OPPJ

Japan Opportunities Fund

Published July 1, 2025

Global Head of Research

Global Chief Investment Officer

Japan's equity markets have experienced a generational reset, with a sweeping re-rating of corporate governance, capital discipline and global relevance that is steadily dismantling three decades of a well-warranted "Japan discount."

An early signal came not from Tokyo bureaucrats or activist hedge funds but from Omaha—when Warren Buffett acquired shares in five Japanese trading companies.1

In Berkshire's 2023 shareholder letter, Buffett explained that Berkshire "continues to hold its passive and long-term interest in five very large Japanese companies, each of which operates in a highly diversified manner somewhat similar to the way Berkshire itself is run… Berkshire now owns about 9 percent of each of the five."2

A year later, he continued his conviction: "As the years have passed, our admiration for these companies has consistently grown… Both of us like their capital deployment, their managements and their attitude in respect to their investors."3 He singled out steady dividend growth, opportunistic buybacks and restrained executive pay; exactly the behaviors Tokyo's stock exchange is now demanding from all companies trading below book value.4

Those governance tailwinds are measurable. Aggregate return on equity (ROE) for TOPIX constituents has doubled over the past decade; net cash balances are falling as boards shrink share counts; and a domestic household savings pool of ¥2 quadrillion is finally edging out of low-yielding bonds and cash into equities.5

Overlay a structurally weak yen, which turbocharges export earnings and attracts foreign inflows, and valuations start to look less like "cheap for a reason" and more like mispriced optionality on global growth.

Buffett also wishes he could own more of these five trading companies, but he is constrained regarding how much capital he can put to work—due to targeting a 10% ownership level.6 As of May 30, 2025, WisdomTree has positioned its new Japan Opportunities Fund (OPPJ)7 to allocate approximately 45% to these trading companies to help individual investors capitalize on the opportunity in a way that Buffett himself cannot. Specifically, this refers to how Berkshire Hathaway's equity allocation is constrained due to its size and that it is already quite close to 10% ownership of these stocks. It's possible that one day Berkshire may negotiate avenues through which to own more than 10% of these companies, but based on available information today, it is not yet the case. OPPJ, on the other hand, does not have a similar constraint on allocating more to these particular stocks.8

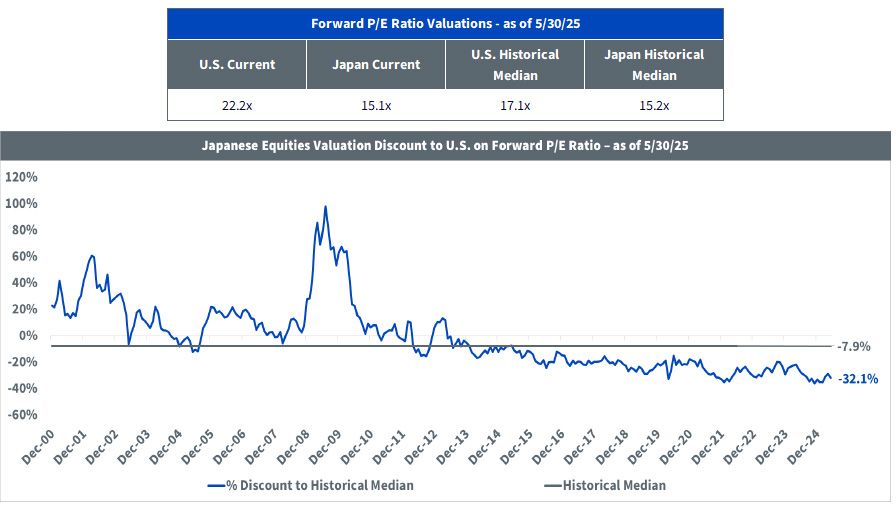

Despite a powerful rally in Japanese equities over the past year, the valuation story remains deeply compelling. As is visible in figure 1, Japan trades at a forward price-to-earnings ratio (P/E ratio) of 15.1x—not only below the U.S. (22.2x) but even slightly below its own long-term median (15.2x).

The real headline, however, is the valuation spread: Japanese equities sit at a 32% discount to the U.S. on forward P/E, one of the widest relative gaps in the past two decades.

For a market undergoing a structural shift in governance, capital efficiency and foreign capital inflows, the message is clear: this generational reset is not priced as such.

Figure 1: A Generational Opportunity: Japan Trades at a 32% Discount to U.S. Equities

Sources: WisdomTree, FactSet, S&P, MSCI, 12/31/00–5/30/25. U.S. measured by S&P 500 Index. Japan measured by MSCI Japan. You cannot invest directly in an index. Past performance is not indicative of future returns.

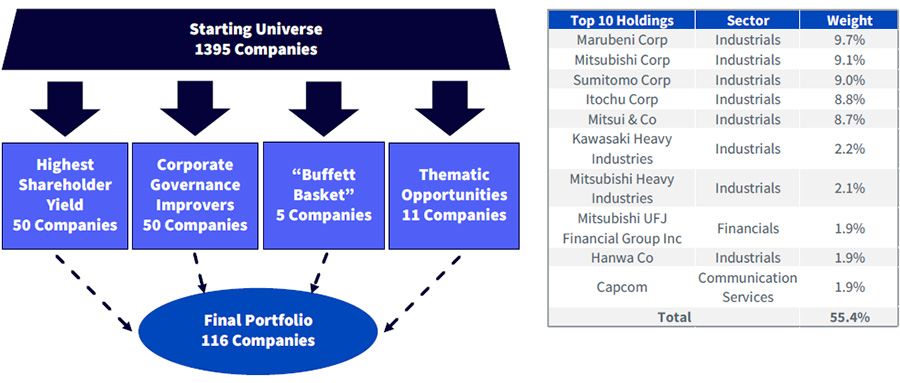

Figure 2 gives a blueprint for understanding the high-level construction of OPPJ.

Figure 2: Transforming Cheap into Outperformance: The Four-Pillar Blueprint

Source: WisdomTree, with data shown as of 5/30/25. You cannot invest directly in an index.

Together, these four pillars create a Japan opportunities portfolio that is both anchored in attractive quality valuations and wired for possible upside catalysts.

From Cash Hoarding to CashBack: Japan's Capital-Return Revolution

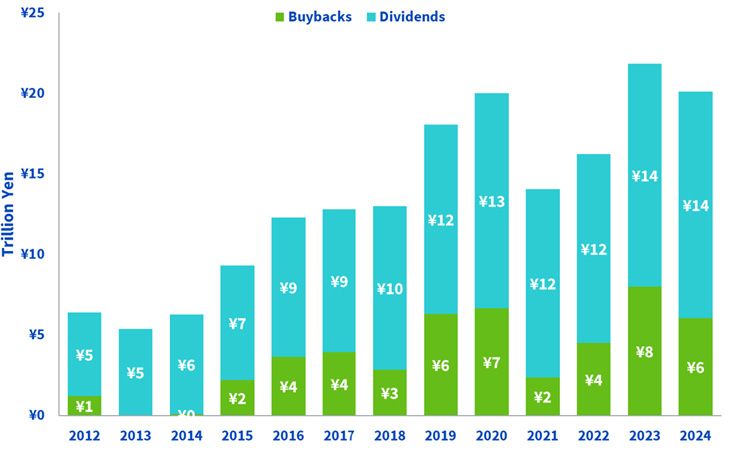

Barely a decade ago, Japanese corporates were infamous for sitting on mountainous cash piles; buybacks were an afterthought, and dividend yields trailed those of their global peers.

As is visible in figure 3, in 2012, companies returned roughly ¥6 trillion to shareholders, almost entirely via modest dividends. Fast-forward to 2024, and total capital returned has quadrupled to about ¥20 trillion, with buybacks alone now exceeding the whole 2012 payout.

This surge coincides with Japan's Corporate Governance and Stewardship Codes (2014–15) and the Tokyo Stock Exchange's more recent "name-and-shame" campaign; reforms that pressured boards to deploy idle cash, shrink bloated balance sheets and tie executive pay to shareholder value.9

This pivot is more than an accounting footnote; it is a structural re-rating catalyst. Rising buybacks shrink float and boost per-share earnings just as dividend growth establishes a floor under valuations.

In short, capital return has shifted from theoretical aspiration to tangible, compounding reality—and our portfolio is designed to turn that tailwind into excess return.

Figure 3: From Cash Hoards to Cash Back: Japan's Shareholder Payouts Rocket Roughly 4xin a Decade

Sources: WisdomTree, MSCI, as of 12/31/24. Payouts measured on a trailing 12-month basis each May month-end. Japanese payouts based on MSCI Japan Index. You cannot invest directly in an index.

Conclusion: Turning Japan's Reset into a Shareholder Renaissance

Japan today is not the Japan of yesterday. When Warren Buffett devotes multiple shareholder letters to the country's corporate champions and then quietly lifts Berkshire's stake to more than 9% in five of them and suggests he will hold them for decades, it's an important signal.

The world's most disciplined value investor sees a market in the early innings of a structural re-rating: one that now combines global business models with cleaner governance, better capital allocation and multi-decade low valuations.

The reset is real. And it's unfolding in plain sight, at a time when much of the world remains preoccupied with crowded trades and stretched multiples elsewhere. The WisdomTree Japan Opportunities Fund is purpose-built for this moment.

Investors aren't just getting access to a country; they're getting exposure to a fundamentally upgraded equity culture—one where value is finally being unlocked, and shareholders are finally being paid.

1 Source: W. E. Buffett, "Berkshire Hathaway Inc. 2023 Annual Shareholder Letter," Berkshire Hathaway, 2024. https://www.berkshirehathaway.com/letters/2023ltr.pdf

2 Source: Buffett, 2024.

3 Source: W. E. Buffett, "Berkshire Hathaway Inc. 2024 Annual Shareholder Letter," Berkshire Hathaway, 2025. https://www.berkshirehathaway.com/letters/2024ltr.pdf

4 Source: Japan Exchange Group,"List of companies disclosing progress on initiatives to enhance corporate value," Tokyo Stock Exchange, 1/15/24. https://www.jpx.co.jp/english/news/1020/20240115-01.html

5 Sources: "Japan ROE for TOPIX index constituents," stock market data, 2024; "Chart Room: Japan Inc's buyback spree," Fidelity International, 2/22/24; "The recent rise of Japan's financial markets: A look at household savings behavior and NISA reform," government of Japan, 3/24.

6 Source: Buffett, 2025.

7 Prior to July 1, 2025, the Fund was known as the WisdomTree Japan Hedged SmallCap Equity Fund (DXJS). On that date, the Fund's policy changed.

8 Due to market performance, this weight may fluctuate up or down as time goes by.

9 Source: "Japan's Corporate Governance Code: Seeking Sustainable Corporate Growth and Increased Corporate Value over the Mid- to Long-Term" (final proposal, 3/5/15), Financial Services Agency & Tokyo Stock Exchange, 2015.

Warren Buffett is not affiliated with WisdomTree or OPPJ.

There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. This Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Japan has and may continue to experience security concerns, war, threats of war, aggression and/or conflict, terrorism, economic uncertainty, sanctions or the threat of sanctions, natural and environmental disasters, the spread of infectious illness, widespread disease or other public health issues and/or systemic market dislocations that lead to increased short-term market volatility and have adverse long-term effects on Japan and world economies and disrupt the orderly functioning of securities markets generally, which may negatively impact the Fund’s investments. Because the Fund invests primarily in the securities of companies in Japan, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Japan and to be more volatile than the performance of more geographically diversified funds. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The Fund invests in derivatives in seeking to obtain a dynamic currency hedge exposure. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations and derivative investments. Derivatives investment can be volatile, and these investments may be less liquid than other securities and more sensitive to the effect of varied economic conditions. Derivatives used by the Fund may not perform as intended. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger-capitalization stocks or the stock market as a whole. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Japan Opportunities Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.