OPPJ

Japan Opportunities Fund

Published September 12, 2025

Global Head of Research

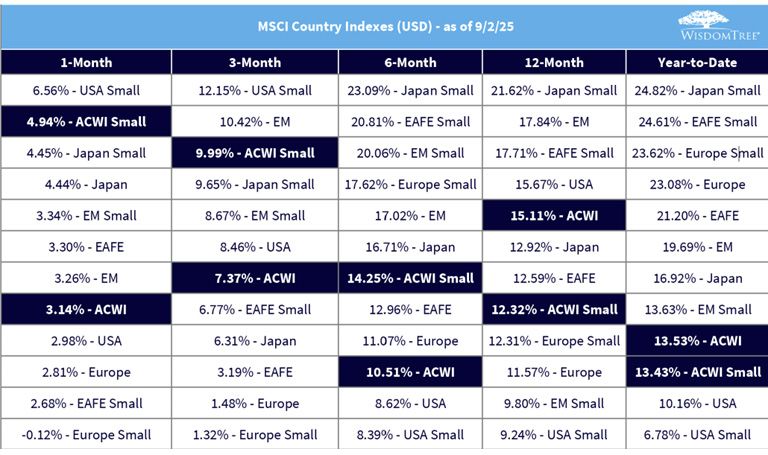

Over the past several months, Japan has quietly gone from global laggard to one of the most intriguing bright spots in global equities. The numbers make the case. While most peers have delivered steady but unremarkable returns, Japan's acceleration stands out. In figure 1:

Markets often turn on inflection points, and Japan is beginning to look like one of those shifts in trajectory.

What makes this surge compelling isn't only the absolute returns, but the relative positioning. Compare Japan with the U.S., commonly associated with the term "US exceptionalism." In figure 1, the U.S. is visible in the lower half of the chart for most of the time periods.

Figure 1: Japan Surges, U.S. Stalls: Shifting Leadership in Global Markets

Sources: WisdomTree, MSCI. You cannot invest directly in an index. Past performance is not indicative of future results. Each box in figure 1 represents an MSCI Index (e.g., ACWI is the MSCI ACWI Index, ACWI Small is the MSCI ACWI Small Cap Index), and each can be interpreted analogously. EM stands for emerging markets.

Professionally Managing a Concept from Warren Buffett

The WisdomTree Japan Opportunities Fund (OPPJ) began in July 2025, and the timing was deliberate. Japan is not simply in a rebound cycle; it is undergoing a structural re-rating of its corporate culture. At the center of the strategy are the five sogo shosha, Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo.1 These trading houses are more than conglomerates. They are diversified ecosystems spanning energy, commodities, logistics, finance and consumer markets, miniature versions of Berkshire Hathaway itself.

Warren Buffett has singled them out for their rare blend of traits: steady dividend growth, opportunistic buybacks and management teams that display notable restraint in executive compensation. In a country long criticized for corporate inertia, Buffett's endorsement marked a turning point.2

And this wasn't a passing comment. In both the 2023 and 2024 Berkshire letters, Buffett made clear that stakes in the five houses, now roughly 9% of each,3 were meant to be permanent. "Forever" is a concept Buffett has historically reserved for what he views as some of the strongest businesses, two examples of which could be Coca-Cola and American Express.4 To apply it to Japanese firms acquired only in 2019 speaks volumes about Berkshire's conviction.

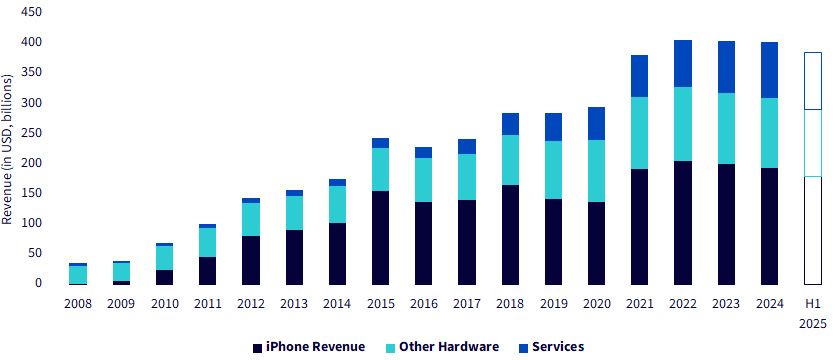

This makes the juxtaposition with Apple all the more fascinating. Apple has been one of the greatest trades in Berkshire's history. From a cost basis of about $36 billion beginning in 2016, Berkshire amassed more than 900 million shares at its peak. By mid-2025, it had sold well over $100 billion worth of Apple stock, locking in profits on a scale rarely seen in market history. Even after these sales, Berkshire still owns roughly 280 million shares worth $57.4 billion, making Apple its single largest equity holding.5

Yet the philosophy has shifted, as is visible in figure 2. Apple's core engine, the iPhone, has plateaued. Services and other hardware have taken on more importance, but overall revenues have leveled off. The chart below tells the story clearly: Apple's once-relentless growth curve has flattened, and the dependence on iPhone sales remains hard to ignore.

Figure 2: Apple's Revenue Machine: Plateau after a Decade of Expansion

Sources: "Apple Inc.," Wikipedia; Joseph D'Souza, "Apple Statistics by Revenue and Facts (2025)," Sci-Tech Today, 6/24/25; "Apple Inc. (AAPL), Metrics, Revenue by Segment," StockAnalysis.com, 6/30/25. We have created the H1 2025 bar as an outline only because it represents the true data for H1 2025, which we then annualized by doubling the three figures to estimate the full-year pace we have seen through 6/30/25.

Buffett and Abel are signaling something profound. Apple, once described as untouchable, is clearly no longer a forever holding. Japan's trading houses now carry that designation.

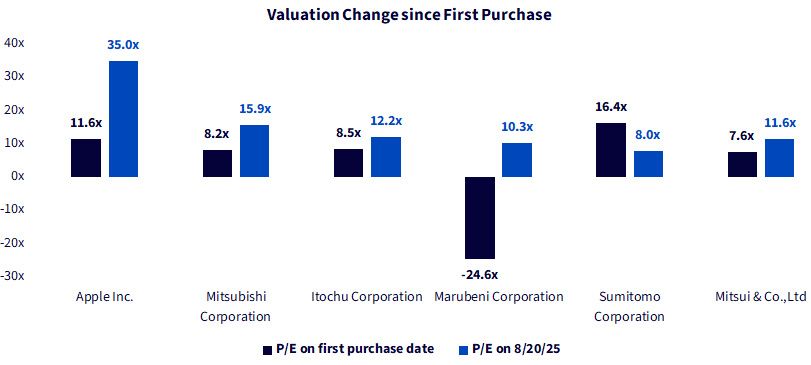

Buffett's Japan purchases began on July 4, 2019, the baseline for measuring how valuations have evolved.6 Since then, Apple's price-to-earnings multiple has exploded from 11.6 times at entry to about 35 times today. The sogo shosha? Their valuations have barely budged, in some cases even compressing, as is visible in figure 3.

This divergence is the crux of the opportunity. Apple's success has already been priced in. Japan's trading houses, despite Berkshire's involvement and improving fundamentals, remain conservatively valued. Figure 3 makes it plain: Apple's multiple has tripled, while Japan's remain stubbornly cheap.

Figure 3: Valuations Tell the Story: Apple Stretched, Japan Still Undervalued

Sources: WisdomTree, FactSet. First purchase date refers to 7/4/19, the date when Buffett indicated Berkshire began building positions in the five Japanese companies. Past performance is not indicative of future results.

Here's the catch: Berkshire itself is capped. It cannot push ownership in the trading houses beyond 9.9% without regulatory hurdles. That ceiling locks Buffett out of buying more, even if his conviction deepens. OPPJ faces no such limits. With roughly 45% of its weight in the "Buffett Basket" of the five Japanese trading houses, it gives investors access to the very exposure Buffett wishes he could own at a greater scale.

But OPPJ goes further. The portfolio layers in three additional pillars, of corporate governance improvers, capital-return champions and thematic opportunities. These complement the trading houses with a broader set of Japanese companies that are buying back stock, raising dividends and aligning compensation with shareholder value. This is not a cultural aspiration anymore. It's happening. Shareholder payouts in Japan have quadrupled over the past decade, with buybacks alone now eclipsing the total dividends of just 10 years ago.

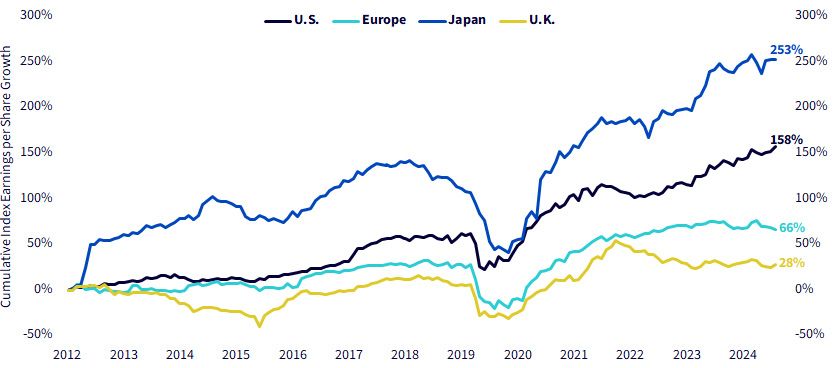

While the Buffett Basket anchors OPPJ, the strategy intentionally looks beyond. Japan's transformation is visible in its fundamentals.

Figure 4 highlights cumulative earnings per share growth since 2012 across major developed markets. Japan's trajectory is striking, surpassing both Europe and the U.K., and narrowing the gap with the U.S. The so-called "Japan discount" persists, but the earnings power is real and rising.

Sources: WisdomTree, MSCI, for the period 12/31/12–7/31/25. U.S., Europe, Japan and U.K. are measured by respective MSCI Index universes. Earnings growth is measured in local currency. You cannot invest directly in an index.

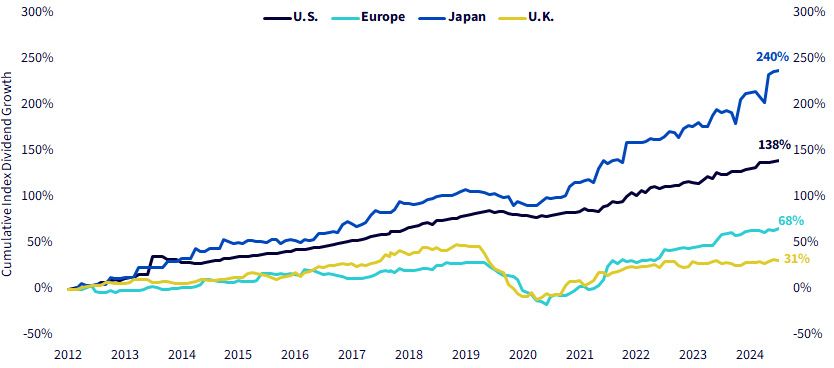

The second chart shows dividends. Over the same period, Japan's dividend growth has outpaced peers by a wide margin. Once criticized for hoarding cash, Japanese companies are now returning capital with discipline and consistency. Investors are no longer waiting for governance reforms to show up in numbers, they already have.

Figure 5: From Cash Hoards to Cash Back: Japan's Dividend Surge

Sources: WisdomTree, MSCI, for period 12/31/12–7/31/25. Dividends are from trailing 12-month periods. Regions represented by respective MSCI country indexes. Dividends are measured in local currency terms. Past performance is not indicative of future returns. You cannot invest directly in an index.

Conclusion: What's Priced In?

Going back to Apple, we'd clearly note that we don't see a revenue problem. We do see a valuation in the range of 35 times earnings that we believe has an inherent expectation of future growth that may not materialize. At a lower valuation, it could represent an opportunity.

We've seen the five trading houses currently held by Berkshire and major exposures within OPPJ, and we have seen the overall earnings and dividend growth in Japan relative to other markets. It's clear that there are positive fundamentals, but the question is, what is priced in?

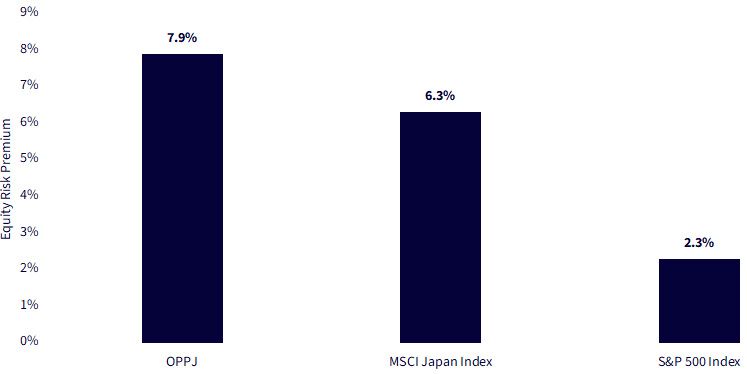

Figure 6 showcases the equity risk premium, which is defined as the earnings yield of a given index minus the 10-year real interest rate for that market.

You can multiply the equity risk premium of the S&P 500 Index by three and still not quite reach the OPPJ figure, a stark contrast. Many may believe that Japan's equities should have a lower valuation than those of the U.S., but this is quite a significant margin. It could signal an opportunity.

Figure 6: Equity Risk Premiums Diverge: Japan Offers More than 3x the U.S.

Sources: WisdomTree, Bloomberg, MSCI, as of 7/29/25. Past performance does not guarantee future results. You cannot invest directly in an index. Subject to change.

Taken together, the case is compelling. Apple's extraordinary run has rewarded Berkshire handsomely, but its valuation leaves little room for compounding. Japan, by contrast, offers discounted valuations, shareholder-friendly reforms and global relevance, ingredients that echo Buffett's favorite playbook of buying wonderful businesses at fair prices and holding them indefinitely.

That's the essence of OPPJ. It professionally replicates Buffett's Japan strategy, while broadening the lens to capture a country in the midst of an earnings and dividend renaissance. In a world of stretched U.S. multiples and crowded trades, Japan stands out as a market where patience, discipline and valuation still converge.

As of 8/21/25, Itochu, Marubeni, Mitsubishi, Mitsui and Sumitomo had weights of 8.56%, 9.97%, 9.11%, 8.81% and 8.85%, respectively, in OPPJ. Holdings are subject to change.

Sources: "2024 Annual Report," Berkshire Hathaway Inc., 2025; "2023 Annual Report," Berkshire Hathaway Inc., 2024.

Source: "Berkshire Hathaway Raises Stakes in Five Japanese Trading Houses to Near 10%," Reuters, 3/17/35.

Source: J. Baer, "What Warren Buffett Learned from His Biggest Hits, and Misses," The Wall Street Journal, 5/4/25.

Source: E. Kim, "Warren Buffett Hails Tim Cook for Making Berkshire More Money than He Has, after Selling Two-Thirds of His Apple Stake," Business Insider, 5/3/25.

Source: "2023 Annual Report to Shareholders," Berkshire Hathaway Inc., 2024.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations, derivative investments which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Japan Opportunities Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.