DGRW

U.S. Quality Dividend Growth Fund

Published February 24, 2026

Global Head of Research

In 2013, we developed what is now known as WisdomTree’s Quality Dividend Growth methodology. At the time, many of the largest technology companies paid no dividend at all. Today, it is increasingly difficult to find mega-cap tech firms that are not returning cash to shareholders and growing those payments consistently. Markets have evolved, leadership has shifted and volatility has come and gone, but the discipline of focusing on profitable companies with sustainable dividend growth has endured. As we move through early 2026’s market turbulence, it is worth stepping back and reassessing nearly 13 years of live results through a long-term lens, focusing on some of the largest exchange-traded funds (ETFs) that represent strategies targeting this concept of ‘dividend growth1.

When I start looking at results, I try to simplify the picture into three things:

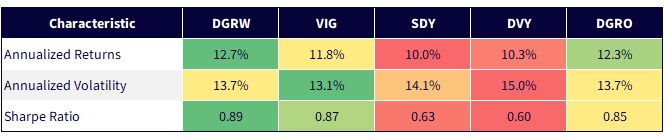

We see the results in Figure 1a.

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 13, 2026 with returns as of February 12, 2026, and both volatility and Sharpe ratio as of December 31, 2025. The period for these statistics starts as far back as possible for all strategies shown, June 10, 2014, the inception for DGRO. Green indicates a more favorable level for a characteristic, measured relative to the other ETFs, whereas red indicates a less favorable level for that characteristic. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

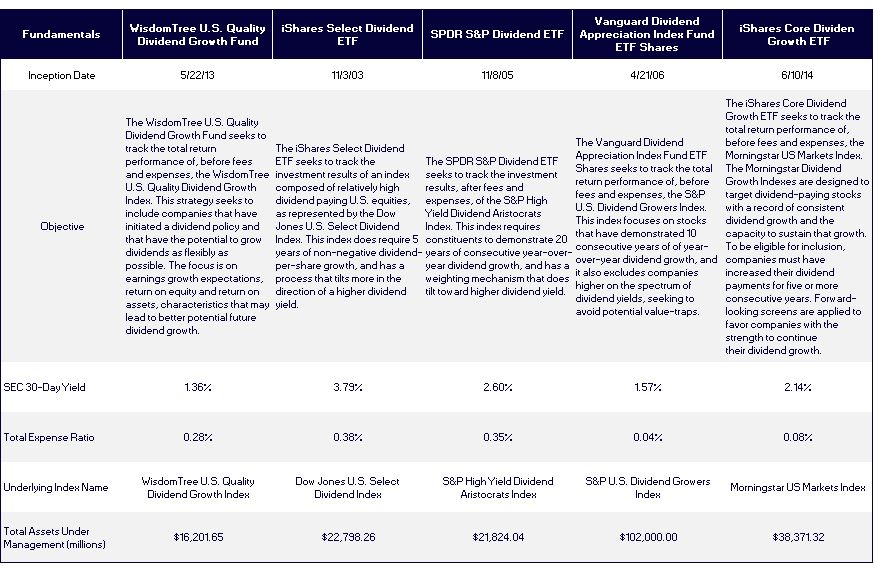

To help with further context:

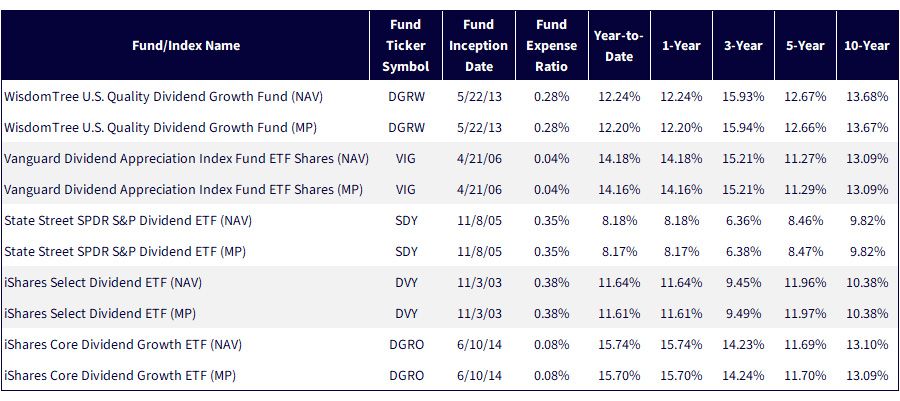

Of course, there are nuances to each of these approaches, but the overall focus is the same—large-cap stocks, predominantly, with a specific policy of looking at the underlying dividend behavior of underlying constituents. DGRW is the only approach in which the underlying strategy is not focused on past dividend growth behavior.

Sources: WisdomTree, FactSet specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 13, 2026 with returns as of December 31, 2025. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: DGRW, VIG, SDY, DVY, DGRO.

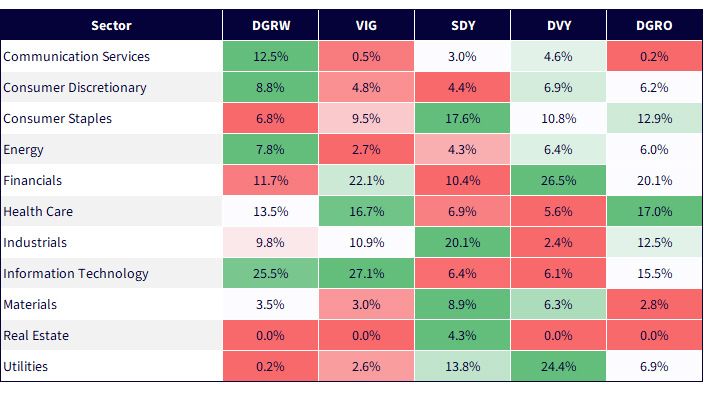

On the surface, each strategy sits under the banner of “dividend growth.” But the sector exposures tell a far more nuanced story. Some approaches lean heavily into Technology and Communication Services, capturing the structural shift toward cash-generative mega-cap growth. Others tilt meaningfully toward Utilities, Financials or Industrials, reflecting a more traditional income orientation. These differences are not cosmetic; rather, they shape return patterns, volatility profiles and drawdown behavior over full cycles. Analysis of dividend policies and potential growth may be a common thread, but sector composition could have a big impact on how each portfolio participates in market leadership, economic sensitivity and structural change. The overall concept may be similar. The economic exposure is not.

Sources: WisdomTree, FactSet, Morningstar, with data as of January 31, 2026. Green refers to a larger sector exposure for a given strategy, whereas red refers to a smaller sector exposure for a given strategy. Subject to change.

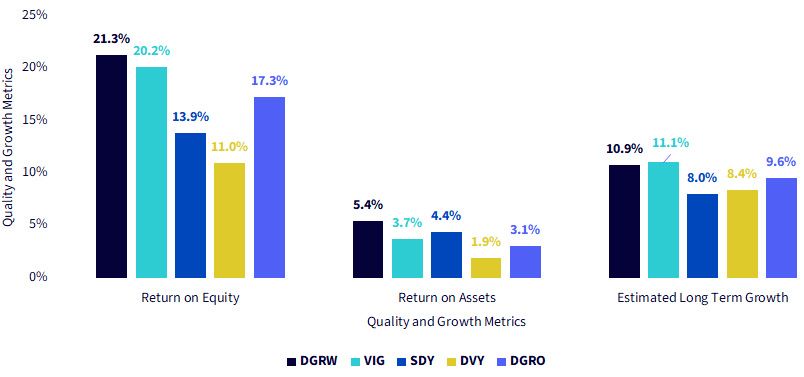

Sector weights are not just about economic sensitivity; they meaningfully influence fundamental characteristics. Strategies like SDY and DVY, with larger allocations to Utilities, tend to exhibit lower average return on equity and return on assets, reflecting the capital-intensive and regulated nature of that sector. Earnings growth expectations also tend to be more modest, consistent with stable but slower-growing cash flows. By contrast, portfolios with heavier exposure to Information Technology and Communication Services typically show stronger profitability metrics and higher expected earnings growth, driven by asset-light business models and structural revenue expansion. Over time, those fundamental differences can compound into materially different risk-adjusted outcomes.

Sources: WisdomTree, FactSet, Morningstar, with data as of January 31, 2026. Green refers to a larger sector exposure for a given strategy, whereas red refers to a smaller sector exposure for a given strategy. Subject to change.

Dividend growth is not a monolith. Sector exposure, profitability and earnings growth expectations meaningfully shape long-term outcomes. In calmer markets, those differences can feel subtle. During volatility, they compound. Investors concerned about valuation risk are often concerned about durability—owning businesses that can sustain cash flows and adapt across cycles. A disciplined focus on quality and growth does not eliminate drawdowns, but it can help position portfolios with stronger foundations when uncertainty inevitably resurfaces.

Sources: Fund sponsor websites and fund pages, with assets under management data current as of February 12, 2026. Subject to change.

1 The ETFs were selected as among the largest ETFs by assets under management as of February 2026 that have, in their underlying index, a focus on some measure of ‘dividend growth’ for underlying constituents.

2 Yield refers to dividend-yield.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or

restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not

believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed

fund.

DGRW: There are risks associated with investing, including possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund is non-diversified, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For additional fund disclosures, click the relevant ticker: VIG, SDY, DVY, DGRO.

U.S. Quality Dividend Growth Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.