WTRE

New Economy Real Estate Fund

Published December 23, 2025

Global Head of Research

As 2025 has unfolded, the conversation around digital infrastructure has taken on the scale and energy once reserved for the early internet. Data centers and compute capacity have become the new oilfields. They are the massive, capital-intensive assets powering artificial intelligence, cloud-based application economies and an emerging class of autonomous digital systems. OpenAI, Microsoft, Alphabet, Meta, Amazon, Oracle and others are announcing multi-gigawatt buildouts as if they were announcing the next great hydroelectric projects of the 20th century.1 Each new deployment represents not just racks of graphics processing unites (GPUs) but an investment in national competitiveness, industrial policy and the physical substrate of intelligence itself. Compute has become a geopolitical resource.

Yet, focusing exclusively on data centers risks mistaking the visible tip for a much larger and more intricate iceberg. The next generation of digital infrastructure isn't confined to compute; it's the full nervous system of the digital world. Fiber routes, subsea cables, edge interconnects, satellite constellations and power distribution networks are all being quietly re-engineered to support AI's insatiable hunger for bandwidth and resilience. The demand for ultra-low-latency data transmission, synchronized compute across continents and renewable power at the edge is forcing a rethinking of how digital systems physically exist in space. In short, the entire internet's plumbing is being rebuilt in real time.

And here lies the opportunity: the world is converging on an era where compute, connectivity and energy form a single strategic triad. The firms that recognize this convergence, whether they're hyperscalers, utilities or specialized real estate investment trusts (REITs), are not merely building infrastructure; they are defining the industrial logic of the AI century. The next digital superpowers may not be the companies that own the best models, but those that control the layers of infrastructure enabling intelligence to move, think and power itself globally. The story of data centers is just beginning, but the true narrative of digital infrastructure is much bigger, and much more exciting, than most investors yet realize.

The WisdomTree New Economy Real Estate Fund (WTRE) is designed to capture the transformation of real estate from a traditional, income-focused sector into a core enabler of modern technology. Its foundation is the WisdomTree New Economy Real Estate Index, a rules-based benchmark that selects companies at the intersection of property and digital infrastructure. Each candidate company is evaluated through four thematic pillars: thematic relevance, market positioning, scalability and potential, and innovation. Firms must derive at least 50% of their revenue, profit or assets from activities tied to digital and industrial economy infrastructure, such as data centers, telecom towers, life sciences labs and modern logistics, or from emerging next-generation digital assets like blockchain hosting companies and high-performance compute facilities.

The Index intentionally balances stability with innovation, allocating 90% of its weight to established "Digital and Industrial Economy Infrastructure" and 10% to "Next-Generation Digital Infrastructure." This ensures exposure not only to large-cap leaders like Equinix,2 American Tower3 and Prologis,4 which anchor the ecosystem through data center and connectivity assets, but also to frontier companies such as Core Scientific,5 Applied Digital6 and Cipher Mining,7 which represent the more cutting edge infrastructure of the AI and blockchain economy. Each constituent is weighted by free float adjusted market cap, and the Index is reconstituted semi-annually to maintain alignment with evolving technology and market dynamics. In practice, this approach means WTRE systematically identifies the real estate assets most critical to megatrends, AI compute, global connectivity, digital logistics and biotechnology, ensuring that companies like IREN8 or AST SpaceMobile9 appear in the portfolio not by coincidence, but by design.

The Engines behind 2025's Next-Gen Infrastructure Rally

The performance story of 2025 isn't being written by the usual suspects in mega cap tech. Instead, it's being driven by a cohort of next-generation infrastructure companies that most investors had barely heard of two years ago. Take Iris Energy (IREN): originally pigeonholed as a Bitcoin miner, it's rapidly evolving into one of the most efficient AI compute operators on the planet. IREN's multi-gigawatt expansion plans in North America are strategically co-located with renewable energy assets, turning stranded hydro and wind capacity into AI horsepower.10 It has become a poster child for the convergence of digital assets, clean energy and high-performance compute, a story that feels as much about industrial reinvention as it does about technology.

Applied Digital and Cipher Mining are two others that embody this reinvention. Both began life in blockchain infrastructure but have transformed their data centers into multi-purpose compute campuses, striking deals with AI firms hungry for power and space. Applied Digital's expansion in Texas, paired with a power purchasing strategy that rivals the sophistication of utilities, has positioned it as a stealth beneficiary of the AI boom. Cipher, meanwhile, has leaned on its low-cost energy model and modular design to deploy new capacity at a breathtaking pace. Its edge isn't just technical; it's logistical.11 These companies show that the infrastructure winners of this decade are often those who understood energy economics first, and compute economics second.

And then there's AST SpaceMobile, pushing the frontier literally off-planet. Its vision, bringing direct-to-device broadband connectivity from space, is no longer a moonshot. With successful satellite tests and commercial partnerships announced in 2025, AST is turning what once seemed speculative into a viable complement to terrestrial fiber networks.12

Together, these firms are defining a new investment category that sits between technology and infrastructure, between speculative and indispensable. The catalysts driving them—AI demand, renewable integration, low-latency communications—are compounding rather than fading. Yet with valuations running hot and capital costs still high, investors face the dual challenge of distinguishing between sustained transformation and temporary exuberance. Either way, it's clear: the "pipes and power" of the AI era are being built now, and the companies behind them are no longer operating in the shadows.

The Morningstar Global Real Estate category is designed to capture strategies investing across the global listed property universe, typically including developers, landlords and REITs with commercial, residential, retail and diversified holdings.13

WTRE stands out precisely because it breaks from a more traditional real estate exposure template. Since April 21, 2022, the Fund transitioned from tracking the WisdomTree Global ex-U.S. Real Estate Index to the CenterSquare New Economy Real Estate Index, redefining its scope from conventional property exposure to the infrastructure powering the digital economy. The subsequent shift, on April 10, 2025, where WTRE began to track the total return performance, before fees, of the WisdomTree New Economy Real Estate Index, tilted exposures even further in this direction. This overall shift toward technology and innovation coincided with the rapid acceleration of AI, cloud and blockchain adoption, real estate segments far removed from traditional office or retail properties.

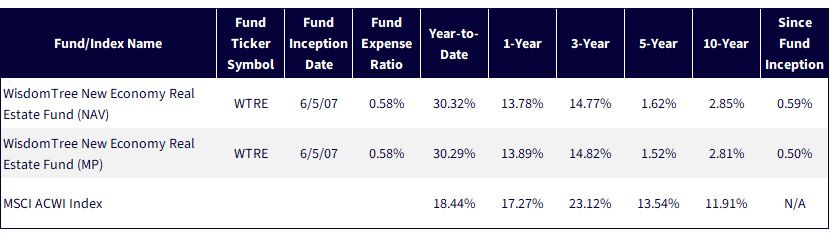

Over the longer horizons, the legacy exposure to non-U.S., traditional real estate assets shows in the numbers. For example, an annualized 2.85% return over 10 years ranks the Fund in the bottom decile of the peer group. Those figures reflected the structural headwinds faced by legacy real estate strategies during a period of rising rates, declining office demand and regional concentration outside the U.S., a reminder that the "old economy" REIT universe struggled to deliver real returns in a world shifting toward digital infrastructure.

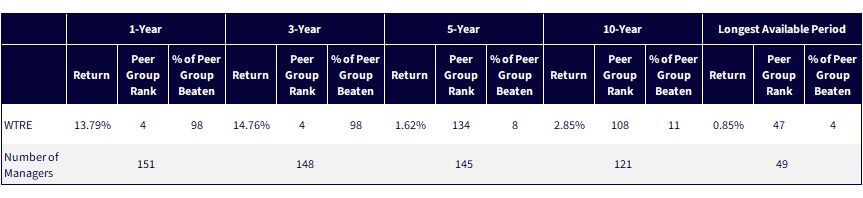

Since the tilt toward technology, however, WTRE's performance has been strikingly different. Its one-year return of 13.79% and three-year annualized return of 14.76% each rank the strategy fourth among more than 150 managers and ahead of 98% of peers for the respective periods. This underscores how the strategy's thematic focus has aligned with the strongest recent secular tailwinds in real estate. The exposure to data centers, digital logistics and next-gen infrastructure has transformed WTRE from a yield-driven Fund into a growth-oriented real asset strategy. It's a powerful illustration of how redefining "real estate" to include the physical backbone of the AI and cloud economy can turn a lagging category participant into one of its top performers. The pivot wasn't cosmetic, it was structural, positioning WTRE as an early leader in what may become the dominant form of real estate investing in the coming decade.

We see the full peer group rankings in figure 2, while we see the standardized performance as of September 30, 2025, in figure 1.

Sources: Morningstar, FactSet and WisdomTree, specifically data from the PATH Fund Comparison Tool, accessed 10/13/25, but showing returns for the period ended 9/30/25. WTRE's investment objective, strategy and policy changed effective 10/10/25. Prior to that date, Fund performance reflects the investment objective of the Fund when it tracked the performance, before fees and expenses, of the CenterSquare New Economy Real Estate Index. On 10/21/22, WTRE shifted from tracking the total return performance of the WisdomTree Global ex-U.S. Real Estate Index to the CenterSquare New Economy Real Estate Index. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Figure 2: Rankings within the Morningstar Global Real Estate Category

Source: Morningstar Direct. Peer group rankings are based on total return relative to funds in the Morningstar Global Real Estate category. The longest available period is 7/1/07–9/20/25, based on 7/1/07 being the closest next month start relative to WTRE's inception on 6/5/07. WTRE's investment objective, strategy and policy changed effective 10/10/25. Prior to that date, Fund performance reflects the investment objective of the Fund when it tracked the performance, before fees and expenses, of the CenterSquare New Economy Real Estate Index. On 4/21/24, WTRE shifted from tracking the total return performance of the WisdomTree Global ex-U.S. Real Estate Index to the CenterSquare New Economy Real Estate Index. Past performance is not indicative of future results.

Conclusion: Building the Physical Internet for the Age of Intelligence

The headlines about OpenAI's latest infrastructure ambitions for multiple gigawatts of new data center capacity over the next several years should stop readers in their tracks. A gigawatt isn't an abstract number; it's roughly the continuous power consumption of 750,000 U.S. homes. To bring even a single gigawatt of AI compute online, it takes not only racks of GPUs but also transmission lines, substations, cooling systems, fiber links and interconnection hubs, all working in unison. Every incremental watt of compute capacity ripples through a vast physical network of assets, from hyperscale campuses to modular edge deployments, from energy storage systems to network backbones orbiting the Earth. The scale of what's being built today rivals the great infrastructure expansions of the 20th century—it's the Hoover Dam era for digital civilization.

Despite this surge in construction, the system remains fully utilized. As of late 2025, there are no "dark GPUs" sitting idle. Every chip brought online finds work, training models, running inference or powering new generative applications.14 This real-world utilization data dispels the notion of an AI overbuild; demand continues to outrun supply in nearly every geography. The bottleneck isn't investor enthusiasm, it's available energy, land and fiber. That's why the conversation around AI infrastructure cannot stop at Nvidia or AMD. Those firms are designing the brains of the system, but the body, the connective tissue that moves data, power and signal, is where the compounding investment opportunity lies.

WTRE's framework is built for this reality. The rise of data center REITs, Bitcoin miners repurposing capacity for AI workloads, low earth orbit (LEO) satellite networks expanding connectivity and cellular tower operators densifying edge nodes all point to a new hierarchy of value creation. If the next decade truly involves bringing tens of gigawatts of compute online, every link in the chain, from energy procurement to data transmission, becomes essential. This isn't a single-sector story; it's an interlocking system of digital, physical and spatial infrastructure. The lesson for investors is clear: the age of intelligence will be powered not only by algorithms but by the real estate of computation, and the firms building it today will define the industrial landscape of tomorrow.

1 Sources: "Inside the Relentless Race for AI Capacity," Financial Times, August 2025; "OpenAI and NVIDIA Announce Strategic Partnership to Deploy 10 Gigawatts of AI Datacenters," OpenAI, 9/22/25; M. Zeff, "Mark Zuckerberg Says Meta Is Building a 5GW AI Data Center," TechCrunch, 7/14/25.

2 As of 10/13/25, Equinix was a 5.07% weight in WTRE.

3 As of 10/13/25, American Tower was a 4.82% weight in WTRE.

4 As of 10/13/25, Prologis was a 5.80% weight in WTRE.

5 As of 10/13/25, Core Scientific was a 1.39% weight in WTRE.

6 As of 10/13/25, Applied Digital was a 2.22% weight in WTRE.

7 As of 10/13/25, Cipher Mining was a 1.45% weight in WTRE.

8 As of 10/13/25, IREN was a 3.61% weight in WTRE.

9 As of 10/13/25, AST SpaceMobile was a 5.05% weight in WTRE.

10 Source: IREN, "IREN Business Update: 1.4 GW Data Center Project Highlighted," GlobeNewswire, 10/16/24.

11 Sources: Applied Digital Corporation, "Applied Digital Announces Long-Term Supply Agreement with TerraForm Power," GlobeNewswire, 12/19/23; Applied Digital Corporation, "Applied Digital Announces Energization of its 200-Megawatt Datacenter in Garden City, Texas," GlobeNewswire, 10/20/23.

12 Source: AST SpaceMobile, "AST SpaceMobile Announces Definitive Commercial Agreement with Verizon to Support Space-Based Cellular Broadband Across the Continental United States," Business Wire, 10/8/25.

13 Source: "Real Estate Funds," Morningstar.

14 Source: "North America Data Center Trends H1 2025: AI & Hyperscaler Demand Lead to Record-Low Vacancy," CBRE Research, 8/19/25.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in real estate involve additional special risks, such as credit risk, interest rate fluctuations and the effect of varied economic conditions. A Fund focusing on a single country, sector and/or emphasizing investments in smaller companies may experience greater price volatility. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

New Economy Real Estate Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.