DGRW

U.S. Quality Dividend Growth Fund

Published December 1, 2025

Global Head of Research

When equity markets are breaking records and optimism feels effortless, it's tempting to believe the good times will simply continue. Yet history shows that the best moment to think about risk is precisely when everything looks strong. It's at the peaks, when valuations are rich, volatility is forgotten and economic data hums, that portfolios are most vulnerable to complacency. The paradox of investing is that the calm before turbulence is often when prudent investors are building resilience. You don't buy insurance after the storm; you position before the clouds form.

Managing risk effectively isn't about predicting the next sell-off, it's about preparing the portfolio architecture that can endure one. The investors who navigate downturns most successfully tend to identify, in advance, the strategies that have demonstrated an ability to hold up when markets fall. These approaches, often rooted in quality, consistent profitability and disciplined capital return, don't rely on market timing. They rely on selecting businesses built to sustain earnings power when conditions deteriorate. In other words, resilience isn't a trade; it's a trait.

That's why periods of strength are the best time to evaluate the defensive foundations of a portfolio. When indexes are near record highs and risk feels invisible, investors have the freedom to reposition from strength rather than from fear. Cultivating exposure to high-quality, dividend-growing companies is one of the clearest ways to prepare for inevitable drawdowns while staying invested in the market's upside. This is the philosophy behind the WisdomTree U.S. Quality Dividend Growth Fund (DGRW),1 designed to track the performance of companies that blend profitability, growth and discipline—attributes that tend to matter most when sentiment shifts.

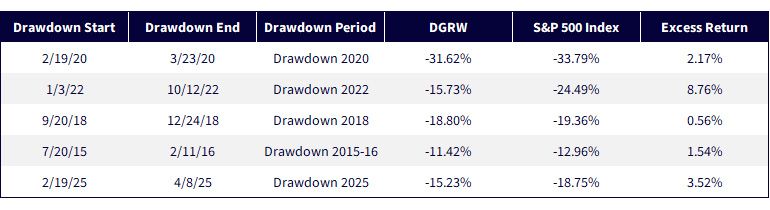

Proven Resilience through Market Stress

The idea of positioning for resilience before markets turn is only as powerful as the evidence that it works. Since its inception in 2013, DGRW has faced five major drawdowns of 10% or greater in the S&P 500 Index.2 Each period offered a real-world test of the strategy's design: can a portfolio built on profitability, disciplined growth and dividend sustainability actually preserve more capital when broader markets sell off?

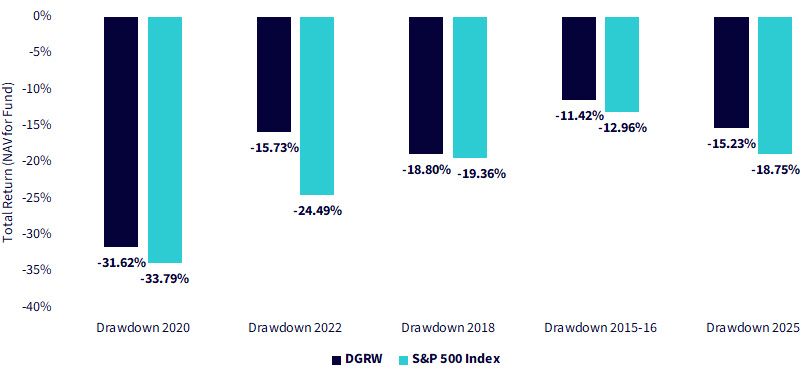

As is illustrated in the detailed table that follows (figure 2a) and then the more intuitive bar chart (figure 2b), across all five drawdowns, DGRW outperformed the S&P 500 Index, cushioning declines in each case. That 2022 spread, an 8.8% excess return during one of the most punishing years for equities in over a decade, illustrates why structural quality and disciplined dividend weighting can matter more than short-term market narratives. This evidence reinforces our core thesis: the time to think about risk is when the market feels strongest. The takeaway is not that quality dividend growth guarantees protection in every downturn, but that its structural emphasis on capital efficiency and sustainability has repeatedly shown value in periods when it's mattered most.

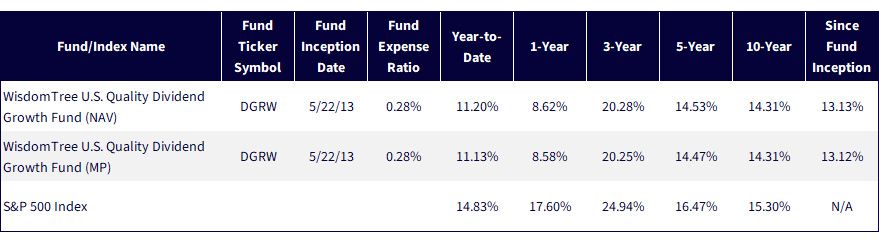

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 10/23/25 with returns as of 9/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

Figure 2a: How Did DGRW Do during Drawdowns?

Sources: WisdomTree, FactSet, S&P, with data current as of 10/23/25. Past performance is not indicative of future results. You cannot invest directly in an index.

Figure 2b: Illustrating the Downside Mitigation over These Periods

Sources: WisdomTree, FactSet, S&P, with data current as of 10/23/25. Past performance is not indicative of future results. You cannot invest directly in an index.

If the last few years have taught investors anything, it's that market leadership can become extraordinarily narrow, and that it can change quickly. Today, the S&P 500 Index's returns are dominated by a handful of companies with extremely large market capitalizations, many at the heart of the artificial intelligence revolution. Their profitability and innovation are undeniable, but so are the risks that come with such concentration and elevated valuations. For allocators, the challenge is to participate in the innovation narrative without letting portfolio risk be swamped by it.

The WisdomTree U.S. Quality Dividend Growth Index, which DGRW tracks, approaches this challenge structurally rather than tactically. By weighting companies by their share of the U.S. dividend stream, not their market capitalization, the Index naturally reins in exposure to the largest mega-cap growth names. The logic is simple: dividends act as a stabilizing force, and companies must generate and return real cash to shareholders to maintain weight. As a result, size alone doesn't confer dominance; financial productivity does.

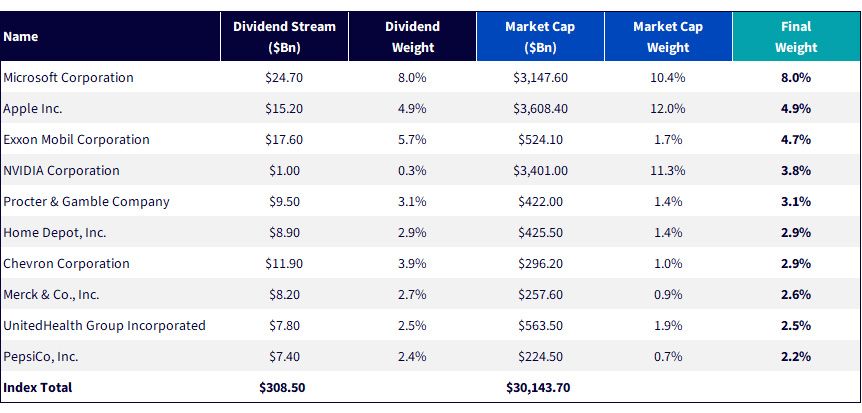

This design doesn't exclude technology leadership, it reframes it. Microsoft, Apple and Nvidia all appeared among the top holdings, but their weights (8.0%, 4.9% and 3.8%) reflect a balance between growth and capital discipline. Compare this with their combined market-cap weight of over 33% in the S&P 500, and you see the difference: DGRW allows participation in the innovation cycle without letting the portfolio become a momentum derivative of it.3

At a moment when debates around AI valuations and concentration risk are intensifying, DGRW's construction functions as a quiet form of risk management. The methodology ensures:

The outcome is a portfolio aligned with the economic reality of U.S. corporate profitability, rather than the market narrative of the moment. That design distinction becomes increasingly valuable when markets may be priced for perfection and the next leg up of returns may depend less on excitement and more on execution.

Figure 3: How WisdomTree's Rebalance Mitigated Concentration Risk

Sources: WisdomTree, Bloomberg, S&P. Data is as of the 2024 annual screening date, 11/29/24. Dividend Stream refers to the regular dividend per share multiplied by the number of shares outstanding. Should the ratio of a security's weight relative to its weight in a market capitalization-weighted version of the Index reach about 3x or fall below 0.33x, the weight of the company will be reduced or increase to meet the 3x or the 0.33x thresholds. Sector exposures will be capped at the less of the 20% or 2x their weight in a market capitalization-weighted version of the initial universe of eligible securities prior to the final selection of 300 companies.

One of the most overlooked strengths of a rules-based strategy like DGRW is that it removes personal judgment from the process. Inclusion and weighting are not based on opinion, market sentiment or narrative alignment. Instead, they're driven by measurable fundamentals. Every company in the WisdomTree U.S. Quality Dividend Growth Index earns its place by scoring highly across three objective metrics: return on equity (ROE), return on assets (ROA) and forward-looking earnings growth estimates.

Consider two of the largest names in U.S. pharmaceuticals that are visible in figure 4, Eli Lilly and Johnson & Johnson. Both are household names, both generate billions in revenue, and both pay dividends. Yet only one currently qualifies for inclusion.

The takeaway is not that one company is "better" than the other, it's that the data determines eligibility. DGRW's framework rewards businesses where high profitability converges with genuine growth potential, not just brand reputation or historical dominance.

Figure 4: A Tale of Two Pharmaceutical Companies at the 2024 Index Screening

Source: WisdomTree, FactSet, with data as of the 2024 Index screening date for the WisdomTree U.S. Quality Dividend Growth Index.

When markets are strong and optimism is the default setting, investors face a subtle but critical choice: to ride the wave uncritically, or to use the calm to reinforce the hull. History rewards those who prepare before the storm.

DGRW is not a forecast, it's a framework. It's built on the belief that the best defense against uncertainty is ownership in companies that combine profitability, discipline and genuine growth potential. That philosophy has proven its worth through five market drawdowns, consistently cushioning losses without abandoning participation in the recovery that follows.

Today's market may be defined by AI narratives, record valuations and narrow leadership, but the principles that drive long-term compounding haven't changed. DGRW's construction ensures exposure to innovation without dependence on it, capturing dividend-paying growth companies across sectors where capital efficiency is rewarded and excess is filtered out.

Risk management isn't about pessimism. It's about building endurance when the wind is at your back, so that momentum becomes sustainability. Investors can't predict the next drawdown, but they can choose to be ready for it. DGRW exists precisely for that decision: a way to stay invested, stay disciplined and stay strong when strength still feels easy.

1 DGRW is built to track the total return performance, before fees and expenses, of the WisdomTree U.S. Quality Dividend Growth Index.

2 Sources: WisdomTree, S&P, through 6/30/25. Past performance is not indicative of future results.

3 Exposures to these companies along with data in figure 3 were calculated as of the 2024 annual screening date for the WisdomTree U.S. Quality Dividend Growth Index.

For current holdings of DGRW, please click here. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. Quality Dividend Growth Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.