QGRW

U.S. Quality Growth Fund

Published March 3, 2025

Global Head of Research

We recently wrote about how investing is a curious mix of logic and emotion and that few topics capture this tension as vividly as market valuations. They evoke awe during periods of booming optimism and despair when pessimism grips the crowd. From the tech boom of the late 1990s to the dominance of today's AI-driven narratives, markets rarely follow a script. As Howard Marks eloquently puts it, bubbles aren't just about numbers—they're about the stories we tell ourselves.1

High valuations, like those seen in the late 1990s or during the Nifty Fifty era, often presage significant corrections. But the market's tendency to overshoot—both up and down—creates opportunities for those with patience and discipline.

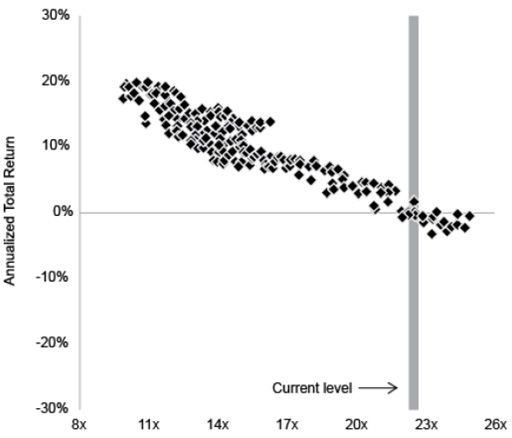

Howard Marks included a graph in a recent article from J.P. Morgan Asset Management, shown here as figure 1.2 There is a square for each month from 1988 through late 2014, meaning there are 324 monthly observations. Each square represents the forward P/E ratio on the S&P 500 Index and then the annualized return over the following 10 years. It's a clear depiction of all that we've said so far: the starting valuation has had a clear relationship to the subsequent return experienced.

Source: J.P. Morgan Asset Management, from Howard Marks, "On Bubble Watch," Oaktree Capital, 1/7/25. Past performance is not indicative of future returns. You cannot invest directly in an index.

The clear takeaway is that higher starting valuations have been associated with lower forward-looking returns.

The question isn't whether we're in a bubble—it's how to navigate the current environment. As Howard Marks says, "It's not what you buy; it's what you pay." Even great companies can become poor investments if bought at inflated prices.

So, what should investors do?

At WisdomTree, we think that if there might be a scarcity of forward-looking returns, income generation could be at a premium.

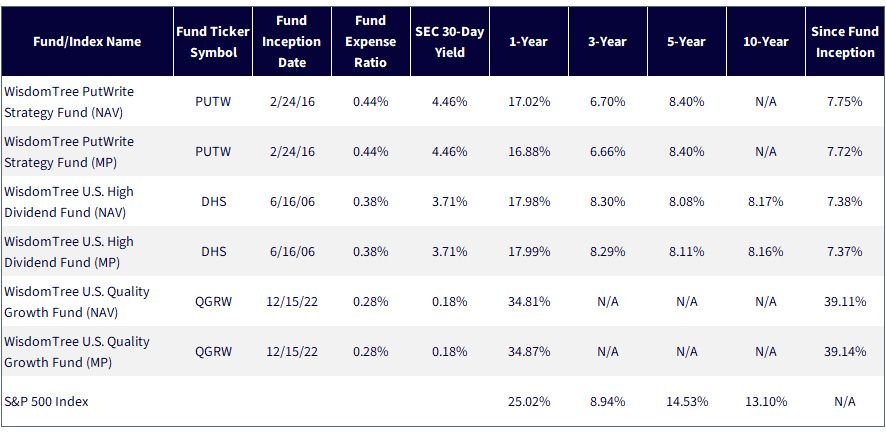

We can benchmark these against the S&P 500 Index, mentioned in figure 1.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/16/25, with returns as of 12/31/24. SEC 30-Day Yield as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Prior to 10/24/22, the WisdomTree PutWrite Strategy Fund was named the WisdomTree CBOE S&P 500 PutWrite Strategy Fund. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: PUTW, DHS and QGRW.

OpenAI released ChatGPT on November 30, 2022. While it was trickier to know at the time, in hindsight, this software release kicked off a massive run in large market capitalization growth equities in the U.S. As ChatGPT was capturing the world's collective attention, WisdomTree launched QGRW on December 15, 2022, which explains the starting point of figure 3. During this massive run in U.S. large-cap growth stocks:

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/16/25. NAV denotes total return performance at net asset value. Prior to 10/24/22, the WisdomTree PutWrite Strategy Fund was named the WisdomTree CBOE S&P 500 PutWrite Strategy Fund. The chart begins on 12/14/22, which essentially means that the opening price on QGRW's 12/15/22 inception date is captured. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker: PUTW, DHS, and QGRW.

Figure 1 discussed the relationship using the S&P 500 Index seeing that lower forward P/E ratios have been historically associated with stronger forward-looking 10-year returns.

In our view, this isn't telling us that the returns in growth are over—it's not that simple. It's telling us that stocks in the growth segment of U.S. equities are at greater risk of a particularly rosy set of circumstances being priced in. If those expectations are not met, a correction could be catalyzed.

One of the stories being told in figure 1 is that the price level of the S&P 500 Index has been appreciating faster than the earnings have been growing—which accounts for the higher P/E ratio. It could also indicate that the price level has been appreciating faster than dividends have been growing, accounting for a lowering of the dividend yield.

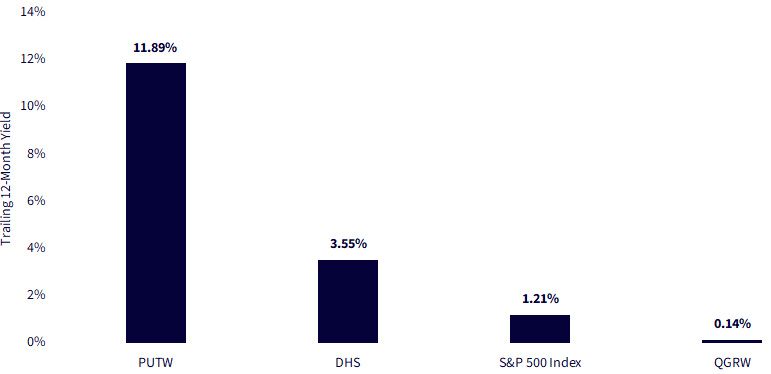

In figure 4, we look at the different distribution yields of PUTW, DHS and QGRW, with the S&P 500 Index dividend yield shown as a point of reference. It's clear that PUTW stands out, so it's important for us to look into this further.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/14/25. Past performance is not indicative of future results.

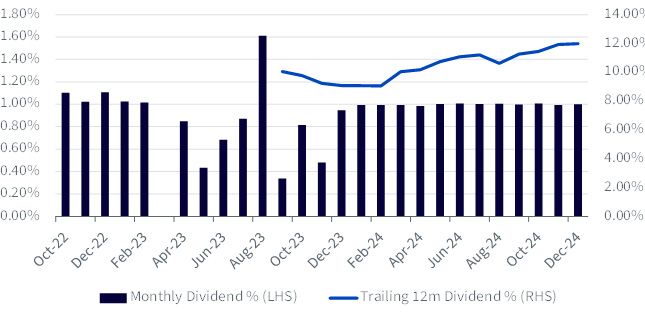

With PUTW's high distribution yield, it's important to understand this figure's inherent risk. The following quote comes from PUTW's prospectus: "The Fund is managed in a way that seeks, under normal circumstances, to provide monthly distributions at a relatively stable level."

It makes sense to test how relatively stable these distributions have been over the period for which the current strategy has been in place, which began on October 24, 2022.

Source: WisdomTree. Prior to 10/24/22, the WisdomTree PutWrite Strategy Fund was named the WisdomTree CBOE S&P 500 PutWrite Strategy Fund, which accounts for the time period shown in figure 5. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For PUTW's most recent month-end and standardized performance, click here.

Market valuations are a mirror of human psychology, reflecting both our hopes and fears. Today's market, driven by AI enthusiasm and the dominance of the Magnificent Seven, is a testament to the power of storytelling in investing. But as history has shown, the best narratives don't always yield the best returns.

Investing isn't about certainty—it's about probabilities. It's about balancing optimism about the future with realism about its price. Many people we speak to don't know if the market is more likely to trend upwards or downwards. If returns are simply more volatile and the compound annual growth rates are lower than they have been for the period since about 2020, we believe that income generating strategies, like PUTW and DHS, may be better positioned.

1 Source: Howard Marks, "On Bubble Watch," Oaktree Capital, 1/7/25.

2 Source: Marks, 2025.

3 The Magnificent 7 refers to Alphabet, Amazon.com, Apple, Microsoft, Meta Platforms, Nvidia and Tesla.

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

PUTW: The Fund will invest in derivatives, including S&P 500 Index put options (“SPX Puts”). Derivative investments can be volatile, and these investments may be less liquid than securities, and more sensitive to the effects of varied economic conditions. The value of the SPX Puts in which the Fund invests is partly based on the volatility used by market participants to price such options (i.e., implied volatility). The options values are partly based on the volatility used by dealers to price such options, so increases in the implied volatility of such options will cause the value of such options to increase, which will result in a corresponding increase in the liabilities of the Fund and a decrease in the Fund’s NAV. Options may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The potential return to the Fund is limited to the amount of option premiums it receives; however, the Fund can potentially lose up to the entire strike price of each option it sells. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs.

DHS: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

QGRW: Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets and the Index may not perform as intended.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.