Value Investing That's Worked

Published December 22, 2025

Matt Wagner, CFA

Director, Research

Key Takeaways

- As investors grow wary of AI-driven mega-cap concentration, the WisdomTree U.S. Value Fund (WTV) offers a compelling alternative with a shareholder yield of 7.1%, nearly triple that of the S&P 500 Index.

- WTV's disciplined, rules-based approach favors companies returning capital to shareholders, helping it outperform the S&P 500 by 1% annualized over the past five years despite avoiding the “Mag 7” giants.

- With just 16% overlap with the S&P 500 and a portfolio rooted in cash-flow discipline, WTV provides true diversification for investors seeking value beyond traditional benchmarks.

Three consecutive years of dominance from growth, momentum and the "Mag 7" have put valuations at the forefront of investor concerns heading into 2026.

The U.S. market increasingly feels like a concentrated and pricey bet on the future of AI. But outside of mega-cap tech, there are broad pockets of the market trading at levels that don't look stretched compared to history.

Take the WisdomTree U.S. Value Fund (WTV). The Fund is designed to identify companies trading at a relative-value discount, based on returns of capital to shareholders through dividends and buybacks.

Diversifying away from the market's most expensive names doesn't have to mean underperformance. Over the last five years, as of November 30, 2025, WTV outperformed the S&P 500 by 1% annualized.

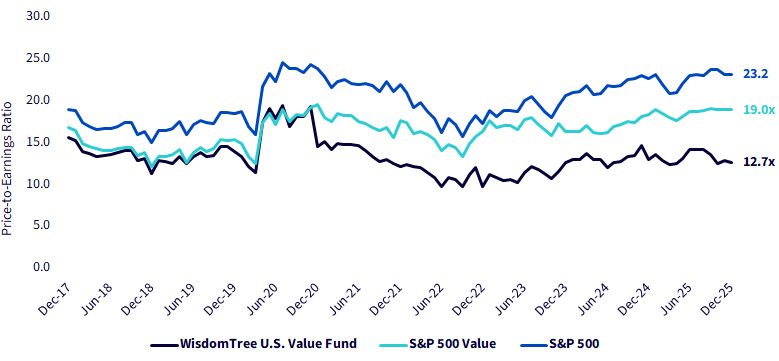

Forward Price-to-Earnings Ratio

Sources: WisdomTree, FactSet, S&P, 12/31/17–12/3/25. Period chosen to coincide with the start of the shareholder yield-focused investment process of the WisdomTree U.S. Value Fund in December 2017. You cannot invest directly in an index.

What Makes WTV Different

Most value strategies rely on accounting-based valuation ratios—price-to-earnings, price-to-sales and price-to-book. These metrics can be distorted by differences in accounting treatment across companies and industries, as well as by the growing role of intangible assets that are often absent from financial statements.

To avoid these distortions, many investors have shifted toward cash-flow-focused approaches that better capture a company's true economic earning power. Shareholder-yield strategies take this a step further by not only identifying companies with strong cash generation but prioritizing those that directly return that cash to investors through dividends and buybacks.

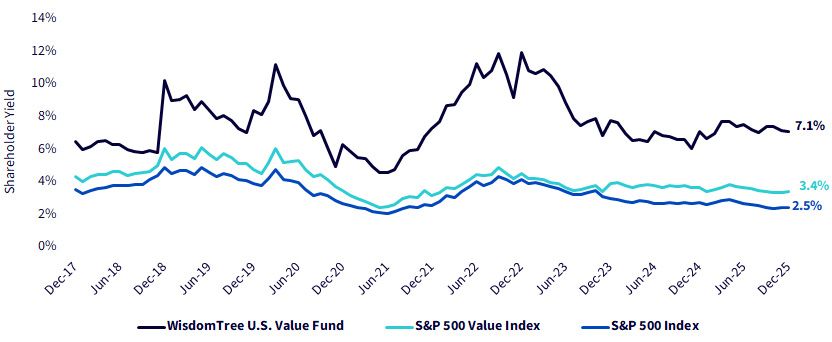

As of December 3, 2025, WTV's shareholder yield stands at 7.1%, compared with 3.4% for the S&P 500 Value Index and 2.5% for the S&P 500 Index. Even before considering any multiple expansion or earnings growth, WTV begins with a 3.7%–4.6% annual advantage in cash returned to shareholders. All else equal, that higher baseline yield can be a powerful tailwind for long-term performance expectations.

Total Shareholder Yield

Sources: WisdomTree, FactSet, S&P, beginning 12/29/17. Period chosen to coincide with the start of the shareholder yield-focused investment process of the WisdomTree U.S. Value Fund (WTV) in December 2017. You cannot invest directly in an index.

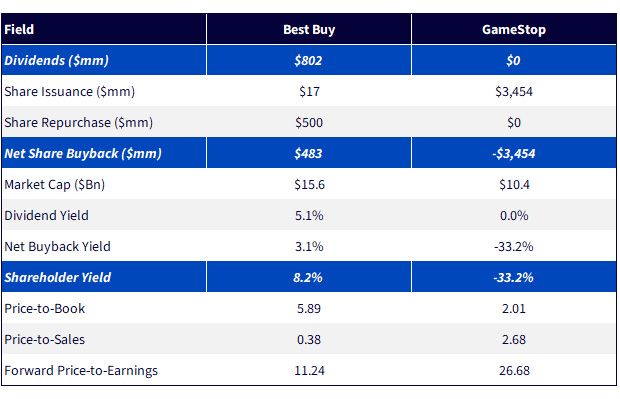

Consider two companies:

- Best Buy returned roughly 8% of its market capitalization to shareholders in dividends and buybacks—about $802 million in dividends and $483 million in net share repurchases.

- GameStop, by contrast, issued nearly $3.5 billion in new shares, paid no dividends and executed no buybacks, resulting in a –33% shareholder yield (i.e., the company issued equity equal to one-third of its market cap).

As of December 3, Best Buy was a 0.98% weight in WTV, while GameStop was not included in the portfolio.

Shareholder Yield Comparison

Sources: WisdomTree, FactSet, as of 12/3/25

Companies as the Market's Best Investors

A recent Economist article, "Who Are the World's Best Investors?", highlighted decades of academic research showing that companies themselves are often the market's most effective investors.

Research over the past 25 years—including studies by Baker & Wurgler (2000), Pontiff & Woodgate (2008) and McLean et al. (2022)—documents a simple, consistent pattern:

- When firms repurchase stock, their shares tend to outperform.

- When firms issue stock, subsequent returns tend to lag.

In aggregate, corporate CFOs have shown a remarkable ability to buy low and sell high—unsurprising given their real-time visibility into their businesses.

WTV systematically seeks to harness that signal, owning the steady capital returners and avoiding the serial diluters.

A Rules-Based Active Approach

WTV is a rules-based, active ETF.

The quantitative model behind the Fund starts with roughly 800 U.S. large- and mid-cap companies and applies three primary quantitative filters:

- Remove value traps using a composite risk score emphasizing profitability, leverage and earnings quality.

- Exclude share diluters—companies issuing more stock than they repurchase.

- Select the top 30% ranked by shareholder yield.

At the last quarterly rebalance in early December, 121 stocks were included in the portfolio.

Source: WisdomTree, as of 10/31/25, the last quarterly screening date of the portfolio.1 Starting universe and post-screen basket are market cap-weighted.2 Final portfolio constituents are initially weighted based on shareholder yield, with considerations to constrain turnover and sector over- and under-weights. Rebalances typically occur quarterly. Subject to change.

The portfolio is primarily weighted by shareholder yield. Some adjustments from shareholder yield weighting include maintaining weights of securities held at rebalance and including partial market cap-weighting—25% of overall weighting at the latest rebalance.

This "rules-based, active" design preserves transparency and discipline while maintaining flexibility to rebalance quarterly, or more frequently, as fundamentals evolve.

A Truer Form of Diversification

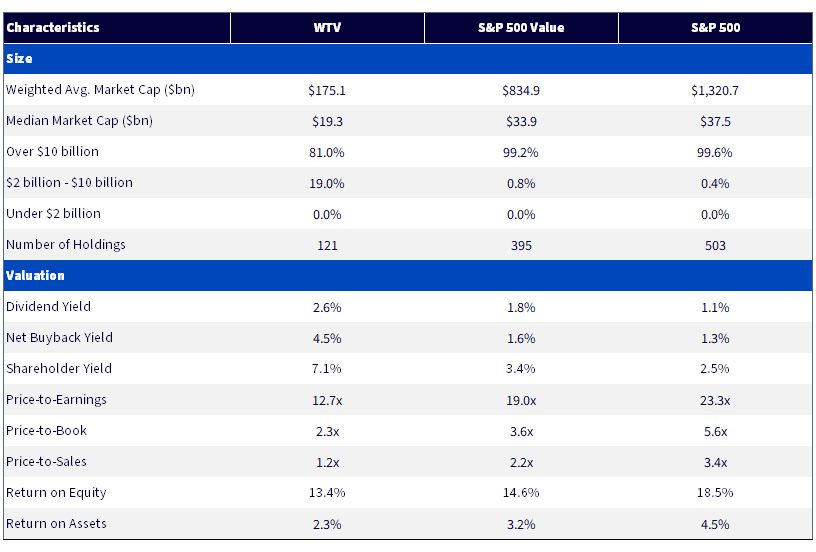

WTV looks markedly different from traditional value indexes:

- Low Overlap with the S&P 500: Only 16% overlap, compared with 61% for the S&P 500 Value.

- Limited "Mag 7" Exposure: Just 5.3% in the Mag 7, versus 35% in the S&P 500 and 19% in the S&P 500 Value.

- High-Conviction Portfolio: About 120 holdings, compared with 395 in the S&P 500 Value.

The result is a portfolio that doesn't simply recycle the same mega-cap growth names dominating core allocations. WTV provides exposure to both established large caps and high-quality mid-caps—a balanced and differentiated value exposure.

Post-Rebalance Characteristics

Sources: WisdomTree, S&P, FactSet, as of 12/3/25. You cannot invest directly in an index. As of 12/18/25, WTV's SEC 30-day Yield = 2.15%. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click here.

Important Risks Related to this Article

This must be preceded or accompanied by a prospectus.

For current holdings of WTV, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models, and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Matt Wagner, CFA

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.