CXSE

China ex-State-Owned Enterprises Fund

Published June 1, 2026

Global Head of Research

How Chinese companies became global leaders in AI infrastructure, electric vehicles, clean energy and biotechnology.

A Moment Worth Paying Attention To

There is a version of the China technology story that most investors think they already know: a government-directed economy producing low-cost goods, constrained by intellectual property concerns and increasingly caught in a geopolitical crossfire with the United States. That narrative has its basis in history, but it is increasingly an obstacle to clear thinking about where things stand today.

What has happened across China’s technology sector over the past several years is more substantial than incremental progress. In a handful of industries that the world’s most sophisticated economies agree will define the next several decades:

Chinese companies have emerged not as fast followers but as genuine leaders. Some are setting the pace globally.

For investors trying to build a portfolio that reflects the world as it is rather than as it was, that shift is worth understanding on its own terms.

Policy as a Signal, Not a Guarantee

One useful starting point is the Chinese government's own stated priorities. Beijing has been unusually explicit, over multiple planning cycles, about which technologies it considers strategically important. Examples include:1

These have all featured prominently in national policy frameworks, and they have been backed with directed capital, regulatory support and domestic procurement incentives at a scale that most governments would struggle to match.

The AI Infrastructure Layer Most Investors Overlook

Much of the conversation about artificial intelligence investment has focused on the large model developers and the consumer applications sitting on top of them. It is also important to look at the physical infrastructure that makes AI systems run: the networking, optical components, specialized chips and data center architecture that link everything together.

This is an area where Chinese companies occupy a surprisingly central position in the global supply chain. The optical transceivers that allow AI data centers to move data between accelerators at the speeds the technology requires are, in meaningful part, manufactured by Chinese firms.2

The push for semiconductor self-sufficiency is ongoing. It has been accelerated, notably, by U.S. export controls, which have had the unintended effect of concentrating Chinese engineering talent and capital on exactly the problems that most needed to be solved.

Electric Vehicles: The Transition China Is Winning

The electric vehicle story in China is now well-documented enough that the broad facts are widely accepted, even if their investment implications are still being absorbed. China is the world’s largest EV market by volume, and its leading manufacturers have achieved cost structures and production scale that European and American competitors are benchmarking against while struggling to match.3

What receives less attention is the breadth of the ecosystem that has developed around vehicle electrification. Some examples include:

Clean Energy: Control of the Supply Chain

The global energy transition requires solar panels, wind turbines, battery storage systems, and the grid infrastructure to connect them. The manufacturing base for most of those components sits, in large part, in China. This is the result of sustained investment over more than a decade, and its implications are becoming fully apparent as the energy transition accelerates globally.

Chinese firms dominate polysilicon refining, solar cell and module manufacturing, wind turbine production, and the battery supply chain from raw material processing through finished cells. The cost declines in solar and battery technology that have made the energy transition economically viable were, in substantial part, driven by Chinese manufacturing scale.4

Biotechnology: A New Kind of Innovation

Perhaps the least well-understood dimension of China's technology evolution is what has been happening in biopharmaceuticals. The sector has historically been associated with contract manufacturing and generic drug production.

That picture has changed materially. Chinese biotech companies have:

The depth of scientific talent that has accumulated in this sector, with much of it trained at leading institutions in the United States and Europe before returning to China, represents a durable foundation, not a temporary advantage.5

The Geopolitical Variable: Present but Not Determinative

None of the above is to say that China technology investing is uncomplicated. The geopolitical environment is real, consequential, and must be part of any honest framework. U.S.-China technology tensions have already produced significant disruptions.

The honest framing is probably this:

Investors who cannot accept that volatility may want to consider other geographic equity allocations.

But the same geopolitical pressures that create risk have also accelerated the very capability-building described above. The trade tensions and export controls of the past several years have, paradoxically, produced a Chinese technology sector that is more self-sufficient, more domestically resilient, and more focused on the specific capabilities that will matter most in the decades ahead.

The geopolitical backdrop is not a reason to dismiss the opportunity. It is a reason to understand it precisely.

The China Equity Opportunity Is Real, but the Question Is How to Access It

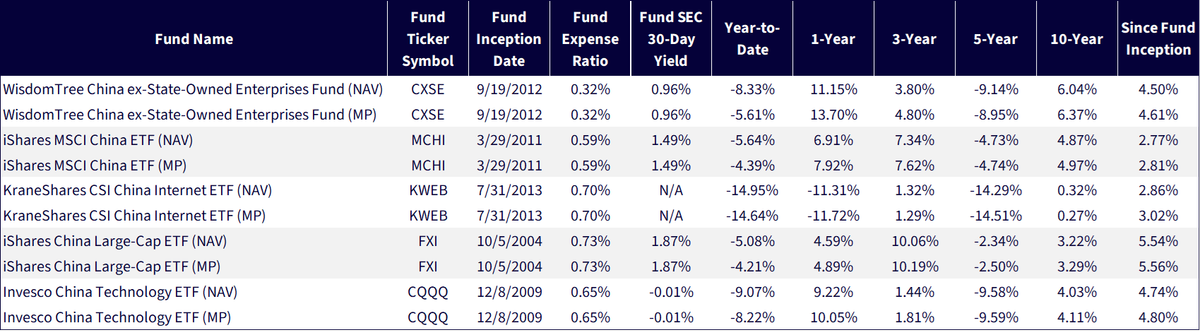

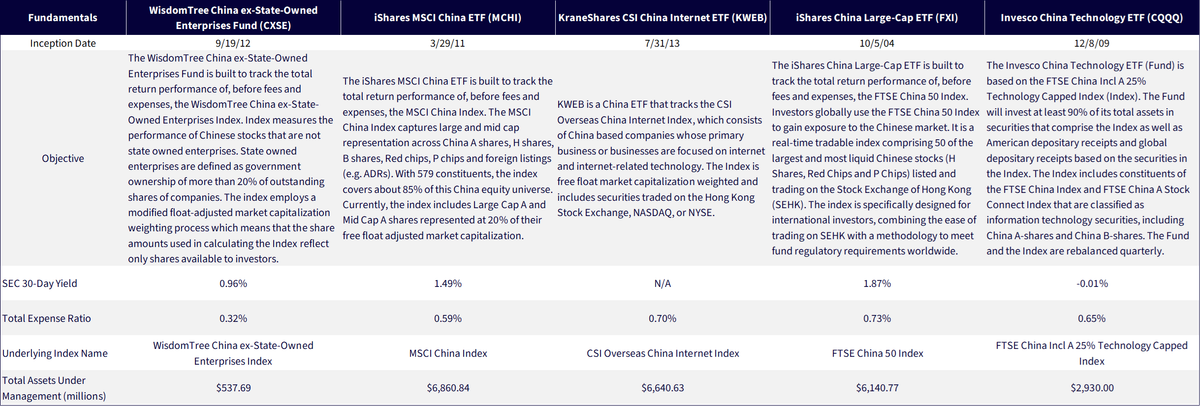

The narrative above establishes why the China technology story deserves attention. The more practical question is how investors can actually gain exposure to it. There is no shortage of U.S.-listed options, but they are not interchangeable. The funds available in this space reflect meaningfully different choices about which companies to include, which to exclude and what role the index designer believes active construction should play. Understanding those differences is itself an investment decision. As of the end of April 2026, the largest four China-specific ETFs within the Morningstar Greater China Region category were:6

For comparison, we bring in the WisdomTree China ex-State-Owned Enterprises Fund, which by the name is indicating a totally different focal point to China’s equity market, but under the hood we’ll be able to see some similarities with some of these other strategies.

Performance: Where the Rubber Meets the Road

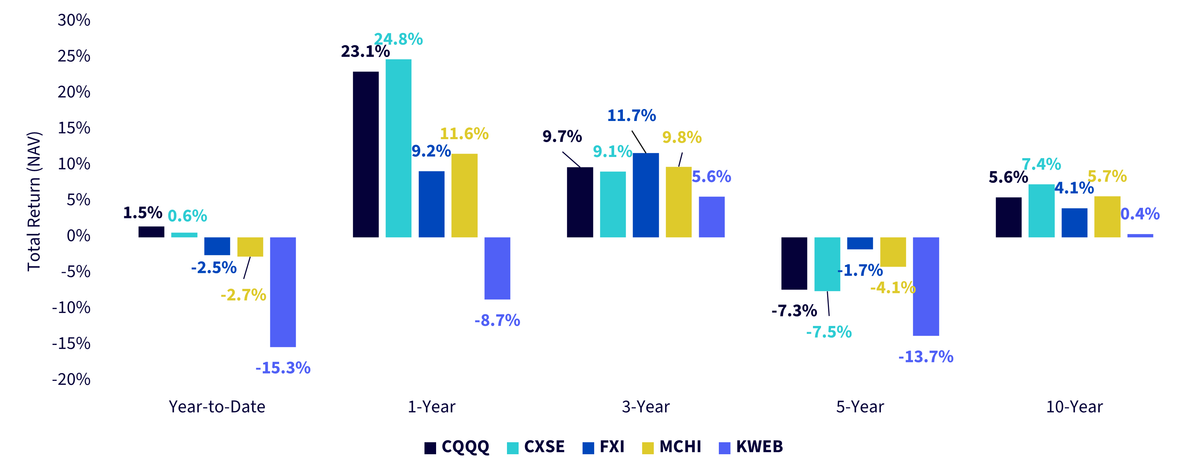

Figure 1a rewards careful reading, because the five funds are not telling the same story. They are telling a few different ones.

Start with the old economy. MCHI and FXI, the two broadest benchmarks, carry substantial weight in China's state-influenced financials, energy, and telecoms sectors.

Now look at the new economy: CQQQ and CXSE, two funds heavily oriented toward private-sector technology and innovation. They tell a meaningfully different story at every horizon than MCHI and FXI.

KWEB's trajectory deserves its own honest accounting. The five-year figure is a direct scar from the 2021–2022 regulatory assault on China's consumer internet giants, a sector-specific shock that does not define the broader China technology opportunity.7

The question worth considering is this: if the thesis in the first half of this article is right—that China’s most consequential companies are private-sector innovators—does a selected China ETF allocation reflect that?

Figure 1a: The Divergence in Performance across ETFs Focused on China’s Equities

Figure 1b: Standardized Performance

Sources: Morningstar, FactSet and WisdomTree. Data are from the PATH Fund Comparison Tool, accessed as of May 8, 2026, and show returns for the period ended May 6, 2026, for Figure 1a and March 31, 2025, for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: CXSE, MCHI, FXI, KWEB, CQQQ.

The Top 10 Holdings of Each ETF Say a Lot

FXI’s list says something immediately: three of its top five slots belong to Chinese state-owned banks, specifically China Construction Bank, Industrial & Commercial Bank and Bank of China. This is the old economy in concentrated form.

MCHI broadens the picture but still carries that state-owned enterprise (SOE) weight, with two major banks in the top ten alongside the familiar platform giants.

KWEB and CQQQ tilt decisively toward the new economy, focusing on consumer internet and technology respectively, though KWEB's concentration is striking, with its top ten representing over 63% of the fund.

CXSE tells the most differentiated story. The SOE banks are absent entirely because of the fund’s focus on ex-state-owned enterprises. In their place: Zhongji Innolight and Eoptolink, which are two of the most important AI infrastructure optical transceiver companies, alongside BYD, Xiaomi, and Midea. The holdings reflect the thesis at the front-end of this piece, not just the broader China equity market.

Figure 2: Strategic Differences are Apparent within the Top 10 Holdings

Sources: WisdomTree, Morningstar, FactSet, with data as of April 30, 2026 and from the WisdomTree Fund Comparison Tool within the broader PATH suite of tools. Holdings subject to change.

Conclusion

China’s technology evolution is not a future prospect; it is a present reality visible in the companies building AI infrastructure, electrifying global transport, supplying the world’s clean energy transition and originating innovative therapies that major Western pharmaceutical companies are actively licensing. The investment question is not whether that reality is worth exposure to, but how to access it with precision. The funds examined here offer meaningfully different answers to that question. For investors who believe the most consequential chapter of China’s economic story is being written by its private sector—by entrepreneurs rather than state enterprises—the construction of the portfolio should reflect that conviction.

Figure 3: Additional Information

Sources: Respective fund pages from WisdomTree, iShares, KraneShares, and Invesco. Assets under management as of May 7, 2026. The funds shown were selected due to their representation as large, widely used China equity ETFs with differing investment exposures and methodologies. Subject to change.

1 Source: People's Republic of China, National People's Congress. (2021). Outline of the People's Republic of China 14th Five-Year Plan (2021–2025) for national economic and social development and long-range objectives for 2035 (Center for Security and Emerging Technology, Trans.). Center for Security and Emerging Technology, Georgetown University.

2 Source: TrendForce. (2025, September 22). AI fuels high-speed interconnects, NVIDIA, Google, AWS boost optical transceiver module demand.

3 Sources: International Energy Agency. (2025). Global EV outlook 2025: Executive summary; Rhodium Group. (2026, February 19). Why are Chinese EVs so cheap?

4 Source: International Energy Agency. (2026). Energy Technology Perspectives 2026.

5 Sources: Tan, L., Song, K., & Lu, B. (2026). China's innovation in translational medicine: Rethinking early-stage clinical development. Nature Biotechnology, 44, 521–524; Drug Discovery World. (2025, October 23). Is China the next global biopharma powerhouse?; BioXconomy. (2025, April 10). China biopharma boom aided by returning talent.

6 Source: Morningstar, with data for the assets under management of the funds in the Greater China Region category measured as of April 30, 2026.

7 Source: The five-year figure is a direct scar from the 2021–2022 regulatory assault on China's consumer internet giants, a sector-specific shock that does not define the broader China technology opportunity.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

CXSE: There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in China, including A-shares, which include the risk of the Stock Connect program, thereby increasing the impact of events and developments associated with the region which can adversely affect performance. Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund’s exposure to certain sectors may increase its vulnerability to any single economic or regulatory development related to such sector. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For additional fund disclosures please click the respective ticker: MCHI, FXI, KWEB, CQQQ.

China ex-State-Owned Enterprises Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.