchored in Software & Security, Firms Expanding the Index’s Innovation Exposure

Source: WisdomTree. References the rebalance target weights for the WisdomTree Artificial Intelligence & Innovation Index as of the rebalance that was effective after the market's close on 11/21/25. Subject to change.

Pillar 4: Cybersecurity Is a First-Order AI Theme

As AI scales, so does the cybersecurity threat environment. AI increases the attack surface, accelerates the speed of threats and amplifies the complexity of securing cloud environments.

CrowdStrike: 2.00%

CrowdStrike's AI-native approach to threat detection and its soaring net retention make it one of the most important security platforms for the AI era.8

Datadog: 1.50%

Observability is now mission-critical. AI workloads create more risk, requiring more logs and more distributed services to monitor. Datadog is indispensable for running AI systems in production at scale.

Palo Alto Networks: 2.50%

Palo Alto sits at the intersection of cloud security posture, networking visibility and AI governance. Its relevance increases with every enterprise AI deployment, and it is particularly appealing to firms looking for a one-stop solution at the cutting edge.

This is not a cyclical subtheme but a structural reality: AI adoption and security demand rise together as data and attack surfaces scale with the technology.

Pillar 5:Avoiding the Noise

A final "bonus pillar" of the rebalance centers on staying disciplined amid the noise surrounding AI. The ecosystem includes companies where AI does not yet play as direct a role in revenue as commentary may suggest, where competitive pressures are increasing or where valuations have moved well ahead of fundamentals. While many of these firms continue to invest meaningfully in AI, their economic linkage is less immediate, and the strategy reflects that with measured adjustments. The full list of drops can be found on the WisdomTree Index Reconstitution page. The most notable of these drops is Tesla, which remains focused on AI, but its valuation still embeds a substantial narrative premium relative to underlying fundamentals. We will continue to evaluate names like these in each rebalance as the evidence develops.

The philosophy is simple, yet important: WTAI is increasingly a bet on measurable AI adoption, measurable AI infrastructure and measurable AI revenue leverage—not on speculative future states. If volatility rises, the Index is positioned to hold the companies capturing real spend rather than those caught in narrative drift.

Closing Thought: AI Is Spreading, but Conviction Is Sharpening

The most important evolution in WisdomTree's AI thinking is this: AI is no longer a theme—it is a system. And systems reward precision.

The November 2025 rebalance was designed with that mentality. It is not about chasing headlines or trying to predict which frontier model will capture the zeitgeist. It is about:

- identifying the parts of the stack where capital must flow,

- concentrating toward the companies with real leverage to that spend

- and maintaining a disciplined posture toward valuation, durability and adoption curves.

AI is now entering a more operational, more infrastructural and more enterprise-driven phase. The newest expression of WTAI is built to meet that moment—with clarity, with conviction and with the five pillars at its core.

1 The rebalance of the WisdomTree Artificial Intelligence & Innovation Index was effective as of the market's close on November 21, 2025. After that date, market performance may cause the weights in the strategy to differ from figures presented throughout this piece, which would be the initial targets as of the rebalance.

2 Source: K. F. Pilz, Y. Mahmood and L. Heim, "AI's power requirements under exponential growth: Extrapolating AI data-center power demand and assessing its potential impact on U.S. competitiveness" (RR-A3572-1), RAND Corporation, 2025.

3 CUDA stands for Compute Unified Device Architecture. It is NVIDIA's parallel computing platform and programming model that allows developers to run general-purpose computations on GPUs (GPGPU computing).

4 Source: S. Pichai, "A new era of intelligence with Gemini 3" [blog post], Google, 11/18/25.

5 Sources: "NVIDIA H100 80GB PCIe GPU | Hopper Gen 5 Tensor Core" [product page], TensorGear, 2025; "NVIDIA HGX B200, GB200, B300 and GB300s" [product overview], Voltage Park, 2025.

6 Source: ServiceNow, "ServiceNow unveils the new ServiceNow AI Platform to put any AI, any agent, any model to work across the enterprise," Business Wire, 5/6/25.

7 Source: J. Fay, "AI is generating code at scale — but human-scale code review can't keep up," DEVCLASS, 6/19/25.

8 Source: "CrowdStrike Signal delivers the next evolution of AI-powered threat detection" [press release], CrowdStrike, 8/6/25.

Important Risks Related to this Article

For current holdings of WTAI, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributors

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Blake Heimann

Senior Associate, Quantitative Research

Blake Heimann joined WisdomTree in 2020 and, in his current role as Senior Associate, supports the creation, maintenance, and reconstitution of our indices. Blake began his career in finance in 2017 as an Analyst at TD Ameritrade, and later a Quantitative Analyst with focuses on research and development of machine learning applications in finance. Blake has bachelor’s degrees in Mathematics and Economics from Iowa State University, as well as his Masters in Computer Science at Georgia Tech, with a specialization in Machine Learning. He is currently pursuing a Masters in Finance from the London School of Economics.