EPI

India Earnings Fund

Published September 24, 2025

Global Head of Research

If you're a U.S. investor paying attention to India in September 2025, chances are you've seen only one storyline: geopolitics. India buys discounted oil from Russia. Prime Minister Modi is seen shaking hands with Vladimir Putin and Xi Jinping. There's discomfort in Washington about whether India is truly a partner or just playing all sides.1

This is the dominant narrative, reinforced by soundbites, often with a skeptical undertone. For many investors, it breeds hesitation. If the world is fracturing into blocs, why take exposure in a country that appears "non-aligned"?

But focusing on this alone risks missing the far bigger story. Because while U.S. audiences hear about geopolitics, what they're not hearing about is something far more consequential for investors: India's Next-Gen GST Reform.2

Ahead of the Diwali festival in late October 2025, the Indian government will roll out sweeping reforms to its Goods and Services Tax (GST), the country's unified consumption tax, akin in scope to a national value-added tax (VAT).

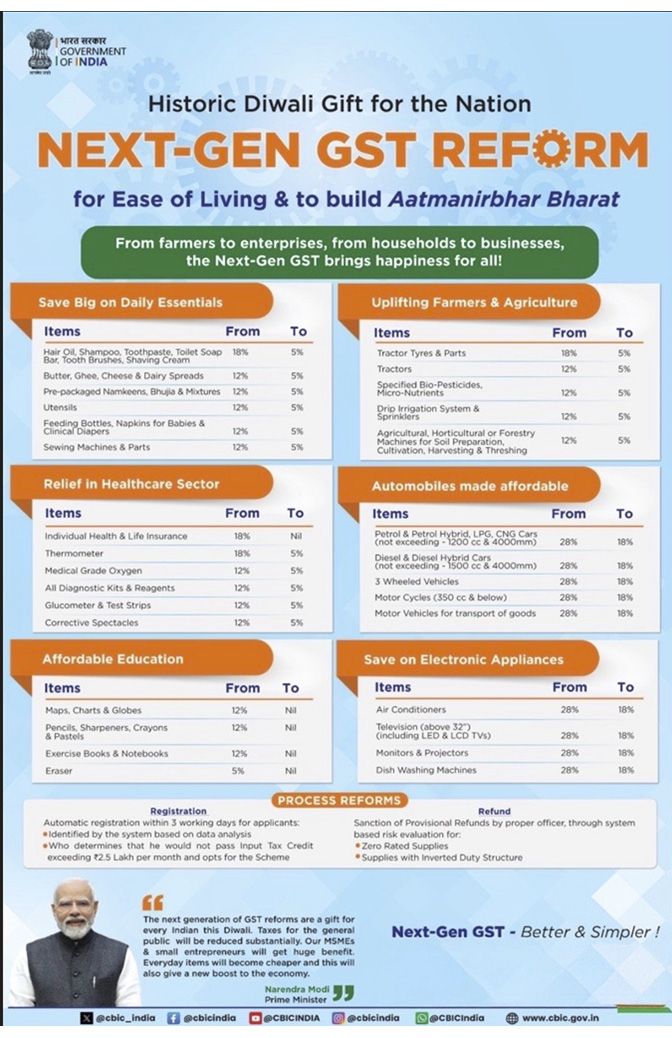

The changes weren't subtle. Figure 1 is a summary document prepared by India's government to detail the high-level changes.

Figure 1: India's Next-Gen GST Reform

Source: Government of India, Central Board of Indirect Taxes and Customs, "Next-Gen GST reform: Historic Diwali gift for the nation" [infographic], CBIC, 2025. Ghee is a type of clarified butter. Namkeens, Bhujia & Mixtures is a broad category of traditional Indian salty snacks. LPG is liquified petroleum gas. CNG is compressed natural gas. cc stands for cubic centimeter. mm stands for millimeters. LED stands for light-emitting diode. LCD stands for liquid crystal display. 2.5 Lakh rupees per month is 250,000 rupees, and is roughly similar in value to $3,000, as of September 5, 2025. MSMEs stands for micro, small and medium enterprises.

Looking just at the six headers in figure 1, the government's intent comes into sharper focus. Three of the categories—Daily Essentials, Farmers & Agriculture and Healthcare—are all being pushed toward a 5% GST rate. That signals a deliberate policy choice to lower the cost of necessities for households, farmers and patients. These are the foundations of day-to-day life: food, hygiene, farming inputs and medical care. By making them cheaper, the government is clearly prioritizing broad affordability, household consumption and support for small producers and rural communities.

At the same time, two other categories, Automobiles and Electronic Appliances, are being normalized to an 18% rate, down from the punitive 28% that had long discouraged demand. This creates breathing room for middle-class consumers and could accelerate spending on durable goods. The sixth category, Affordable Education, goes even further, dropping rates to nil. That underscores education as a public good rather than a taxable luxury, placing it on par with zero-rated essentials. Taken together, the six headers show a government that is easing pressure on both the household wallet and the engines of small enterprise, while also giving a symbolic and material boost to human capital investment through free-of-tax education.

India's Real Story Isn't Geopolitics; It's the Consumption Revival

The GST reform immediately expands household spending power. Roughly 99% of goods that are currently taxed at 12% are moving to 5%, and about 90% of goods currently taxed at 28% are moving to 18%.3 That means essentials, health care, educational items and even aspirational durables become significantly cheaper for 1.4 billion people. In a country where ~60% of GDP is consumption-led, this is not a marginal adjustment; it is a direct injection of demand into the system.4 First-order effects show up in household wallets, rural affordability for tractors and farm inputs and urban budgets freed up for consumer goods and services.

The second-order effects are already visible in earnings momentum and market positioning. Consumer staples, which had suffered two years of downgrades, just posted their strongest revenue surprises in five quarters. Autos rallied 4% in a single day after the GST announcement, with real estate, metals and staples following closely behind. Domestic mutual funds, still structurally under-weight in consumer staples by around -130 basis points relative to their benchmarks, are beginning to raise allocations, while foreign selling pressure in staples has finally stabilized. That creates both a fundamental and flow-driven opportunity: earnings revisions in consumer sectors are turning upward at the same time positioning is light, a combination that often leads to sustained outperformance.5

The third-order implications are macroeconomic and structural. Inflation is expected to moderate to around 3% in FY2026,6 and the current account deficit is contained at ~1% of gross domestic product (GDP), conditions that allow India to sustain this consumption push without destabilizing its balance sheet. Crucially, rural demand is strengthening on the back of a favorable monsoon season, which delivers the bulk of India's annual rainfall between June and September. That rainfall replenishes water supplies and is vital for farming, since nearly half of India's agricultural land is still rain-fed. Early data shows monsoon precipitation tracking 7% above normal this year. That has translated into stronger kharif sowing, the summer planting season that covers staple crops like rice, pulses and coarse cereals, up 3.4% year-on-year. More rain and more planting mean better harvests, rising farm incomes and healthier demand from rural India, which represents more than a third of consumption. As cheaper goods lift volumes and rural incomes improve, private-sector capex begins to follow, already visible in housing sales and new manufacturing projects. The result is a reinforcing cycle: policy lowers costs, demand expands, earnings and employment strengthen, and investment accelerates. For equity markets, this is the story U.S. investors are missing: India's domestic engine is firing in sync across households, corporates and the policy backdrop.7

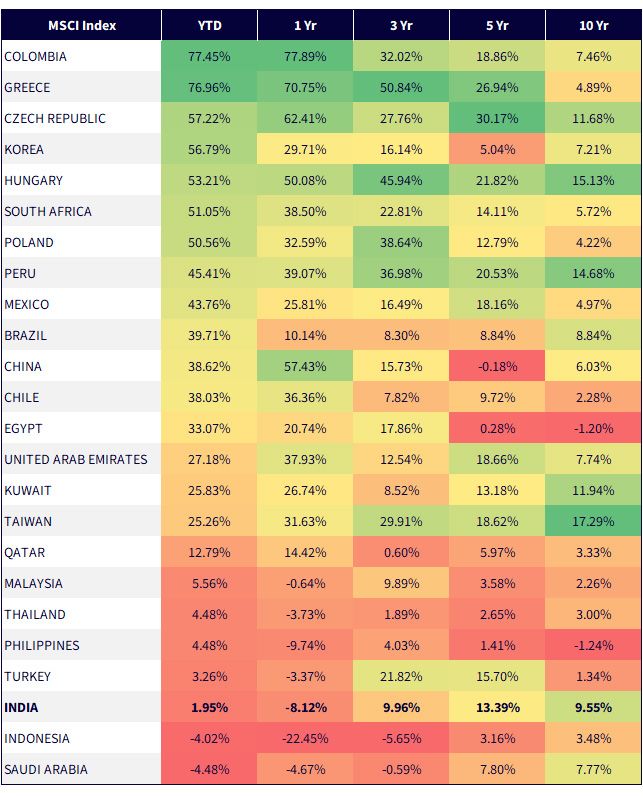

Conclusion: India's Place in a Diverging Emerging Market Landscape8

Looking across emerging markets year-to-date, leadership has been dominated by smaller, idiosyncratic stories: Colombia up roughly 77%, Greece not far behind, and the Czech Republic up roughly 57%. Much of this strength reflects local rebounds or commodity-driven surges that may not be durable. By contrast, larger emerging markets show a more mixed picture: China is up nearly 39% year-to-date, but its longer-term record is uneven, with a five-year annualized return in negative territory, actually the worst over that period of all 24 indexes shown in figure 2. Brazil is approaching 40% this year, but its 10-year track record is a more modest 8.8%. The key point: many of the best short-term performers as of early September 2025 currently lack the long-term consistency that institutional allocators may find more comforting.

India, in contrast, looks disappointing if judged purely on 2025 year-to-date performance, sitting near the bottom of the list at –1.95%, the worst of the still-positive performers over the period. But zoom out and the picture changes dramatically: over three years, India is up 9.96% annualized, over five years, 13.4%, and over ten years, 9.6%. These figures put India firmly in the upper tier of sustained performance among large emerging markets. Unlike commodity-dependent peers or reform-fragile economies, India's equity returns reflect a durable base of domestic consumption, steady policy reform and a corporate sector that has consistently delivered through cycles. What looks like near-term underperformance is more accurately a pause within a long-term compounding story.

The strategic implication is clear. U.S. investors focusing only on headlines, India's geopolitical positioning or a single year of lagging equity returns risk missing the structural opportunity. GST reform, fiscal discipline, favorable demographics and rising rural demand all point to a consumption engine that is strengthening just as other emerging markets may face greater fragility. In a world where many EM allocations are forced into volatile "boom-bust" cycles, India offers a rare combination: short-term noise, long-term consistency. That consistency is precisely what sets it up to remain a core emerging market allocation and potentially the anchor for investors seeking exposure to the world's fastest-growing large economy.

Figure 2: Why India's Equity Story Can't Be Judged by 2025

Source: MSCI, with performance data measured as of 9/19/25. Past performance is not indicative of future returns. You cannot invest directly in an index.

1 Source: "Xi Jinping's anti-American party," The Economist, 9/2/25.

2 Source: Unless otherwise noted, the source for different GST information is Government of India, Central Board of Indirect Taxes and Customs, "Next-Gen GST reform: Historic Diwali gift for the nation" [infographic], CBIC, 2025.

3 Source: "GST reforms: A potential boost to domestic consumer-sensitives" (India Strategy report), Goldman Sachs Global Investment Research, 8/21/25.

4 Source: "India economics – Catalysts in place for stronger growth" (investor presentation), Morgan Stanley Research, 9/4/25.

5 Source: Goldman Sachs, 2025.

6 In India, the fiscal year (FY) runs from April 1 to March 31 of the following year. FY2026 = April 1, 2025, March 31, 2026.

7 Source for economic data in this paragraph is Morgan Stanley, 2025.

8 Source for this section is MSCI, with performance data measured as of 9/4/25.

India Earnings Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.