Adding, Not Replacing: Gold in the Age of Efficient Capital

Published May 6, 2026

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- Since the WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE) launched in March 2022, portfolios incorporating gold through an efficient overlay have outperformed traditional 60/40 allocations across multiple time horizons, signaling a timely opportunity to enhance diversification without sacrificing returns.

- As geopolitical risks, persistent deficits and evolving monetary policy challenge stock-bond diversification, GDE enables investors to pair equity growth with gold’s asymmetric upside in stressed market environments.

- By leveraging the Efficient Capital framework through GDE, investors can maintain core equity exposure while adding gold, moving beyond the traditional trade-off of selling growth assets to fund diversification.

For decades, portfolio construction has revolved around a simple constraint: you have 100 percent of a total allocation, and every new addition requires taking a portion from somewhere else. That constraint has shaped everything as we look at the dominance of 60/40 portfolios and the difficulty of incorporating alternatives without sacrificing expected return.

Introducing WisdomTree’s Efficient Capital Framework

WisdomTree’s Efficient Capital framework was not introduced as a theoretical concept, and it was launched into the market in 2018 with the debut of the WisdomTree U.S. Efficient Core Fund (NTSX).

NTSX represented the practical implementation of an idea that had largely lived in institutional portfolios and academic journals for decades. By combining a 90% allocation to U.S. equities with a 60% exposure to U.S. Treasury futures, the strategy delivered approximately 150% notional exposure, effectively recreating a traditional 60/40 portfolio, but doing so more efficiently, using less capital for the same overall notional exposure.

The innovation wasn’t leverage for its own sake. It was about solving a structural inefficiency in portfolio construction, thereby freeing up capital without giving up core exposures.

Since 2018, WisdomTree has expanded its range of options within the broader Efficient Capital Framework, and we think gold offers one of the most illustrative examples of helping investors solve a classic portfolio conundrum.

Filling the Gap: Why Gold Might Belong in an Efficient Portfolio

One of the most intuitive uses of newly created portfolio “space” is gold, an asset that has served as a store of value for centuries, yet remains persistently debated in modern portfolio construction.

Unlike equities or bonds, gold does not generate cash flows. It pays no dividends, earns no interest and compounds nothing. In 2011, Warren Buffett famously stated “Today the world’s gold stock is about 170,000 metric tons. If all of this gold were melded together, it would form a cube of about 68 feet per side… You can fondle the cube, but it will not respond.”1 That critique is valid, but it could also be incomplete. Gold’s role has never been about income. It is about diversification, purchasing power preservation and resilience in extreme environments.

Gold’s role in portfolios is often described in static terms, a few being:2

- Hedge

- Safe haven

- Diversifier

But in practice, its value is far more dynamic.

Gold tends to assert itself during periods when traditional assets face pressure, not only because of correlation properties, but because of how markets actually function under stress. During geopolitical shocks, for example, gold has historically outperformed equities over subsequent periods, even if its path is not always immediate or linear.3

What’s often overlooked is the mechanism. In the early stages of a shock, gold can decline alongside risk assets, not because its role has failed, but because it is one of the most liquid assets available to meet margin calls and forced selling. As those pressures subside, its fundamental drivers, such as geopolitical risk, currency instability and declining confidence in financial assets, can tend to reassert themselves.

At the same time, gold is deeply tied to macro conditions. Movements in real interest rates, the strength of the U.S. dollar and structural fiscal dynamics all influence its trajectory. In environments characterized by rising deficits, questions around monetary policy credibility or persistent geopolitical tension, gold’s role becomes more pronounced, not as a return generator in the traditional sense, but as a portfolio stabilizer with potential asymmetric upside in stress scenarios.4

In that context, gold’s lack of yield is not a flaw, and it is what allows it to behave differently when it matters most.

Still, the implementation challenge remains.

Allocating to gold traditionally requires selling something else in one’s portfolio allocation, usually equities, the very asset class that has historically driven long-term wealth creation. This creates a difficult trade-off: diversification versus compounding.

This is where the WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE) fits within the Efficient Capital framework. This strategy was launched by WisdomTree in March of 2022.

GDE is designed to resolve that tension by combining approximately 90% exposure to U.S. equities5 with 90% exposure to gold futures, delivering roughly 180% notional exposure. Instead of replacing equities with gold, it allows investors to hold both simultaneously.

In effect, if Efficient Core creates space, GDE fills it with a complementary asset, one that behaves differently across market regimes, without forcing investors to give up their primary engine of growth.

The result is a more balanced portfolio: one that can participate in upside, but is also better equipped for the environments where traditional allocations fall short.

From Trade-Off to Addition: A New Way to Add Gold to Portfolio Allocations

To make this more tangible, we can compare three portfolio allocations, but first we have to define our different ETF building blocks.

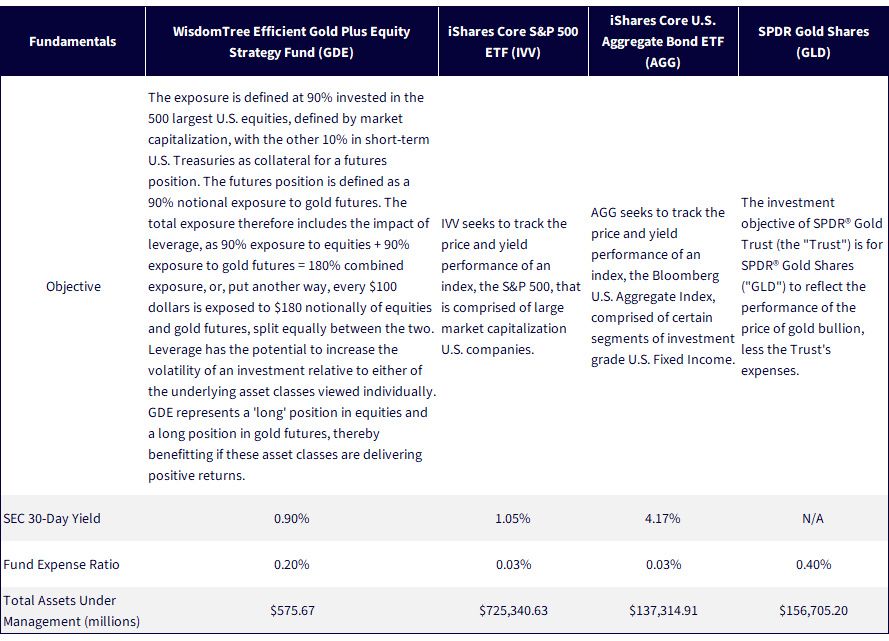

- IVV: The iShares Core S&P 500 ETF, which is designed to track, before fees and expenses, the total return performance of the S&P 500 Index, the most widely followed and referenced benchmark for U.S. equity market performance. This strategy is among the largest by assets under management tracking this benchmark.

- AGG: The iShares Core U.S. Aggregate Bond ETF, which is designed to track, before fees and expenses, the total return performance of the Bloomberg U.S. Aggregate Bond Index. This is among the most widely followed measures of the performance of U.S. investment grade fixed income.

- GLD: The investment objective of SPDR® Gold Trust is for SPDR® Gold Shares to reflect the performance of the price of gold bullion, less the Trust's expenses. GLD is the largest, measured by assets under management, strategy that allows investors to gain exposure to the returns of ‘physical gold’ minus expenses as of this writing. We look to it as the primary choice investors got used to prior to having the example of WisdomTree’s Efficient Capital allocation choice.

- GDE: As described previously, this strategy focuses on providing broad exposure to a basket of U.S. large market capitalization equities alongside gold futures in a single investment strategy.

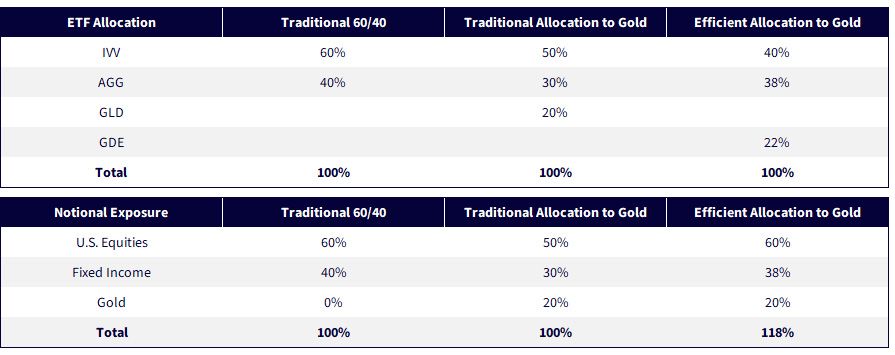

In Figure 1, the starting point is the ‘traditional 60/40’, 60% equities (IVV) and 40% fixed income (AGG). This serves as a familiar baseline, with 100% total notional exposure split between stocks and bonds.

From there, is the ‘traditional allocation to gold’ approach, which introduces exposure to gold by reallocating capital: 50% equities, 30% bonds and 20% gold, in this case through GLD. This maintains 100% total exposure but requires reducing core equity and bond allocations to make room for the diversifier, in this case, gold.

The ‘Efficient Allocation to Gold’ takes a different path.

Overall, the idea is to keep the roughly 60% U.S. equities and 40% U.S. fixed income parts of the allocation intact, but to then add exposure to gold over the top. Figure 1 shows how placing:

- 40% in IVV

- 38% in AGG

- 22% in GDE

Leads to notional exposures of 60% U.S. equities, 38% U.S. fixed income and 20% gold, in this case, gold futures.

This is the key distinction. The investor keeps close to the original allocation and adds a potential diversifier, in this case gold, over the top.

Figure 1: Gold Without the Trade-Off: Rethinking Portfolio Construction

Source: WisdomTree

Has It Worked? The Performance Case for Efficient Gold

Figure 2a illustrates a consistent performance hierarchy across time horizons, with portfolios incorporating gold outperforming a traditional 60/40 allocation. The “efficient allocation to gold” leads in almost every period, most notably over one year and three years. Even the traditional gold allocation improves outcomes relative to 60/40, reinforcing gold’s diversification benefits. We do recognize that gold has delivered strong performance over this period, which is really defined by GDE's inception date of March 17, 2022.

Figure 2a: Adding Gold Without Sacrificing Returns: The Performance Evidence

Figure 2b: Standardized Returns

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of April 11, 2026, but showing returns for the period ended April 9, 2026 for Figure 2a and March 31, 2026 for 2b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDE, IVV, AGG, GLD.

Conclusion: From Trade-Off to Opportunity

Gold has always occupied a unique place in portfolios, valued for its resilience, yet often underutilized because of the trade-offs required to own it. For decades, investors have faced a binary choice: allocate to gold and give up a certain percentage exposure to equities, or prioritize growth and forgo diversification.

Efficient Capital changes that equation.

By separating exposure from capital, strategies like GDE allow investors to move beyond that trade-off. Instead of asking whether to own gold or equities, the question becomes how to own both in a more intentional way. The result is a portfolio that retains its core growth engine while incorporating an asset designed to respond differently across macro environments.

In a world shaped by shifting geopolitical risks, evolving monetary policy and less reliable traditional diversification, that flexibility matters. The goal is no longer just participation—it is adaptability.

And that may ultimately be the most valuable asset of all.

Figure 3: Additional Information

Sources: Respect fund webpages for each respective ETF sponsor. Assets under management data is as of April 1, 2026. Subject to change.

- Source: Buffett, W. E. (2011). Berkshire Hathaway Inc. 2011 annual letter to shareholders. Berkshire Hathaway Inc.

- Source: Baur, D. G., & McDermott, T. K. (2025). Revisiting the hedging and safe haven roles of gold. Journal of International Financial Markets, Institutions and Money.

- Source: Source: Bloomberg, WisdomTree, 1973–2026. Past performance is not indicative of future results. Equities refers to the S&P 500 Index, specifically the price return, which does not include the impact of any dividend reinvestment. Gold refers to the LBMA gold price, calculated as of the afternoon fixing. The return is calculated as the 1 year period following the date specified, for example, the Israel-Hamas War was October 7, 2023, so the period would be from that date to October 7, 2024.

- Source: Federal Reserve Bank of Chicago. (2021). What drives gold prices? Chicago Fed Letter, No. 464.

- U.S. equities in the context of GDE refers to 500 U.S. large market capitalization stocks that are weighted on the basis of market capitalization.

Source: Buffett, W. E. (2011). Berkshire Hathaway Inc. 2011 annual letter to shareholders. Berkshire Hathaway Inc.

Source: Baur, D. G., & McDermott, T. K. (2025). Revisiting the hedging and safe haven roles of gold. Journal of International Financial Markets, Institutions and Money.

Source: Source: Bloomberg, WisdomTree, 1973–2026. Past performance is not indicative of future results. Equities refers to the S&P 500 Index, specifically the price return, which does not include the impact of any dividend reinvestment. Gold refers to the LBMA gold price, calculated as of the afternoon fixing. The return is calculated as the 1 year period following the date specified, for example, the Israel-Hamas War was October 7, 2023, so the period would be from that date to October 7, 2024.

Source: Federal Reserve Bank of Chicago. (2021). What drives gold prices? Chicago Fed Letter, No. 464.

U.S. equities in the context of GDE refers to 500 U.S. large market capitalization stocks that are weighted on the basis of market capitalization.

Important Risks Related to this Article

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

There are risks associated with investing, including possible loss of principal.

GDE: The Fund is actively managed and invests in U.S. listed gold futures and U.S. equity securities. The Fund’s use of U.S. listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models and the models may not perform as intended.

NTSX: While the Fund is actively managed, the Fund’s investment process is heavily dependent on quantitative models and the models may not perform as intended. The Fund invests in derivatives to gain exposure to U.S. Treasuries. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage and derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. Interest rate risk is the risk that fixed income securities, and financial instruments related to fixed income securities, will decline in value because of an increase in interest rates and changes to other factors, such as perception of an issuer’s creditworthiness.

Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For additional fund disclosures, click the respective ticker: IVV, AGG, GLD.

Categories

Related articles

The Periodic Table Has a Hidden Power Structure

Trump, Xi, and the Strategic Processing Reserve

Adding Alpha to Beta: A Capital-Efficient Solution

The Strategic Metals Underpinning Our Modern Technologies

Gold Monthly: Rebounding after a Violent Drawdown

Two Monetary Assets Walk into a Ratio

Adding, Not Replacing: Managed Futures in the Age of Efficient Capital

Adding, Not Replacing: Broad Commodities in the Age of Efficient Capital

The Month Gold Broke: Five Lessons from the ‘March Madness’ Selloff and the Rebound Opportunity

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.