Mag 7 Components Turning Value? The Russell Shuffle

Published July 11, 2025

Jeremy Schwartz, CFA

Global Chief Investment Officer

Matt Wagner, CFA

Director, Research

Key Takeaways

- Alphabet and Meta began paying dividends in 2024, making them eligible for WisdomTree's dividend-focused Indexes.

- In a landmark shift, Amazon, Meta Platforms and Alphabet now have portions of their market caps included in the Russell 1000 Value Index following the June 2025 rebalance—marking Amazon’s first-ever partial Value designation.

- This crossover reflects cooling Growth outlooks and more attractive valuations for these mega-cap tech names, with Alphabet’s forward P/E now lower than the S&P 500’s.

The annual Russell U.S. Index rebalance is always a bellwether for style-tilt rotations.

The top headline for this year: three of the "Mag 7" mega-caps crossed the Value/Growth divide.

At the end of June,1 Amazon (first time ever), Meta Platforms and Alphabet each had portions of their market capitalizations allocated to the Russell 1000 Value Index.

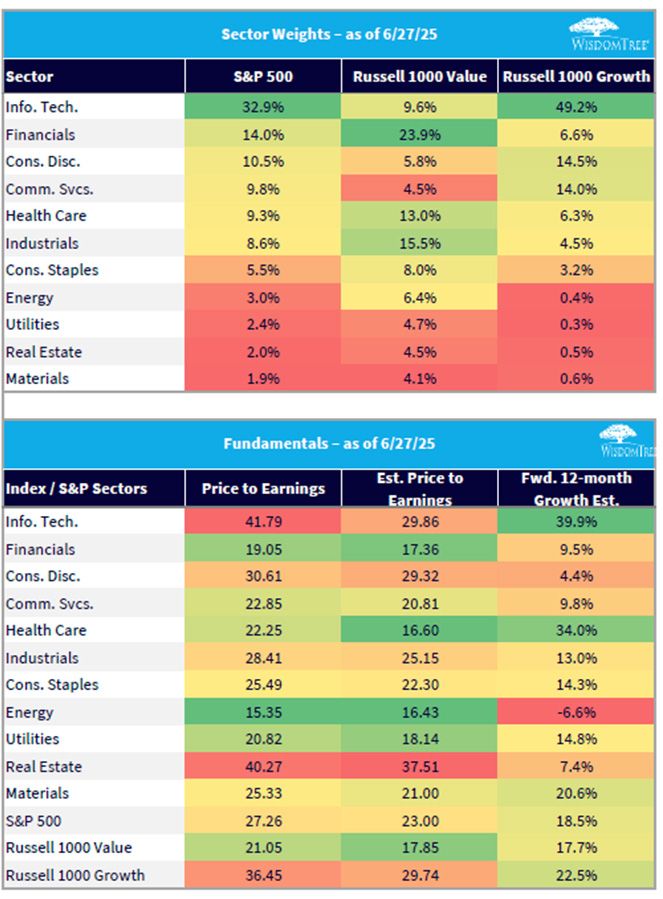

Current Sector Weights/Valuations

Figure 1 shows the pre-rebalance sector weights of the Russell 1000 Value and Growth Indexes.

Value—as is normal—was heavily tilted to Financials (24%), reflecting the sector's lower relative valuations and growth rates.

Growth, by contrast, exhibited its customary over-weights in Information Technology, Consumer Discretionary and Communication Services—sectors with among the highest valuations and growth rates.

Many of the Consumer Discretionary and Communications Services stocks are traditionally viewed as "Tech" stocks: Tesla, Amazon, Meta and Alphabet, in particular.

Figure 1: Sector Changes

Sources: WisdomTree, FactSet, S&P, Russell. You cannot directly invest in an index.

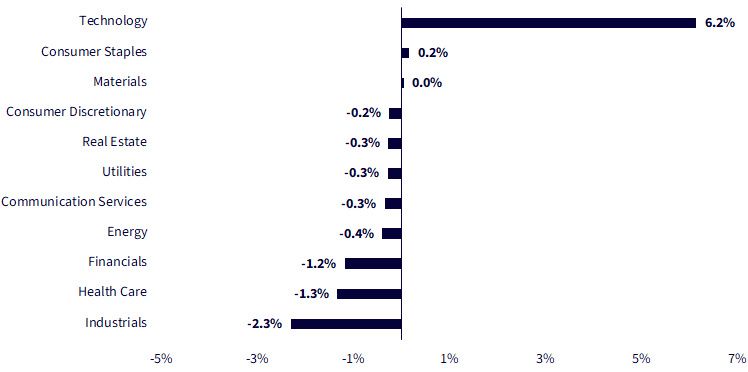

Zooming in on what shifted at the rebalance shows that the Russell 1000 Value Index picked up a meaningful 6% in Technology using a broader definition than GICS.

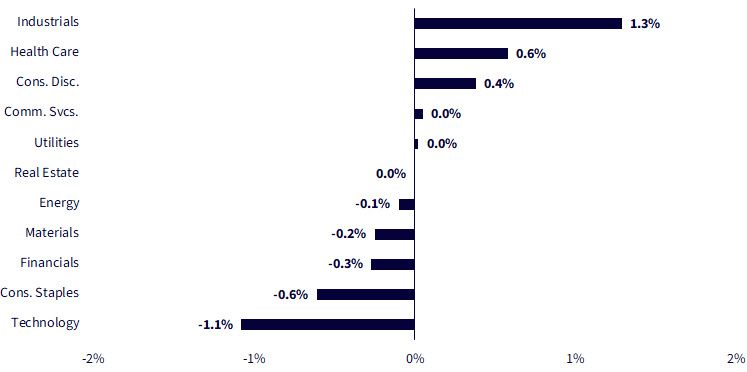

On the Growth side, changes were more muted: Industrials exposure ticked up via weight increases in GE Aerospace and the Index inclusion of GE Vernova, reflecting cyclical recovery themes in aerospace and clean energy.

Figure 2: Russell 1000 Value Sector Change

Sources: WisdomTree, FTSE Russell, Cantor Fitzgerald, as of 6/6/2025. Technology includes the Information Technology sector, Interactive Home Entertainment subindustry, Interactive Media & Services subindustry, Amazon, eBay, Etsy and Netflix. Changes based on preliminary rebalance files. Rebalance effective at the close on June 27, 2025.

Figure 3: Russell 1000 Growth Sector Changes

Sources: WisdomTree, FTSE Russell, Cantor Fitzgerald, as of 6/6/2025. Technology includes the Information Technology sector, Interactive Home Entertainment subindustry, Interactive Media & Services subindustry, Amazon, E-Bay, Etsy, and Netflix. Changes based on preliminary rebalance files. Rebalance effective at the close on June 27, 2025.

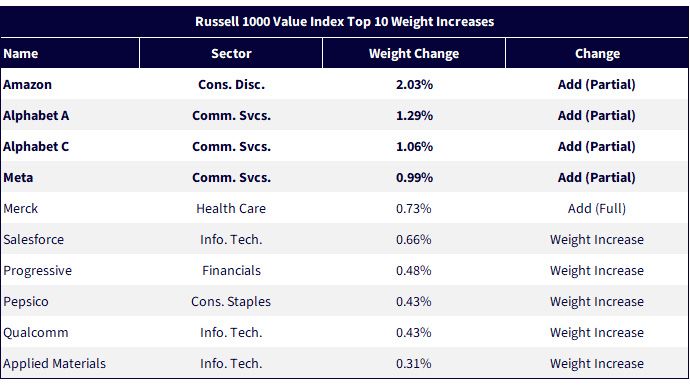

Top Name Changes

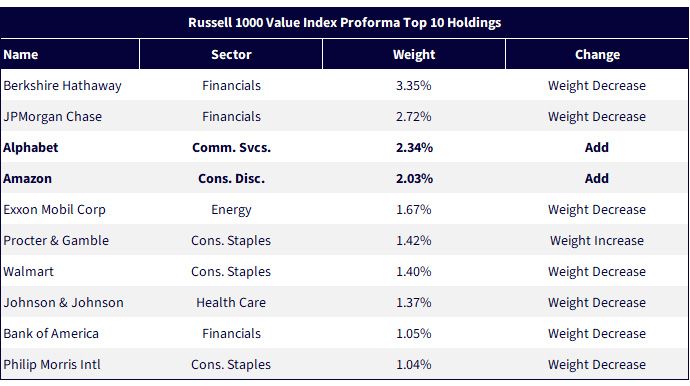

Alphabet—combining its share classes—landed as the #3 holding in the Value Index, followed by Amazon at #4.

Meta hovers just outside the top 10 at roughly 1% weight.

Importantly, each company still has more than half its market cap allocated to the Growth Index, meaning that Russell's model isn't exactly calling these "Value" companies. Instead, they are no longer "pure Growth" companies that have 100% of market cap in the Growth Index.

Figure 4: Russell 1000 Value Index Top 10 Weight Increases

Sources: WisdomTree, FTSE Russell, Cantor Fitzgerald, as of 6/6/2025. Changes based on preliminary rebalance files. Rebalance effective at the close on June 27, 2025.

Figure 5: Russell 1000 Value Index Proforma Top 10 Holdings

Sources: WisdomTree, FTSE Russell, Cantor Fitzgerald, as of 6/6/2025. Changes based on preliminary rebalance files. Rebalance effective at the close on June 27, 2025.

Alphabet Forward P/E Lower than S&P 500

Why did these Mag 7 names cross over from being pure Growth?

Russell's methodology employs a composite score that weights 50% on valuation (price/book) and 50% on growth measures (trailing sales growth blended with forward earnings estimates).

On valuation, Alphabet trades at a lower forward valuation (on forward P/E) than the S&P 500.

On growth, all three companies have significantly higher trailing five-year earnings growth than the S&P 500. Conversely, Alphabet and Meta each have lower earnings growth outlooks than the S&P 500.

Figure 6: Price-to-Earnings of Magnificent 7

Sources: WisdomTree, FactSet, S&P. as of 6/9/25. *Forward price-to-earnings growth based on median analyst estimates **Trailing 3-year where 5-year is not available. Growth is annualized. ***Estimated Long-Term Growth is annualized and based on median analyst earnings growth estimates over the next 3 years. You cannot invest directly in an index.

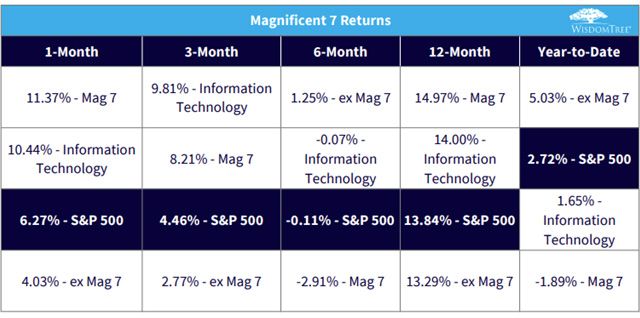

Sometimes, we see big reversals in sectors and/or single names based on recent performance. For example, significant underperformance from Growth in a particular year can lead more traditional Growth names into the Value Index.

A performance reversal doesn't seem to be a big part of the story this year.

Of the Mag 7 names added, only Alphabet underperformed the S&P 500 over the trailing 12-month period.

As a group, the Mag 7 has outperformed the S&P 500 by just more than 1% over the last 12 months.

Figure 7: Magnificent 7 Returns

Sources: WisdomTree, FactSet, S&P. Returns as of 6/9/25. Magnificent 7 includes Microsoft, Apple, NVIDIA, Alphabet, Amazon, Meta, and Tesla. Information Technology is the S&P 500 Information Technology Sector Index. You cannot invest directly in an index.

Bottom Line

Alphabet's underperformance and more attractive pricing made its Value inclusion not entirely surprising, with Meta a similar story, given its slower earnings growth outlook from analysts.

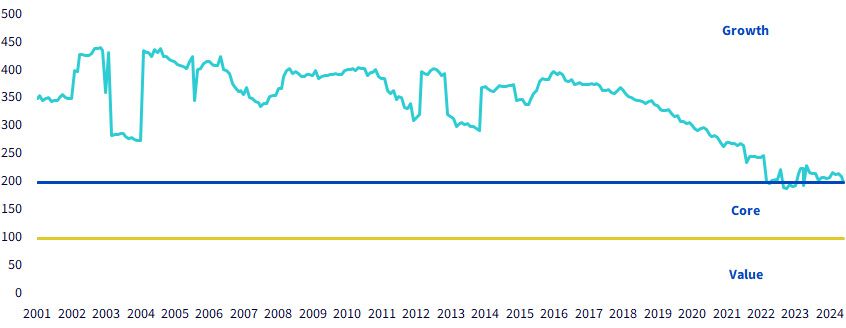

The surprise was Amazon. Its Growth bias has normalized from its extreme levels, but it still appears on our factor exposure score to be more of a core stock with growthy characteristics.

Figure 8: Amazon Historical Factor Exposure Score

Sources: WisdomTree, FactSet, 12/31/015/30/25. Factor exposure score based on a blend of Value fundamentals and Growth characteristics relative to U.S. equity universe. Score greater than 200 indicates Growth exposure, between 100 and 200 indicates core exposure and less than 100 indicates value exposure.

Each Index provider has its own nuanced definitions of what a "Value" stock is.

At WisdomTree, many of our Value and Value-tilted Indexes select only among dividend-paying companies and weight companies based on a modified Dividend Stream process, giving more weight to greater cash dividend-paying companies.

In our view, dividends are a measure of quality—management is signaling confidence in the recurring cash flow to support the dividend—and an objective anchor of valuation.

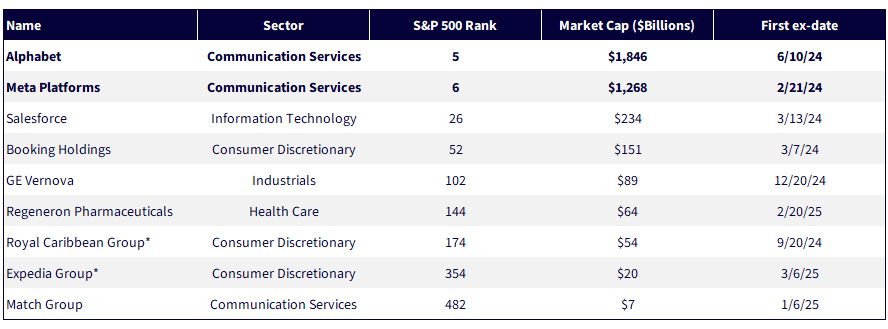

When Alphabet and Meta each began paying dividends in the first half of 2024, those companies became eligible for inclusion in WisdomTree's family of Dividend Indexes.

Figure 9: S&P 500 Dividend Initiators Since the Start of 2024

Sources: WisdomTree, S&P, FactSet, as of 3/31/25. *Dividends reinitiated after suspension during the COVID-19 pandemic in 2020.

In some ways, our dividend Indexes came to the same conclusion as Russell—but a year earlier—on including Alphabet and Meta via an alternative path, one focused on dividends instead of price-to-book and growth rates.

Will Amazon soon start returning more capital to shareholders via dividends? Maybe the Russell Value inclusion will motivate management to appeal to a broader community and start their cash return cycle.

The inclusion of these three Mag7 stocks might mean active Value managers have to start increasing their exposure for fear of mis-tracking the benchmark—an interesting summer season to be watching.

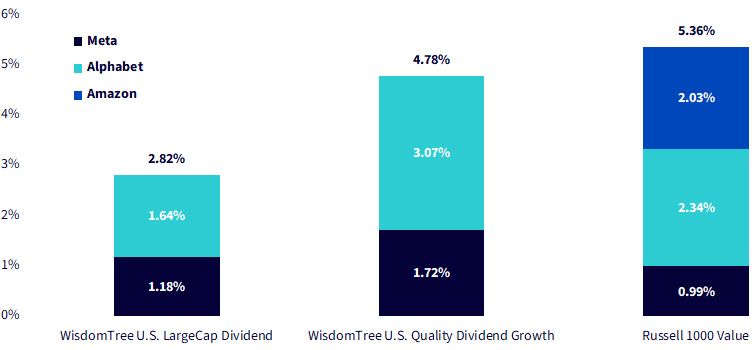

Figure 10: Index Weights

Sources: WisdomTree, FTSE Russell, Cantor Fitzgerald. Russell 1000 Value weights as of 6/6/25. Weights based on preliminary rebalance files. Rebalance effective at the close on 6/27/25. WisdomTree Index weights as of 6/10/25. You cannot invest directly in an index.

1The rebalance effective at the close of trading on June 27, 2025.

Categories

About the contributors

Jeremy Schwartz, CFA

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.

Matt Wagner, CFA

Director, Research

Matt Wagner joined WisdomTree in May 2017 as an Analyst on the Research team. He currently serves as a Director, where he supports the creation, maintenance, and reconstitution of WisdomTree’s indexes and actively managed ETFs. Matt began his career at Morgan Stanley, working as an analyst in Treasury Capital Markets from 2015 to 2017, focusing on unsecured funding planning, execution, and risk management. He graduated magna cum laude from Boston College in 2015 with a B.A. in International Studies, concentrating in Economics. In 2020, he earned a Certificate in Advanced Valuation from NYU Stern. He is also a Chartered Financial Analyst (CFA) charterholder.