DGRW

U.S. Quality Dividend Growth Fund

Published June 5, 2025

Global Head of Research

“We were using it and paying for it—we should have realized how powerful it was.”

—Charlie Munger, recalling early impressions of Google Search at a Berkshire Hathaway annual meeting1

When Charlie Munger and Warren Buffett discussed Google from the stage years ago, they weren’t talking about a hot new startup or a moonshot—they were marveling at a utility they used every day. The genius of Google’s business model was evident even then: provide an essential service with virtually zero marginal cost and monetize it at scale through targeted ads. The result? Alphabet has built one of the most successful commercial engines in history. In 2024, Google Search alone generated nearly $100 billion in net income.2

But even the greatest business models face their inflection points.

Alphabet now sits at the uncomfortable center of the Innovator’s Dilemma. Search, its crown jewel, is under existential scrutiny—not because it is failing, but because its success makes it difficult to pivot. As large language models and artificial intelligence (AI) agents proliferate, so do alternative methods of querying the world—Perplexity, ChatGPT, Claude and Grok are increasingly serving as the interface between curiosity and knowledge. Search’s supremacy is being unbundled, rethought and challenged from the edges.

Wall Street gets it. AI Overviews and AI Mode are promising starts, but analysts are quick to point out that the architecture of disruption has already been built. The question isn’t whether generative AI can technically replace some share of Google Search—it can. The question is whether Alphabet can execute a pivot without destroying a business unit that remains its primary profit center.

Alphabet’s answer has come in layers. First, it launched AI Overviews—a generative AI summary of answers sourced from across the web. Then, in May 2025, AI Mode was rolled out to all U.S. users, offering an integrated conversational interface on google.com modeled more like ChatGPT than a traditional list of links.3

But here’s the strategic tension: AI Mode is intentionally hard to find. Accessing it requires clicking a separate tab. There’s an understandable reason—it’s not yet clear how AI Mode will monetize relative to the traditional blue links and search ads model. Some of Alphabet’s best AI capabilities are now behind a $250/month “Ultra” subscription tier, indicating internal hesitations about cannibalization.4

And yet, the potential is immense. According to Google, users who engage with AI Overviews are already conducting 10% more search queries over time than those who do not, and those queries often involve more commercial intent.5 This is not erosion—it’s enhancement.

At its I/O 2025 event, Google laid out a roadmap that is bolder than some expected:6

These are not features for casual experimentation. They hint at a long-term strategy to migrate from a search engine to a user agent. From being the map to becoming the guide.

The evolving suite of AI features could be incrementally accretive to both engagement and monetization, particularly given Alphabet’s unmatched distribution scale and data advantage. When we say “unmatched scale,” we are considering:7

AI Overviews are already monetizing “on par” with traditional search in early tests, contradicting the prevailing investor fear of deterioration.8

The bear case remains valid: AI adoption could fragment behavior, compute costs could spike, and ads may migrate to more immersive or walled garden ecosystems. But the base case, and possibly the bull case, is that Google’s AI-enhanced search leads to more sessions, deeper engagement and richer queries—without sacrificing margin.

Alphabet’s Valuation Is Separated from the Other “Mag-7” Stocks

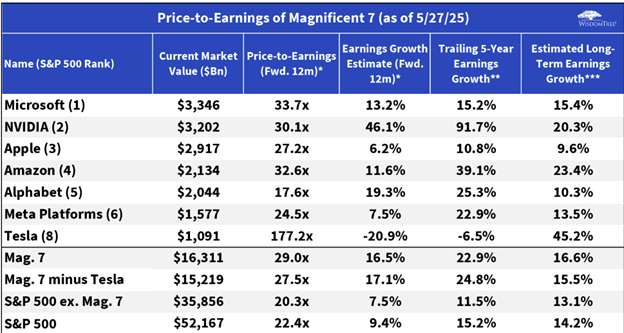

As is visible in figure 1, Alphabet’s forward P/E of 17.6x is not only the lowest among the Magnificent 7, but also sits below the S&P 500 Index average of 22.4x and well below its tech mega-cap peers. Despite this discounted valuation, Alphabet has delivered a trailing five-year earnings growth rate of 25.3%—a figure that outpaces the broader market and reflects strong fundamental performance. Yet the market appears to be pricing in a more modest long-term growth expectation of just 10.3%, significantly below peers like NVIDIA (20.3%) and Amazon (23.4%), even as Alphabet maintains dominant positions in search, mobile operating systems and emerging AI capabilities. This disconnect between valuation and historical earnings strength suggests investor expectations are unusually muted, likely due to uncertainty surrounding AI transition execution and monetization. With such low expectations embedded in its multiple, Alphabet may be one of the few mega-cap names positioned for a positive earnings surprise and multiple re-rating if it delivers on its AI strategy.

Sources: WisdomTree, FactSet, Standard & Poor’s. *Calendar year price-to-earnings and earnings growth based on median analyst estimates. **Trailing 3-Year where 5-Year is not available. Growth is annualized. ***Estimated Long-Term Earnings Growth is annualized and based on median analyst earnings growth estimates over the next 3 years. Trailing 5-Year Earnings Growth and Estimated Long-Term Earnings Growth as of 4/30/25. All other data as of 5/26/25. You cannot invest directly in an index.

It’s interesting to see in figure 1 that the aggregate estimated long-term growth for the Magnificent 7 is at 16.6%, which is only about 3.5% per year better than that of the S&P 500 Index benchmark constituents outside of these seven companies. It is a signal that the rest of a given growth-oriented strategy outside of these big names could be gaining in importance. Alphabet may be setting up for an upside surprise, but other big names in figure 1 have much higher valuations—it will be harder for them to do the same.

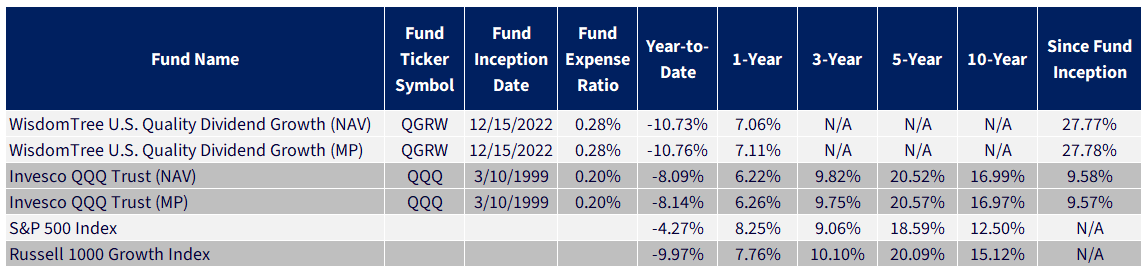

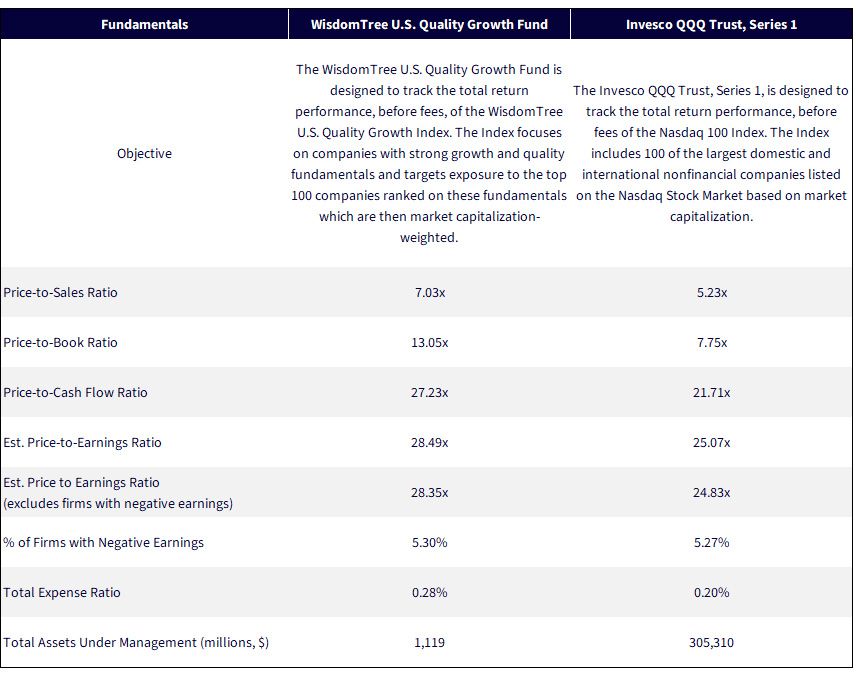

For many, the Nasdaq 100 Index, the total returns of which are tracked by Invesco QQQ Trust, Series 1 (QQQ), has been synonymous with exposure to big tech. But there’s an important nuance hiding in plain sight: the Nasdaq 100 Index doesn’t explicitly target growth or quality. It simply selects the 100 largest non-financial stocks trading on the Nasdaq Exchange.9 This means that while QQQ gives investors access to scale, it does not optimize for company fundamentals. As the market begins to differentiate more sharply within the mega-cap cohort, index design can become an active decision—even in passive wrappers.

Enter the WisdomTree U.S. Quality Growth Fund (QGRW), a fundamentally driven alternative designed to track the total return performance of the WisdomTree U.S. Quality Growth Index, which focuses on the more-profitable, higher-growth names in large-cap U.S. equities. There is a direct emphasis on return on equity, return on assets and earnings growth, as compared to Nasdaq 100 Index constituents, which are not included due to any direct requirements like this. For investors who believe the AI boom still has legs—but want a basket built on enduring fundamentals, not just market cap—QGRW may offer the right lens for this next leg of the tech trade.

Of course, the S&P 500 Index and Russell 1000 Growth Index could serve as reasonable benchmarks.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/25/25 with returns as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the respective ticker: QGRW, QQQ.

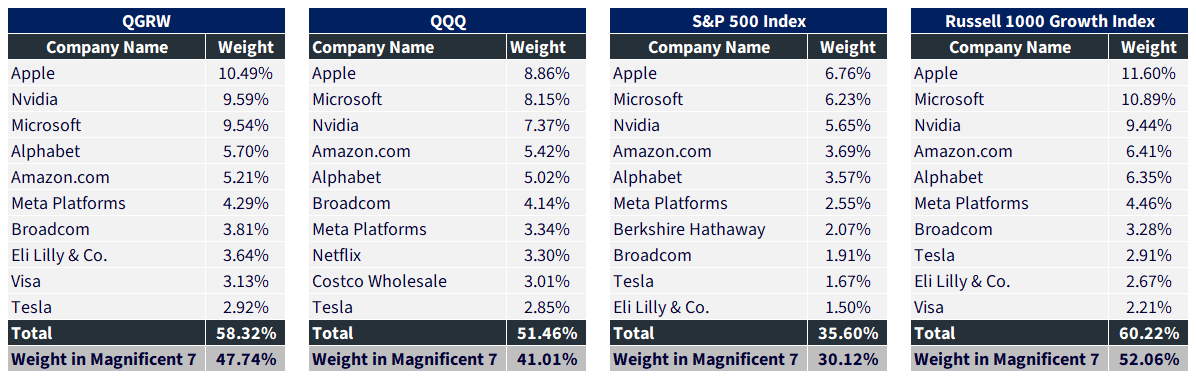

In figure 3, we see that QGRW, QQQ and both of the Index benchmarks all have significant exposure to the Magnificent 7. The Russell 1000 Growth Index was at the upper end, slightly above 52%, but QGRW was close behind at 47.74%. The S&P 500 Index was the lowest, at 30.12%.

Sources: WisdomTree, FactSet, with data accessed through WisdomTree’s Fund Compare Tool within its suite of PATH tools as of 5/25/25. Data is as of 4/30/25. Subject to change.

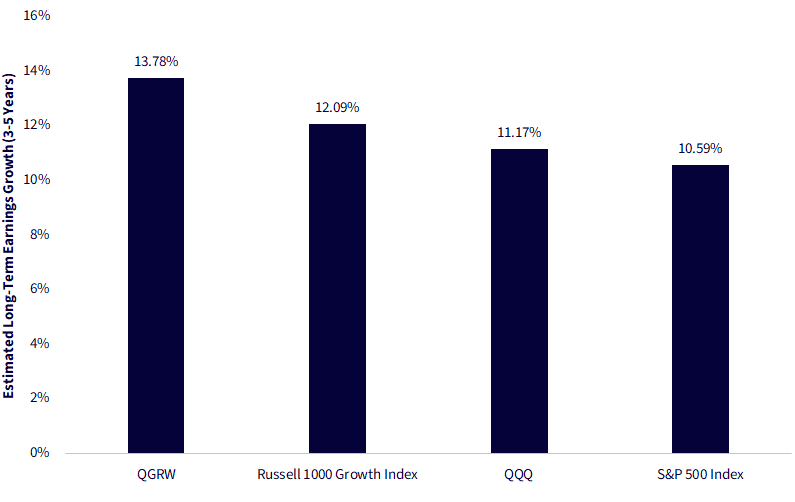

The bottom line for many investors is the concept that they can invest in companies that are growing earnings faster than the broad market. QGRW focuses on companies that are exhibiting stronger earnings growth estimates, as the Russell 1000 Growth Index is, accounting for the higher figures.

Sources: WisdomTree, FactSet, with data accessed through WisdomTree’s Fund Compare Tool within its suite of PATH tools as of May 25, 2025. Data is as of April 30, 2025. This is a different data field than in figure 1. Subject to change.

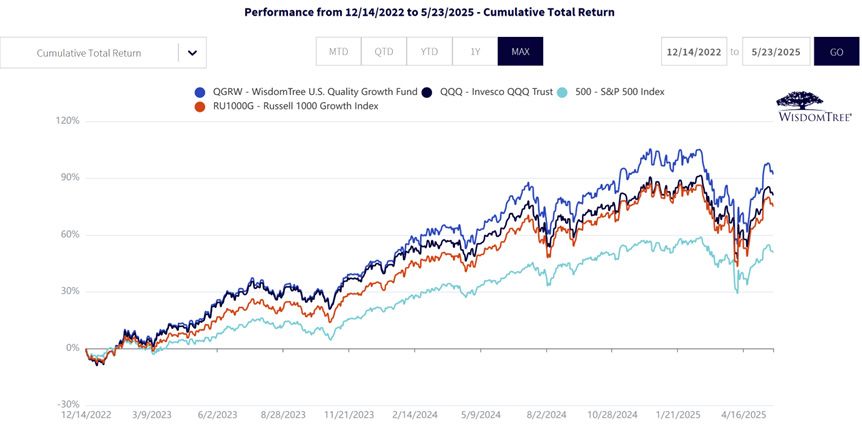

QGRW was launched on December 14, 2022, roughly two weeks after the launch of ChatGPT—the version that generated 100 million users in approximately two months.10 What we have seen since then has been an incredibly positive environment for large-cap growth equities in the U.S. QGRW has been able to, so far, outpace QQQ, as well as the Russell 1000 Growth Index benchmark. The S&P 500 Index, which is more “core” and not solely growth, lagged these other three strategies significantly over this period.

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 5/25/25 with returns as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances, click the respective ticker: QGRW, QQQ.

The way out of the innovator’s dilemma could be to act as though you have no incumbent business to protect. It’s a contrarian thought, especially when that incumbent business is worth $200 billion per year.11

But Alphabet may be threading that very needle.

The company doesn’t need to abandon search—it needs to reimagine what search can be while using its scale to steer user behavior rather than react to it. With the right integrations, AI may not disrupt Google’s cash machine. It may rebuild it for a new age.

Munger was right: they should’ve seen it. Now, the question is whether Alphabet does. As we continue to watch how some of the largest equities in the world navigate the evolving AI landscape, we think diversified strategies focused on growth and quality could mitigate the risk of being over-exposed to a strategic misstep—should it occur—from any single company.

Sources: WisdomTree, FactSet, with fundamentals as of 4/30/25 and assets under management sourced from WisdomTree and Invesco websites, current as of 5/8/25. Subject to change.

1Source: T. Franck, “Warren Buffett says he was ‘too dumb’ to realize Google’s potential early on,” CNBC, 5/6/19. https://www.cnbc.com/2019/05/06/buffett-says-he-was-too-dumb-to-realize-googles-potential-early-on.html

2Source: T. Kim, “Google struck gold with search. Now it’s time to move on,” Barron’s, 5/23/25.

3Source: B. Nowak, M. Bombassei, N.R. Chintala & J. Herrera, “How search will become more agentic...in 2025,” Morgan Stanley Research, 5/21/25.

4Source: (Nowak et al., 2025).

5Source: (Nowak et al., 2025).

6Source: (Nowak et al., 2025).

7Sources for list: B. Nowak, M. Bombassei, N.R. Chintala & J. Herrera, “How search will become more agentic...in 2025,” Morgan Stanley Research, 5/21/25; “Q3 2024 earnings call transcript,” Alphabet Investor Relations, 10/24/24. https://abc.xyz/investor/.

8Source: E. Sheridan, A. Vegliante, A. Sachdeva & B. Miller, “Google I/O 2025: Alphabet accelerates pace of AI innovation, led by Gemini” [equity research report], Goldman Sachs & Co. LLC, 5/20/25.

9Source: “Nasdaq-100 Index methodology,” Nasdaq, Inc., 2024. https://indexes.nasdaqomx.com.

10Source: K. Hu, “ChatGPT sets record for fastest-growing user base - analyst note,” Reuters, 2/1/23.

11Source: T. Kim, “Google struck gold with search. Now it’s time to move on,” Barron’s, 5/23/25.

For current holdings of QGRW, please click here. Holdings are subject to risk and change.

QGRW: There are risks associated with investing, including the possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified; as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

QQQ: There are risks involved with investing in ETFs, including the possible loss of money. Shares are not actively managed and are subject to risks similar to those of stocks, including those regarding short selling and margin maintenance requirements. Ordinary brokerage commissions apply. The Fund’s return may not match the return of the underlying Index. The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risk associated with an investment in the Fund. Investments focused in a particular sector, such as Technology, are subject to greater risk, and are more greatly impacted by market volatility, than more diversified investments.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.