EPI

India Earnings Fund

Published April 23, 2026

Global Head of Research

The Market Is Struggling. The Story Isn’t.

India has become one of those markets that everyone agrees on, until they look at performance.

The long-term narrative around India is clean and compelling. Everyone recognizes:1

And yet, in 2025 and into 2026, the experience, particularly with respect to the performance of India’s equity market, has been far less convincing.

India’s energy vulnerability has come back into focus. The conflict in the Strait of Hormuz has reminded investors just how exposed India remains to imported fuel and geopolitical shocks.

This is the tension, in one line:

India is a structurally bullish story running headfirst into cyclical and geopolitical reality.

Beneath the surface, India is not standing still. It is quietly attempting something far more ambitious:

India is seeking to redesign its energy system and its technological backbone at the same time.

India’s near-term vulnerability is straightforward.

India is not just an energy importer; it is structurally dependent on external supply.

India is the third-largest energy consumer in the world, yet imports roughly 85% of its crude oil needs and around 50% of its natural gas consumption.2 That places it among the most import-dependent large economies globally, certainly more exposed than the United States or China, though less extreme than countries like Japan or South Korea, which import nearly all of their fossil fuel needs.

Critically, a large share of India’s oil imports transit through the Strait of Hormuz, one of the most strategically vulnerable chokepoints in the global energy system. Roughly 20% of global oil flows pass through this corridor, meaning disruptions there are not just regional, they are systemic.3

For India, that creates a different kind of risk profile.

When geopolitical tensions rise, the issue is not just higher prices, but rather it is physical supply risk. Unlike more energy-secure economies, India cannot easily substitute domestic production or reroute supply at scale in the short term.

For a country trying to industrialize, digitize, and urbanize simultaneously, that’s not a trivial risk. It’s foundational, and India’s equity markets are reacting accordingly. Given volatility in the geopolitical situation around Iran as of this writing, we’d expect sensitivity to work both ways, meaning that if the perception of risk is falling, we might expect better performance from India’s equities, whereas if the perception of risk is rising, we might expect worse performance. None of that is certain, but it’s a reasonable mental model to have on the current situation.

But here’s what we think could be the more interesting framing:

What looks like a weakness in the short term is actively shaping India’s long-term strategy.

India doesn’t just want cheaper energy; it wants energy independence.

India’s energy strategy is not just about solar panels and wind farms. It is far more structurally ambitious, and also far more unique.

At the center is a decades-long effort to build a closed-loop nuclear fuel cycle, designed specifically around India’s resource constraints.

India has limited uranium, but roughly 25% of the world’s thorium reserves.4

That single fact has shaped one of the most unconventional nuclear strategies in the world: a three-stage program designed to turn thorium into a long-term, self-sustaining energy source.

The progression is deliberate:

This is no longer theoretical.

In April 2026, India’s Prototype Fast Breeder Reactor (PFBR) achieved first criticality, effectively marking entry into Stage 2.5

In our opinion, that milestone matters more than the market is currently pricing.

This is because fast breeder reactors do something critical:

They create fuel instead of just consuming it.

And if India successfully executes the third stage, which would manifest as thorium-based reactors, it unlocks something few countries have:

A pathway to centuries-scale domestic energy supply.

This is not a 2–3-year catalyst, but it could be a 20–30-year structural shift.

In our opinion, markets tend to underprice slow-moving transformations, until they suddenly matter.

If the nuclear story is about energy independence, the next layer is about energy demand. That demand is increasingly coming from Artificial Intelligence.

India is positioning itself as infrastructure in the current global AI buildout.

Data centers, semiconductor ambitions, and digital services are all accelerating. The country’s data center capacity alone is expected to scale dramatically, with power demand rising from ~13 TWh to ~57 TWh by 2030.6

That creates a simple but powerful equation:

Renewables alone don’t solve that, but Nuclear can.

This is where India’s strategy starts to look less like a collection of independent bets and more like a system:

At the same time, globally, AI is becoming less about flashy breakthroughs and more about scaling infrastructure, which means things like data centers, integration, and real-world deployment.

There’s another shift happening in parallel, and this is also one that we believe investors are currently underestimating.

India is moving from being a consumer of technology to a builder of technology ecosystems.

India’s technological ambition is no longer theoretical—it is increasingly visible in real supply chains.

Take Apple.

Over the past few years, India has emerged as a critical node in global iPhone manufacturing. Apple now produces roughly 15–20% of its iPhones in India, with ambitions to increase that share meaningfully as it diversifies away from China.7 What began as assembly has steadily moved up the value chain into components, supplier ecosystems, and export scale.

More broadly, India is actively positioning itself not just as a consumer of technology, but as a manufacturing and infrastructure backbone of the global digital economy.

At the core of this transition is a rapidly expanding semiconductor ambition. India’s semiconductor market, already estimated at ~$45–50 billion, is projected to reach $120 billion by 2030 and $300 billion by 2035, driven by demand from mobile devices, electric vehicles, and data centers.8

But this is not just about demand. It is about control.

India currently imports over 90% of its semiconductor needs, leaving it exposed to global supply chain disruptions and geopolitical fragmentation.9 The response has been a deliberate push toward domestic capacity, for example through incentives, fabrication plans, and a growing ecosystem of assembly, testing, and packaging facilities.

This is happening alongside a broader reconfiguration of global supply chains.

As companies rethink resilience, India is emerging as a beneficiary, not just because of cost advantages, but because of scale, political alignment, and long-term policy support.

So how should investors think about India today?

It’s tempting to focus on what’s not working:

But that, in our opinion, risks missing the broader dynamic.

India is not a clean, linear growth story. It is a transitional one—where short-term volatility is real, but long-term positioning is steadily improving. In many ways, today’s headwinds are shaping tomorrow’s strengths. Energy shocks are accelerating the push toward domestic energy security. Geopolitical tensions are reinforcing the need for supply chain independence. And rising AI demand is justifying large-scale investments in infrastructure. What looks like weakness may, in fact, be investment in resilience.

India, over the better part of 2025 and now 2026, has not been easy for investors. It has required patience, a tolerance for volatility, and a willingness to look beyond the next quarter. But the underlying trajectory, in our opinion, is becoming clearer. This is a country attempting to build energy independence, scale digital infrastructure, and embed itself in the next phase of global technological development, and it is doing these things all at once. That may create friction, but it could also create opportunity. In our view, the markets that feel most uncomfortable today are often laying the foundations for tomorrow’s growth.

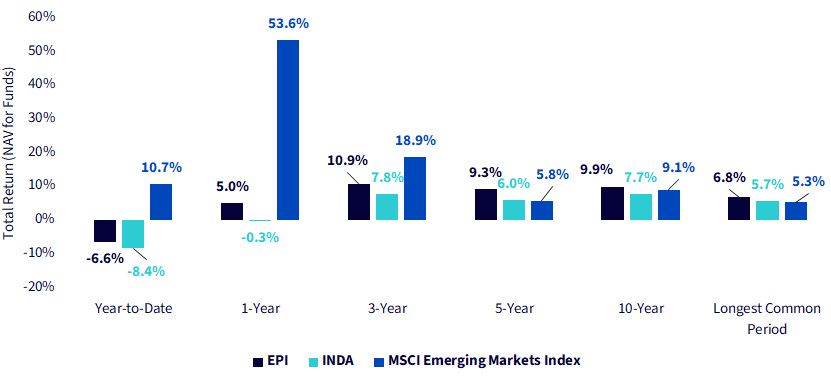

The WisdomTree India Earnings Fund (EPI) is designed to track the total return performance, before fees and expenses, of the WisdomTree India Earnings Index. Figure 1a shows how both EPI and the iShares MSCI India ETF (INDA)10 have underperformed the broader MSCI Emerging Markets Index.

In our view, the year-to-date and one-year periods represent the ‘challenge’ of being an investor in India’s equities of late. The nice thing about Figure 1a is it also shows the longer run, simply as a reminder that India’s equities have performed well in the past and the long-term picture does not look like the more recent picture. It’s simply a matter of trying to provide a fuller historical context.

If the market begins to appreciate the efforts that India has been making, and that we have detailed, maybe there could be an equity market opportunity in this particular market.

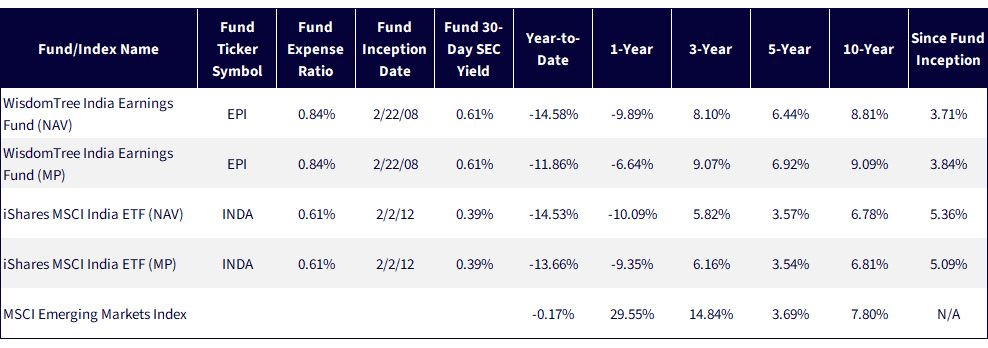

Sources: Morningstar, FactSet and WisdomTree, specifically, data is from the PATH Fund Comparison Tool, accessed as of April 13, 2026, but showing returns for the period ended April 10, 2026 for Figure 1a and March 31, 2026, for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: EPI, INDA.

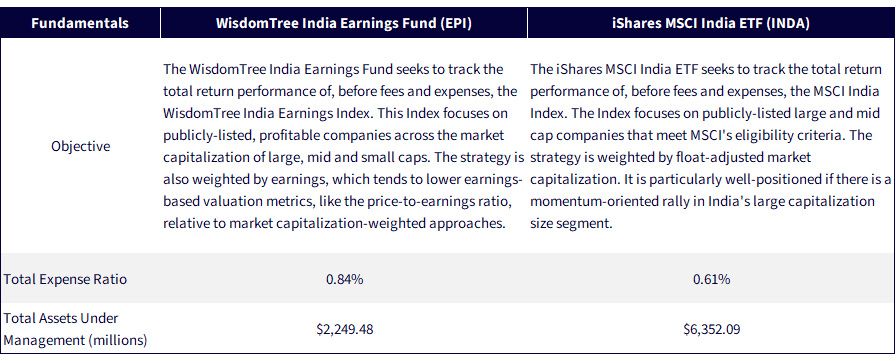

Sources: Respective fund pages, with assets under management data as of April 10, 2026. Subject to change.

United Nations, Department of Economic and Social Affairs, Population Division. (2023). World population prospects 2022: Summary of results. United Nations; World Bank. (2024). India development update: Sustaining growth amid global uncertainty. World Bank Group; Pew Research Center. (2021). The expanding global middle class: India; Bain & Company. (2023). India’s digital economy report 2023.

Sources: International Energy Agency. (2023). India energy outlook 2023. IEA; U.S. Energy Information Administration. (2024). India country analysis brief.

Source: U.S. Energy Information Administration. (2023). World oil transit chokepoints.

Source: U.S. Energy Information Administration. (2024). India country analysis brief.

Source: Press Information Bureau, Government of India. (2026, April 7). Prototype fast breeder reactor at Kalpakkam attains first criticality.

Source: Deloitte & NITI Aayog. (2025). India’s data center surge: Navigating capacity growth, real estate pressure and power readiness. Deloitte.

Source: Bloomberg News. (2026, March 10). Apple now makes about 25% of iPhones in India after China pivot.

Source: Deloitte. (2026). Technology, media and telecommunications predictions 2026: India chapter. Deloitte.

Source: Deloitte. (2026). Technology, media and telecommunications predictions 2026: India chapter. Deloitte.

This is the largest ETF focused specifically on India’s equities, tracking the MSCI India Index benchmark index before fees and expenses.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund invests in the securities included in, or representative of, its Index regardless of its investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For INDA's risk disclosures, click here.

India Earnings Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.