GCC

Enhanced Commodity Strategy Fund

Published January 23, 2026

Global Head of Research

In the world of commodity investing, category names can obscure critical strategy differences. Funds grouped under the same "broad commodities" label can behave very differently depending on how they allocate across sectors, manage risk, and navigate futures curves. Understanding those differences is essential, because they ultimately determine whether a portfolio captures diversification—or simply concentrates exposure in unexpected places.

The WisdomTree Enhanced Commodity Strategy Fund (GCC) incorporates an active strategy that takes into account both an enhanced roll methodology alongside a broader, research-driven strategic allocation. Enhanced roll in this context refers to attentiveness to contango (negative roll yield) and backwardation (positive roll yield). Minimizing contango while leaning into backwardation, where possible, is the underlying logic of the strategy. GCC also represents a widely diversified approach, typically spanning around 26 contracts and up to 5% bitcoin exposure.

By contrast, the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC), the category leader by AUM1, tracks the DBIQ Optimum Yield Diversified Commodity Index. The DBIQ Optimum Yield Diversified Commodity Index is a rules-based commodity futures index designed to provide broad, diversified commodity exposure while seeking to enhance roll yield. The index allocates across energy, metals, and agricultural commodities based on a combination of market liquidity and global production metrics, subject to sector and commodity caps. Rather than rolling futures on a fixed schedule, each commodity selects the futures contract along the curve with the highest implied roll yield, aiming to benefit from backwardation and mitigate contango. The index is rebalanced annually, with additional safeguards to prevent excessive concentration during periods of extreme price movements.

The First Trust Global Tactical Commodity Strategy Fund (FTGC) takes yet another approach as an actively managed, long-only commodity futures strategy designed to deliver diversified commodity exposure with controlled volatility2. Rather than weighting commodity exposures by production or market size, the portfolio uses quantitative models to forecast volatility and correlations across a broad universe of liquid commodity futures contracts. Portfolio weights are constructed to target a consistent risk profile and avoid over-concentration in any single commodity or sector. The strategy is rebalanced regularly and includes active contract selection along the futures curve, seeking to improve roll yield and manage contango and backwardation dynamics.

GCC, FTGC, and PDBC all provide diversified commodity exposure and fall within the same Morningstar Category, but they reflect two distinct schools of portfolio construction.

GCC and FTGC are actively managed strategies that emphasize risk-aware portfolio design rather than static index weights. GCC combines discretionary oversight with systematic signals, such as term structure, carry, and momentum, to dynamically allocate across commodity exposures, seeking to improve roll yield and performance across market regimes. FTGC also departs from an index-tracking construction, using quantitative models to forecast volatility and correlations across a broad commodity universe, then constructing a portfolio targeted to a relatively stable risk profile. While both are active, GCC places greater emphasis on regime sensitivity and tactical positioning, whereas FTGC focuses more on volatility targeting and diversification efficiency.

PDBC, in contrast, is fully rules-based. Its methodology allocates commodities using liquidity and global production metrics, then systematically selects futures contracts with the highest implied roll yield along the curve. Rebalancing follows predefined schedules and constraints, with limited discretion.

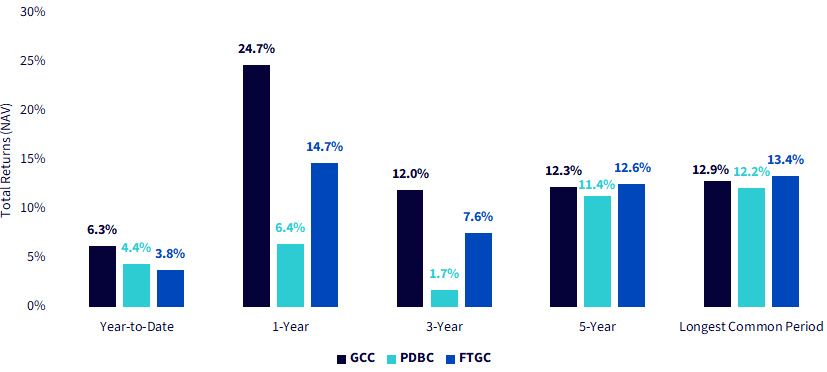

While it's important to know, in our opinion, which strategies are active, which are passive and what the overall strategy is seeking to achieve, we understand that the first evaluation that many investors will do regards performance. Figure 1a shows:

Figure 1a: When Methodology Matters: A Multi-Year Test of Commodity ETF Design

Figure 1b: Standardized Returns

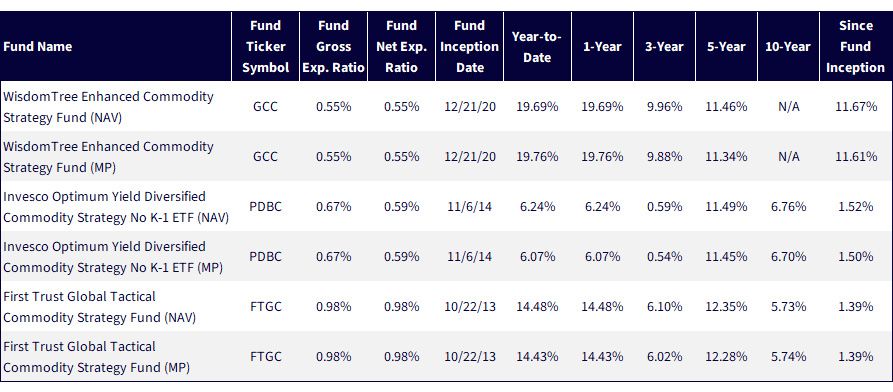

Sources: WisdomTree, FactSet specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed January 14, 2026, with returns in Figure 1a as of 1/13/26, and in Figure 1b as of 12/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click the relevant ticker:GCC, PDBC, FTGC.

The Bottom Line Drivers of Differentiated Returns

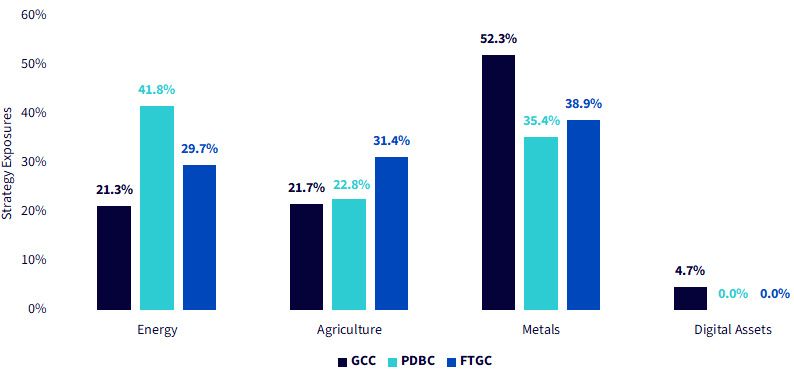

Figure 2 allows us to understand the underlying commodity exposures from a clearer perspective:

Figure 2: Portfolio DNA Across Ags, Metals, and Digital Assets

Sources: WisdomTree, FirstTrust and Invesco product pages, with data as of 1/13/26. Subject to change.

Conclusion: Why Commodity Exposure Demands Clarity

For investors seeking real asset exposure, not all "broad commodity" strategies are created equal, and the differences are rarely obvious from the label alone. While commodities are often framed as a single inflation hedge or macro diversifier, the reality is that portfolio behavior is driven by underlying sector exposures. When a large share of a strategy is anchored to energy, outcomes can end up reflecting oil market dynamics far more than broader real asset trends.

This is why looking under the hood matters for allocators. Commodity investing is not a monolith; it is a collection of distinct, volatile sub-sectors, energy, metals, agriculture, and increasingly digital assets, each responding to different economic and geopolitical forces. Rules-based approaches like PDBC deliver systematic exposure shaped by production and liquidity weights, while active strategies such as FTGC and GCC introduce risk management and discretion. The distinction lies in how deliberately those tools are used.

A more flexible, actively managed approach, like GCC, allows sector exposures to evolve with changing regimes, reducing reliance on any single commodity complex and increasing the likelihood of participating in emerging themes, from industrial metals demand to gold's role in central bank reserves or the growing institutional relevance of bitcoin. For allocators, the takeaway is straightforward: choose the exposure that reflects your conviction. Otherwise, your commodity allocation may behave very differently than you expect.

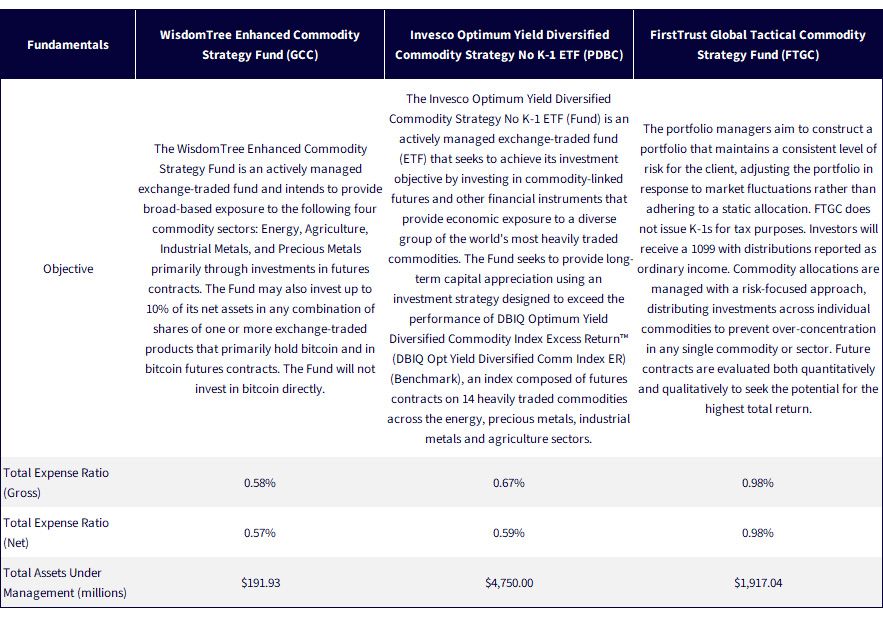

Figure 3: Additional Information

Sources: WisdomTree's fund compare tool, which utilizes data from FactSet and Morningstar. Assets under management is from the individual fund sponsor websites and is as of 1/14/26.

1 The category refers to the Morningstar Commodities Broad Basket category of U.S. listed ETFs. As of December 31, 2025, PDBC was the largest fund by AUM in this category.

2 As of December 31, 2025, FTGC was the largest fund in the Commodities Broad Basket category, defined by Morningstar, that was not tracking the return of any underlying index.

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

GCC: There are risks associated with investing including possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk, and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors which contribute to the Fund's performance. These factors include use of commodity futures contracts. In addition, bitcoin and bitcoin futures are a relatively new asset class. They are subject to unique and substantial risks, and historically, have been subject to significant price volatility. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relate directly to the value of the futures contracts and other assets held by the Fund and any fluctuation in the value of these assets could adversely affect an investment in the Fund's shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”) and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

For PDBC risk disclosures, click here.

For FTGC risk disclosures, click here.

Enhanced Commodity Strategy Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.