India’s Next Chapter: Between Aspiration and Execution

Published May 5, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- Apple’s plan to shift the assembly of all U.S.-sold iPhones to India by 2026 highlights a seismic supply chain pivot that positions India as a rising global tech manufacturing hub. Days after this announcement, we have also been hearing from the Trump Administration about progress toward a trade deal between the U.S. and India.

- With average monthly wages just one-fifth of China’s, India offers a powerful labor cost advantage that could catalyze a long-delayed export boom, drawing comparisons to China’s post-WTO growth surge.

- The WisdomTree India Earnings Fund (EPI) has delivered 22.5% annualized returns over the past five years by focusing on profitable Indian companies, offering investors a strategic way to access India’s growth story without the risks of early-stage venture capital.

Many of us at WisdomTree are weekly listeners to the All-In podcast and big fans of the show. It was particularly exciting when the episode that published over the last weekend of April 2025 struck a distinctly optimistic tone about India's future in the global economy. As part of a 90-minute conversation that spanned technology, geopolitics and investment strategy, India emerged as a standout—a country increasingly seen not just as an alternative to China, but as a critical destination in its own right for multinational companies and global investors.

It was noticeable that even though David Sacks, who serves as the White House AI & Crypto Czar in the Trump Administration, was careful to note his official role is not negotiating trade deals, he kept repeating the alignment of the India with the U.S. against the common threat of China. He indicated this could be a very long-term reality in geopolitics.

On April 29, 2025, the market was also greeted with signals of significant progress toward an India-U.S. trade deal from the Trump Administration.

Key Topic: iPhones Destined for the U.S. To Be Made in India

All-In is frequently structured as delivering commentary and predictions based on the biggest events seen the week prior to the episode being recorded. One of the most eye-catching headlines in the India discussion came from a recent Financial Times report: Apple is aiming to shift the assembly of all U.S.-sold iPhones to India by the end of 2026.1 If successful, it would mark one of the most significant supply chain pivots of the modern era—a manufacturing migration driven not just by cost efficiencies, but by geopolitics, tariffs and the accelerating need for companies to diversify beyond China.

The scale of the ambition is staggering. Today, the U.S. accounts for roughly 28% of Apple's global iPhone shipments—more than 60 million units annually. To meet that demand, Apple would need to double its current iPhone production in India, an effort already underway through partnerships with Foxconn and Tata Electronics. In some ways, India is the natural choice: a massive labor force, improving infrastructure and a government eager to court technology giants.2

But if history teaches anything, it's that scaling world-class manufacturing is never as simple as it looks on a roadmap. Assembly is only the final step. The real complexity lies upstream, in the thousands of components that flow into every finished device. Today, India can assemble iPhones, but many of the key parts—chips, camera modules, advanced displays—still originate in China or other parts of Asia. Last year, Apple even had to import pre-assembled component sets to keep Indian production lines moving at pace.

In that light, the idea that every U.S.-bound iPhone could be truly "made in India" by 2026 looks less like a base case and more like an aspiration. Chamath was certainly reacting to this difficulty in the conversation. Final assembly in India? Very plausible. But full local sourcing of all critical components? That's a much harder lift, one that would likely extend well into the second half of this decade, if not beyond.

The bigger picture, though, is arguably even more important than the tactical details. Apple's move signals a sea change: India is no longer just "an emerging market." It's becoming an essential node in the global technology supply chain, not in 10 years, but now. Even if the transition isn't seamless—and it probably won't be—the direction of travel is clear. The question isn't whether Apple will make more iPhones in India. It's how quickly India can rise to the level of precision and scale that Apple demands, and whether the next wave of global supply chains will be more distributed, resilient and politically attuned than the last.

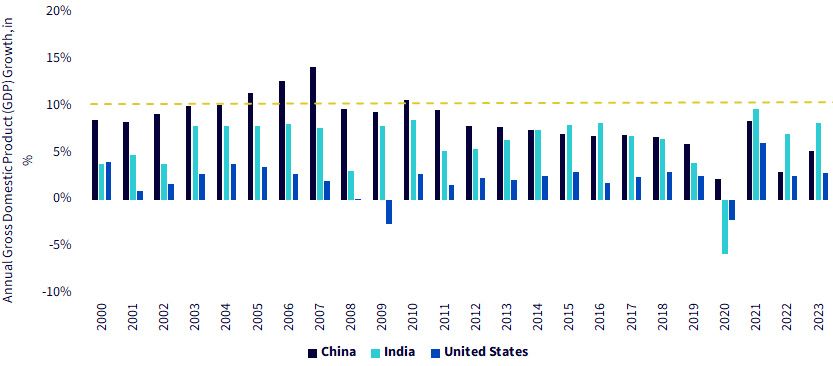

China's Economic Growth in the 2000s Was Spectacular—Might We See Something Similar for India?

When Chamath highlighted China's extraordinary growth trajectory after its entry into the World Trade Organization (WTO) in 2001,3 he wasn't exaggerating. Figure 1, which we created using World Bank data on World Development Indicators, vividly shows that between 2000 and 2010, China's GDP growth consistently hovered near or above the 10% annual mark (marked with the red dotted line). This is a stunning performance, especially when sustained over a full decade. In several years, growth rates were well into the double digits, a feat that transformed China from a low-cost manufacturing hub into the world's second-largest economy.

By contrast, India, while posting healthy numbers during the same period, largely operated in the 6% to 9% growth range. Impressive, but distinctly lower than China's breakneck pace. Meanwhile, the U.S. remained firmly in the 2% to 4% growth corridor throughout, illustrating the fundamental gap between developed and emerging market dynamics at the time.

This context is critical when thinking about India today. Chamath and the group pointed out that while India's growth prospects are bright—and indeed stronger than most large economies today—it is not yet following the same hyper-accelerated trajectory that China did post-WTO accession. Instead, India's path may be more measured and multi-polar, with growth fueled by internal consumption, technology adoption and selective manufacturing gains, rather than by becoming the world's single dominant export engine.

Figure 1: China's GDP Growth Rate of 10% (or above) in Certain Years Was Spectacular

Source: World Bank. World Development Indicators, The World Bank Group, 2025. Retrieved from https://databank.worldbank.org/source/world-development-indicators. Past performance is not indicative of future results.

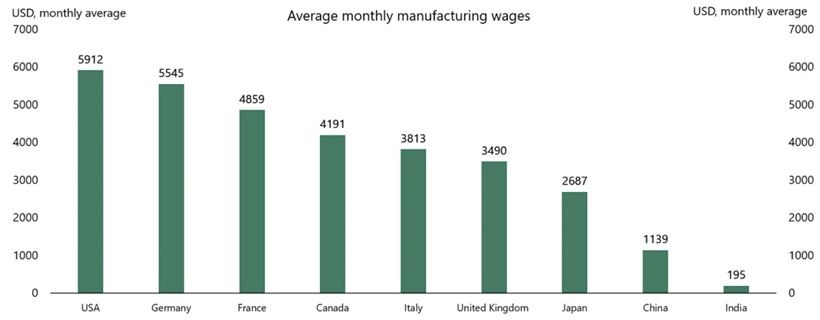

Labor Cost: India 1/5 of China, China 1/5 of the U.S.

Another major theme Chamath hit on during the India discussion was labor cost—and figure 2 makes the point visually impossible to miss. The numbers are staggering: the average manufacturing wage in India is just $195 per month. That's about one-fifth of China's average ($1,139) and roughly one-twenty-fifth of the U.S. average ($5,912).

This cost advantage isn't just theoretical. It's potentially catalytic. So far, India's economic rise has been driven mostly by domestic consumption—a growing middle class buying more goods and services inside the country. That's a different growth model than China's post-WTO ascent, which was fueled heavily by exports of manufactured goods.

But with labor costs this low, and with multinationals increasingly looking for China alternatives, it raises a provocative question: could India's next chapter look more like China's 2000s export boom?

The story India is writing now is not simply a rerun of China 20 years ago. It's something new—a hybrid of consumption-driven growth with the potential for a late-blooming export surge. That possibility alone adds a fascinating new dimension to the India investment case.

Figure 2: Average Monthly Manufacturing Wages

Source: T. Slok, Global Manufacturing Wages: India vs. China vs. United States [Chart], Apollo Academy, 9/16/24. Retrieved from https://www.apolloacademy.com/wp-content/uploads/2024/09/091624-Chart_v4-1.pdf. Subject to change.

India as an Investment Destination

One of the most honest—and valuable—parts of the All-In discussion came when the group acknowledged a crucial nuance: it's possible for the broad economic narratives about India to be true, and yet for it to still be an incredibly difficult place to invest.

Chamath, David Friedberg and Andrew Ross Sorkin all touched on it. They were largely speaking from the lens of venture capital investing—a world they know intimately well. And they're right: if you're used to operating in the U.S., jumping into India's venture landscape can feel like playing an entirely different sport. Regulatory hurdles, local business practices and market fragmentation all add layers of complexity. The risk profile is steep, and for many investors, particularly outside India, it may not be the right fit.

But that's not the only way to invest in India.

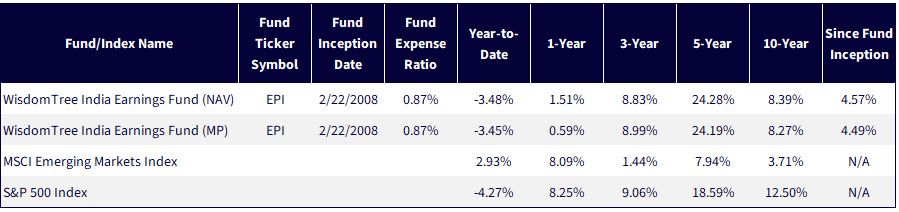

If you step back from venture and look at broad public equity exposure, the picture becomes much more navigable—especially with strategies designed to focus on profitability and earnings quality. WisdomTree's India Earnings Fund (EPI), which has been in the market since February 2008, is a case study in this. Unlike more speculative vehicles, EPI is structured to emphasize profitable companies, weighting exposures by their contribution to India's total corporate earnings base.

Figure 3: Standardized Performance

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/27/25, with returns as of 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. For definitions of terms/indices in the table above, please visit the glossary. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

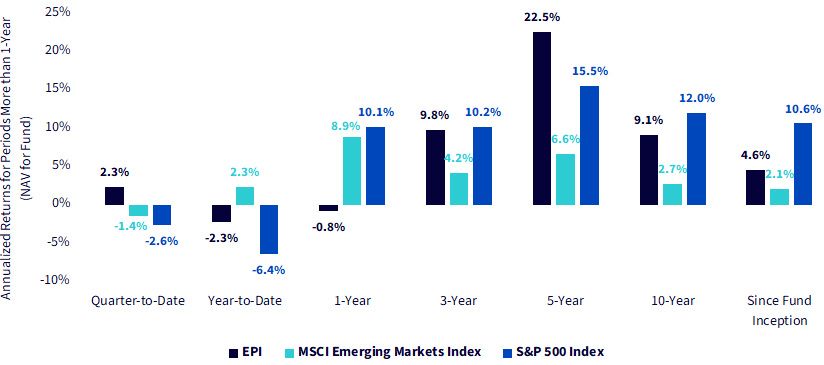

And when we look at the returns data, a compelling picture emerges:

- Returns: In figure 4, over the past five years, EPI has returned an annualized 22.5%, significantly outperforming both the MSCI Emerging Markets Index (6.6%) and even the S&P 500 (15.5%). EPI was consistently (except over one year) able to outpace the returns of the broader MSCI Emerging Markets Index. However, the S&P 500 Index looked particularly strong over the 10-year time frame as well as the time frame going back to EPI's inception in February 2008.

Figure 4: EPI's Returns Looked Relatively Strong over Many Periods

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/27/25, with returns as of 4/25/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

In figure 5, we zoomed in on the five-year period, which is clearly the strongest. The S&P 500 Index—and U.S. Exceptionalism4—has dominated the narrative over this period so many would not immediately know or predict that a strategy focused on India was able to outpace it. One can see how the annualized figures in figure 4 lead to the cumulative return experience—the effect of those differences on the compounding of equity returns is quite significant.

Figure 5: Zooming In on the Most Recent 5-Year, a Strong Period for EPI

Managing Over-Valuation Risk & Focusing on Growth Potential

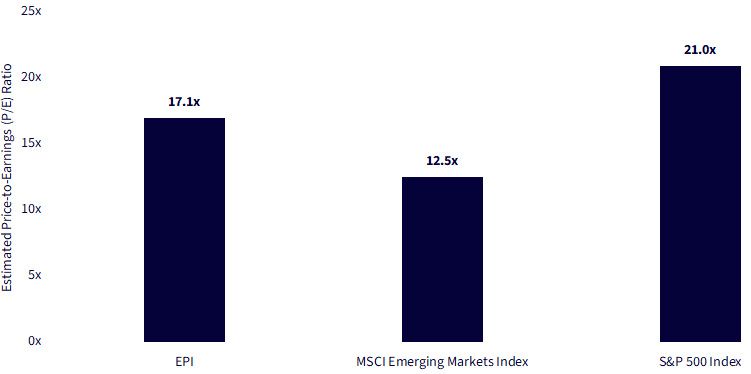

Once something is mentioned on a podcast as popular as All-In, the greatest risk to consider likely becomes valuation. This discussion was far from the first time India's demographic advantage, educated workforce and fast economic growth have been mentioned. For anyone researching India as a possible investment, these details are well covered. Once market participants see that growth in particular and feel that potential, it could translate to higher valuations. In figure 6:

- Valuations: As of today, EPI trades at an estimated 17.1 times earnings, noticeably below the 21.0 times multiple of the S&P 500 Index. EPI's investment strategy—defined in the methodology of the WisdomTree India Earnings Index—includes only profitable companies weighted by their earnings. Building a strategy in this way tends to mitigate the risk of continuing to add weight to companies becoming more and more expensive relative to their earnings.

Figure 6: Estimated Price-to-Earnings (P/E) Ratios

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/27/25, with fundamentals as of 3/31/25. Subject to change.

Growth, the Other Side of Value

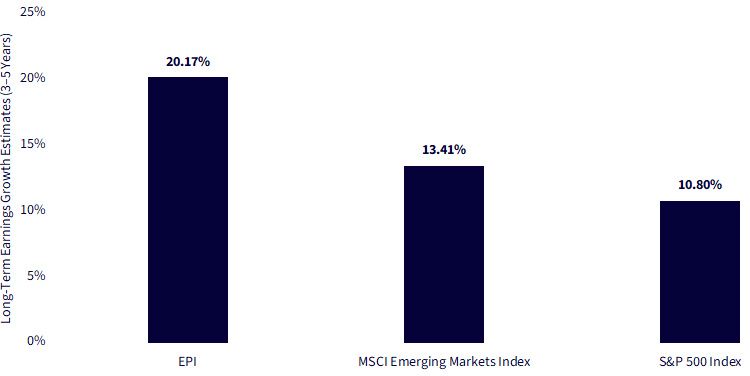

It's difficult to know what valuation means in isolation. The U.S. doesn't tend to be the fastest growth market in the world, but one of the reasons investors like it is the clarity of the data and the greater degree of transparency into company fundamentals. No one would argue that India's accounting standards have attained similar levels of clarity, even if the market is on an improving path. Still, for those looking to potential forward-looking earnings growth, in figure 7:

- Growth Expectations: Forward earnings growth for EPI is projected at 20.17% over the next 3 to 5 years, compared to 13.41% for emerging markets broadly and just 10.80% for the S&P 500 Index. These estimates are not without risk and accounting estimates for India's companies can be particularly risky, but the margin relative to the indexes shown is significant. The bottom line to any India allocation has to be a belief that the economic positives discussed in the All-In podcast episode translate through company fundamentals and contribute to earnings growth over the coming decades.

Figure 7: Earnings Growth Estimates for Companies within EPI Look Relatively Strong

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/27/25, with fundamentals as of 3/31/25. Subject to change.

Conclusion: India as a Long-Term Investment

The All-In conversation made one thing clear: the economic tailwinds behind India are not hypothetical—they are real, and they are accelerating. Apple's supply chain pivot, the country's unmatched labor cost advantages and its deepening geopolitical alignment with the U.S. all point toward a future where India plays a much larger role on the global stage.

Anyone following India's market is also looking to see if it will be the first country to announce a new trade deal, officially completed, with the U.S.

Yes, India can be a difficult market to navigate—especially for those approaching it through early-stage venture investing. But for general investors, the story is far from closed. Vehicles like EPI offer a pragmatic way to access India's growth while managing risk by focusing on profitable, established companies, diversifying across industries and avoiding the volatility of speculative early bets.

India may be tough, but it isn't uninvestable. It's a market where strategy matters—and matching the right approach to the right opportunity could make all the difference over the coming decade.

1 Source: Acton et al., "Apple Aims to Source All U.S. iPhones from India in Pivot Away from China," Financial Times, 4/25/25.

2 Source: Acton et al., 4/25/25.

3 Source: World Trade Organization, Ministerial Conference Fourth Session: Accession of the People's Republic of China, 2001.

4 Refers to the idea that the United States of America is a unique and even morally superior country for historical, ideological, or religious reasons. Proponents of American exceptionalism generally pair the belief with the claim that the United States is obligated to play a special role in global politics.

Important Risks Related to this Article

Unless otherwise noted, the source is: Calacanis et al., “Trump Rally or Bessent Put? Elon Back at Tesla, Google’s Gemini problem, China’s Thorium Discovery,” [audio podcast episode], All-In, 4/26/25.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. As this Fund has a high concentration in some sectors, the Fund can be adversely affected by changes in those sectors. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.