OPPE

European Opportunities Fund

Published April 9, 2026

Global Head of Research

Macro Strategist, Model Portfolios

Currency is often treated as a background variable that can be hedged away, neutralized, or simply ignored. But in the current environment, that framing could overlook potentially compelling investment opportunities. When we see the distinct macro regimes playing out across major economies, each creating its own currency narrative, we think those narratives can be actionable. They are leading us to lean into certain currency exposures while stepping back from others.

This framing turns currency from a passive decision into an active lever within the opportunity set.

The Japanese yen sits at the center of the current currency discussion, not because it is the most volatile, but because it appears to be the most anchored. There is a clear sense, both from policymakers and market behavior, that levels around 160 USD/JPY represent something close to a soft ceiling.1

This is not a formal policy target, but rather something more subtle. When the yen weakens toward 160, we have seen signaling behavior: recent comments from Japanese officials,2 in the past, “rate checks” from the U.S. Treasury,3 and a broader sense that policymakers are increasingly uncomfortable with further depreciation. These signals do not guarantee intervention, but they do not need to. Markets have tended to respond preemptively.

In our view, what makes this particularly interesting is that the macro backdrop in Japan does not justify a dramatically weaker currency. Corporate performance has been solid, global capital continues to find its way into Japanese equities, and the economy itself is behaving more constructively than it has in years.4 A move toward 160 starts to look less like equilibrium, in our opinion, and more like an overshoot.

We think this creates a relatively well-defined range, from about 150 to 160, that can be used as a tactical framework.

At the upper end of that range, when the yen is weak, the argument is to dial down the hedge. In practical terms, that means allowing for more unhedged exposure so that portfolios can participate if and when the yen strengthens. The asymmetry here is important—policy signaling tends to emerge more forcefully at these weaker levels, increasing the probability of mean reversion.

At the lower end of the range, closer to 145–150, the calculus shifts. The currency has already strengthened, and the risk-reward of further appreciation becomes less compelling. That is where the argument turns toward dialing the hedge back up, locking in gains and reducing exposure to potential reversals.

The yen, in other words, is not a currency that demands a fixed stance. It is a currency that we think rewards dynamic positioning within a policy-influenced range.

If the yen is defined by policy signaling, the euro is defined by policy divergence. In this context, we reference the divergence in forward-looking messaging coming from the European Central Bank (ECB) and the U.S. Federal Reserve.

At present, that divergence is becoming more pronounced. The ECB, and to a similar extent the Bank of England, have leaned more hawkish in its recent communications.5 Discussions around rate hikes remain active, and there is little emphasis on near-term cuts. By contrast, the Federal Reserve is closer to a holding pattern, with the market still contemplating potential easing further out.6

That difference matters. Currency markets are highly sensitive to forward-looking interest rate expectations, and when one region appears structurally more hawkish than another, capital tends to follow the yield differential.

However, the European story is not without complication. Inflation in Europe is not being driven by excess demand in the same way it might be in the United States. Instead, it is heavily influenced by energy costs. Europe’s relative lack of energy independence means that geopolitical shocks, particularly in the Middle East, translate more directly into higher costs for consumers and businesses.7

This creates a somewhat uncomfortable reality: the ECB may be tightening policy in response to inflation drivers that monetary policy cannot fully address. Raising rates does not produce more energy supply. Yet, from a currency perspective, the distinction matters less than the signal, as a central bank that is perceived as hawkish still tends to be more bullish for its currency versus a central bank that is perceived as less hawkish.

In our view, if policy divergence continues to favor Europe over the United States, the euro has a reasonable case for appreciation, or at least for stabilizing after recent weakness. In that environment, the argument is to dial down the hedge on euro exposure.

Moving beyond the euro, the United Kingdom presents a similar, though not identical, story. The Bank of England has also exhibited a hawkish bias, with members of its Monetary Policy Committee openly discussing the possibility of rate hikes.8 Inflation remains persistent enough to justify that stance, and there has been little indication of a rapid pivot toward easing.

In our opinion, this places the British pound in a comparable position to the euro. While the underlying economic structures differ, the policy signal is aligned: relatively tighter monetary conditions compared to the United States.

As a result, the hedging approach follows a similar logic. There is a case for reducing hedge ratios, allowing for some exposure to potential currency strength driven by policy expectations.

But Europe is not a monolith, and as we move further into the region, the narratives become more fragmented.

Poland & the Czech Republic

Countries like Poland and the Czech Republic introduce a different dynamic. Their economies have performed relatively well, and their central banks have maintained a cautiously hawkish stance. In Poland’s case, there is an additional layer of complexity: increasing gold reserves and a growing role in regional defense spending. Over time, these factors could contribute to a perception of greater currency stability or strategic importance.9

Still, these are not currencies that dominate portfolio outcomes from an overall exposure perspective in the same way as the euro or yen. Their influence is more incremental, and so too is the hedging decision.

The Nordic currencies, particularly the Norwegian krone, introduce yet another dimension: commodity linkage.

Norway’s position as a major energy exporter means that its currency behaves, to a meaningful degree, like a proxy for oil and gas prices. When energy prices rise, the krone tends to strengthen. When they fall, it weakens.10

This shifts the hedging question away from central banks and toward commodity markets. The decision to hedge or not hedge becomes, in part, a view on the direction of energy prices.

If the outlook for oil and gas is constructive, there is a rationale to dial down hedging, allowing portfolios to benefit from potential currency appreciation. If the outlook weakens, the opposite holds: increase hedging to mitigate downside risk.

This is a different type of currency exposure, in our opinion less about policy and more about global supply-demand dynamics.

Finally, there is the Swiss franc, which occupies a unique position in the currency landscape.

Unlike many of its peers, the franc is heavily managed. Swiss authorities have historically taken an active role in limiting excessive appreciation or depreciation, resulting in a currency that tends to move within a relatively constrained range.11

For investors, this creates a different opportunity. The franc is not typically a source of directional return. Instead, it offers stability—and, importantly, the potential to earn carry while maintaining a hedge.

In this case, the argument is straightforward: maintain a higher hedge ratio. The limited volatility reduces the opportunity cost of hedging, while the carry component can enhance returns.

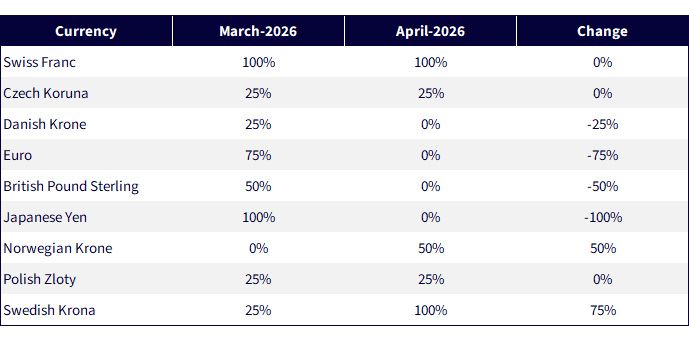

Figure 1 brings this narrative together, showing how the currency hedge ratios looked in March 2026 and what changed, based on our aforementioned thinking, for April of 2026.

Source: WisdomTree, with data for March 2026 implemented after the close of trading on 2/27/2026, and for April 2026 implemented after the close of trading on 3/31/2026. Change refers to the change from March-2026 to April-2026. Currency exposures are based on a baseline U.S. dollar exposure. These currency hedging ratios impact OPPJ and OPPE WisdomTree ETFs that are described in the conclusion of this article. Currency Hedge Ratios are subject to change.

These currency narratives point toward a broader conclusion. In our view, hedging currency exposure can be a dynamic process, informed by the evolving macro environment.

The yen offers a range-bound, policy-sensitive opportunity to adjust exposure tactically. The euro and pound reflect policy divergence, creating a case for selective participation in currency strength. The Nordic currencies tie into commodity cycles, requiring a different analytical lens. And the Swiss franc provides a stable anchor, where hedging can be maintained with confidence.

What unites these perspectives is not a single directional call, but a framework. Currency becomes another lever, one that can be adjusted incrementally to align with changing conditions.

In the opportunities strategies at WisdomTree, that flexibility is not just beneficial. It is essential. The specific strategies that apply these currency exposures as of April 2026 are:

Source: Katayama, S. (2026, March 26). Remarks on foreign exchange movements and potential intervention measures. Ministry of Finance, Japan.

Source: Katayama, S. (2026, March 26). Remarks on foreign exchange movements and potential intervention measures. Ministry of Finance, Japan.

Source: Grossman, M., & Douglas, J. (2026, January 24). Treasury “rate check” boosts yen, weakens dollar. The Wall Street Journal.

Sources: J.P. Morgan Asset Management. (2025). Japan’s corporate governance reforms boost shareholder value; Du, L., & Sano, N. (2026, March 23). Berkshire Hathaway to invest $1.8 billion in Tokio Marine. Bloomberg; Goldman Sachs. (2026). Japan economic outlook 2026: Steady fundamentals, policy risks ahead.

Sources: European Central Bank. (2026, March 19). Monetary policy statement and press conference; Bank of England. (2026, March 19). Monetary Policy Committee summary and minutes.

Source: Board of Governors of the Federal Reserve System. (2026, March 19). Federal Open Market Committee

Source: European Central Bank. (2026, March 25). Navigating energy shocks: Risks and policy responses.

Source: Bank of England. (2026, March 19). Monetary policy summary and minutes of the Monetary Policy Committee meeting ending on 18 March 2026.

Sources: Czech National Bank. (2026, February 12). Monetary policy report – Winter 2026; Narodowy Bank Polski. (2026). Interest rate and macroeconomic data.

Source: Norges Bank. (2025). Monetary Policy Report 2/2025.

Source: Swiss National Bank. (2026, March). Monetary policy assessment and communication on foreign exchange intervention.

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty

OPPJ: The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

OPPE: This Fund focuses its investments in Europe, thereby the impact of events and developments associated with the region can adversely affect performance. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Derivative investments can be volatile, and these investments may be less liquid than other securities, and more sensitive to the effects of varied economic conditions. Derivatives used by the Fund may not perform as intended. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs.

Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.