EPI

India Earnings Fund

Published February 2, 2026

Director, Quantitative Research

Head of Indexes, U.S.

At first glance, 2025 appeared disappointing for Indian equities. Relative returns lagged meaningfully, headlines lacked excitement and foreign participation was notably weak. In U.S. dollar terms, the MSCI India Index returned approximately 4.2%, a modest outcome compared to the broader global rally. By contrast, the MSCI Emerging Markets Index advanced roughly 34.3%, while the S&P 500 Index finished the year up around 17.9%. This divergence made 2025 one of the most challenging relative years for India in decades. Importantly, however, this underperformance reflected positioning and narrative dynamics rather than a deterioration in fundamentals. India simply lacked exposure to the dominant global equity themes, such as the artificial intelligence (AI) and semiconductor boom or the stimulus-driven rebound in China.

Foreign portfolio investor (FPI) outflows was a key drag throughout the year. FPIs were net sellers of approximately $18.4 billion, as global capital rotated toward markets offering cheaper valuations and more technology-heavy growth narratives. While domestic institutional investors stepped in effectively and prevented sharper drawdowns, the absence of incremental foreign capital limited upside and kept index-level returns subdued.

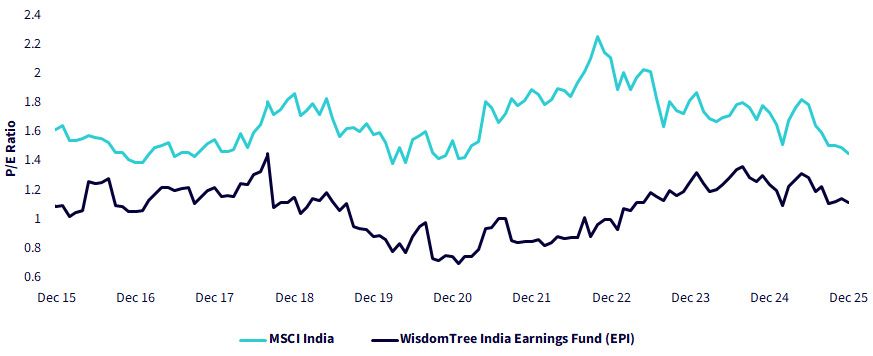

Valuations also underwent a period of normalization (see Figure 1). India entered 2025 trading at a significant premium to both its emerging market peers and historical averages. Although earnings growth remained healthy at mid-teens levels, it was insufficient to justify further multiple expansion, particularly against the backdrop of a strong U.S. dollar and restrictive global financial conditions. As a result, the market experienced a time correction rather than a sharp price adjustment, allowing fundamentals to catch up with expectations.

Figure 1 shows the MSCI India Index price-to-earnings (P/E) has come down significantly from its peak around end of 2022. It is also notable that WisdomTree India Earnings Index has consistently maintained lower P/E ratio compared to the MSCI India Index.

Sources: WisdomTree, FactSet, for the period 12/31/15–12/31/25. For definitions of terms in the chart above, please visit the glossary. You cannot invest in an Index. Past performance is not indicative of future results.

The key takeaway from 2025 is that it laid the groundwork for a more balanced forward outlook. Inflation has moderated and is hovering around the Reserve Bank of India's 4% target, with recent readings even lower. This has allowed the central bank to adopt a less restrictive stance, gradually easing domestic liquidity conditions.

At the same time, foreign investors remain materially underweight India. Given the scale of prior outflows, even a modest softening in the U.S. dollar or a stabilization in global interest rates could act as a catalyst for renewed foreign inflows. From a positioning perspective, the asymmetry has improved meaningfully compared to a year ago.

Despite near-term consolidation, India's long-term growth drivers remained resilient throughout 2025. Real GDP growth of approximately 7.5% continued to lead major economies, supported by several durable structural pillars.

Demographics and labor force dynamics remain a core advantage. India is now the world's largest provider of working-age talent, with a median age of roughly 28. Rising female labor force participation is expanding the productive base of the economy, reinforcing long-term consumption growth and improving household income durability.

Policy stability and investment visibility continue to differentiate India in a fragmented global landscape. While many economies grappled with political uncertainty, India offered continuity, enabling long-term capital expenditure planning across infrastructure, defense, energy and manufacturing. This stability has been instrumental in sustaining domestic investment cycles and attracting long-horizon capital.

Manufacturing, ‘China + 1' and supply chain realignment have become increasingly tangible. The "China + 1" strategy is no longer aspirational; it is being executed. Production-linked incentive schemes, combined with a deep STEM talent pool, are accelerating India's transition from a back-office economy toward high-end manufacturing and R&D. India has already built scale in smartphone manufacturing and pharmaceutical exports and is gaining traction in electronics, defense and increasingly semiconductor-related supply chains.

The evolving tariff and geopolitical landscape also merits attention. India faced heightened scrutiny and tariff-related challenges in prior years, which weighed on sentiment. However, the global backdrop has shifted. Trade frictions have broadened, with higher tariffs now being imposed across multiple regions, including traditional U.S. allies in Europe. Recent tensions spilling into politically sensitive areas such as Greenland underscore that tariff risk is no longer India-specific but part of a wider realignment of global trade. In this context, India's relative positioning has arguably improved, particularly given its scale, domestic demand base and strategic importance within diversified supply chains.

In hindsight, 2025 was less a year of disappointment and more a necessary reset. Valuation excesses were worked off, expectations were realigned and the market's foundation strengthened. With fundamentals intact, structural drivers firmly in place and foreign positioning significantly cleaner, India enters 2026 from a position of improved balance. If earnings growth remains on track and global flows stabilize, the coming year could mark a meaningful catch-up phase rewarding investors who looked beyond short-term underperformance and focused on the durability of India's long-term story.

The WisdomTree India Earnings Fund (EPI), which tracks the WisdomTree India Earnings Index, offers a long-established, broad market and valuation-conscious (see relative valuations comparison in Figure 1) approach to investing in the Indian markets. By selecting on profitable companies and weighting them by their net income, the fund controls valuation versus the market-cap-weighted indexes. This approach has led to historical outperformance versus the market-cap-weighted MSCI India Index, as shown below.

Sources: WisdomTree, FactSet, for the period 12/3/07 to 12/31/25 (earliest common history). For definitions of terms in the chart above, please visit the glossary. You cannot directly invest in an Index. Past performance is not indicative of future results.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund invests in the securities included in, or representative of, its Index regardless of its investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

India Earnings Fund

Director, Quantitative Research

Ayush Babel is the Director of Quantitative Research in WisdomTree's multi-asset quantitative research and index teams. In this role, he focuses on developing innovative quantitative strategies across various asset classes while supporting WisdomTree's diverse range of products. His expertise spans factor exploration, portfolio construction and optimization, quantitative investment research, and product development.

With over a decade of experience in the financial services industry, Ayush has held investment research roles at J.P. Morgan and Franklin Templeton. At these institutions, he was responsible for developing and managing equity and fixed income smart beta products, as well as cross-asset risk premia solutions for global institutional and retail clients. His experience covers a broad spectrum of asset classes and investment styles.

Ayush holds a bachelor's in Engineering Physics and a master’s degree in Nanoscience from the Indian Institute of Technology, Bombay.

Head of Indexes, U.S.

Alejandro Saltiel joined WisdomTree in May 2017 as part of the Quantitative Research team. Alejandro oversees the firm’s Equity indexes and actively managed ETFs. He is also involved in the design and analysis of new and existing strategies. Alejandro leads the quantitative analysis efforts across equities and alternatives and contributes to the firm’s website tools and model portfolio infrastructure. Prior to joining WisdomTree, Alejandro worked at HSBC Asset Management’s Mexico City office as Portfolio Manager for multi-asset mutual funds. Alejandro received his Master’s in Financial Engineering degree from Columbia University in 2017 and a Bachelor’s in Engineering degree from the Instituto Tecnológico Autónomo de México (ITAM) in 2010. He is a holder of the Chartered Financial Analyst designation.