Steeper Curves Ahead

Published August 20, 2025

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Key Takeaways

- Following July’s softer jobs report, markets now widely anticipate a September Fed rate cut, with additional easing priced in through 2026.

- Despite losing their inversion, the 3-month/10-year and 2-year/10-year Treasury yield curves remain historically flat, reflecting the Fed’s inaction amid shifting expectations.

- With short-term yields poised to fall faster than long-term rates, investors should prepare for a likely steepening of the yield curve when the Fed resumes cutting rates.

Following the softer-than-expected July jobs report, the money and bond markets have fully embraced the narrative that a Fed rate cut will be coming at the September FOMC meeting. On top of that, additional rate cuts are also being priced in for the rest of this year and for 2026. As far as the market is concerned, it is now not a question of “if” but “when” the Fed cuts rates again. Against this potential monetary policy backdrop, I’ve been asked questions about my thoughts on the Treasury (UST) yield curve and where it may be headed in the months ahead.

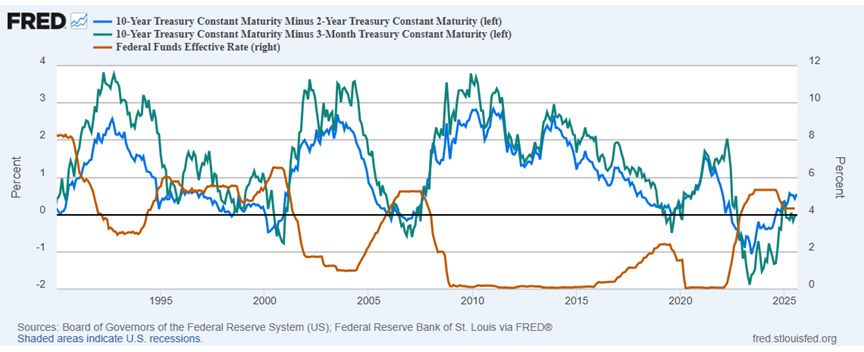

First up, it is important to point out that there are a variety of different yield curves one could follow. However, in bond-land, the two constructs that tend to be the most widely scrutinized are the 3-month/10-year and 2-year/10-year curves. Since the UST 3-Month t-bill yield essentially trades on “top” of the Fed Funds Rate, for the most part, one could use the 3mo/10yr curve as a proxy for the differential for overnight money versus the UST 10-Year yield.

Source: St. Louis Fed, as of 8/15/25

As of this writing, both of the aforementioned yield constructs are no longer inverted. However, they remain historically flat at +9 basis points (bps) and +56 bps, respectively. Interestingly, the 3mo/10yr curve has actually flattened year-to-date, and has at times gone back into negative territory, while the 2yr/10yr curve has steepened by about 25 bps. This is a function not only of changing market expectations for Fed rate cuts, but more importantly, is due to the fact that the policy makers haven’t actually lowered rates this year. Remember, the UST 3-month t-bill is directly correlated to the actual Fed Funds Rate, while the UST 2-Year yield is also impacted by market expectations for where Fed Funds may be going in the months ahead.

The graph above highlights an unmistakable trend…the Treasury yield curves outlined in this blog post have steepened, at one point or another, during each Fed rate cut cycle over the last 35 years. Upon further review, this should not come as a surprise. It really is just math, if you think about it. A declining Fed Funds Rate from Fed rate cuts pushes ultra-short- and short-term UST yields lower than what transpires at the back-end of the curve, namely UST 10-Year yields. In fact, you can even have what is known as a “bull steepener” where both short- and long-term yields fall, but the decline at the front-end of the curve is more than what transpires in longer-dated maturities.

Conclusion

In my opinion, the expected resumption of the current rate cut cycle should follow historical trends, resulting in steeper yield curves for both the 3mo/10yr and 2yr/10yr constructs. For this go-round, our base case is for the U.S. economy to avoid an outright recession, but it will only produce a slow growth setting. In addition, inflation is expected to remain above the Fed’s preferred 2% target. In this scenario, short-term rates will move lower right along with Fed Funds, but the UST 10-Year yield could be trapped in a 4%–4.75% trading range.

Categories

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.