DXJ

Japan Hedged Equity Fund

Published March 18, 2025

Global Head of Research

Global Chief Investment Officer

One of our favorite annual events occurs when Warren Buffett, Chair and CEO of Berkshire Hathaway, publishes his annual shareholder letter.

WisdomTree has focused on Japanese equities all the way back to the election of Prime Minister Shinzo Abe in December 2012.1 "Abenomics" revitalized the country's macro backdrop and catapulted the Nikkei to finally surpass the former 1989 peak—a feat taking more than 30 years.2

This period highlighted to U.S. investors to the importance of currency exposure when investing in non-U.S. equities. When investors looked at their unhedged exposures, they saw these figures were quite different from the Japanese market in yen terms.

Buffett has historically ventured outside of the U.S., but the vast majority of his allocation has been to the U.S. It is tough to argue against this, and it also forces us to pay that much closer attention when we do see references to non-U.S. equity exposures.

Buffett focused multiple paragraphs of the 2023 and 2024 Annual Letters on his Japan investments, and in each of these years he also mentioned how he benefited from thinking about his equity exposure while mitigating and hedging his currency exposure—something WisdomTree has been advocating for since 2012.

Buffett wrote in 2023, "Neither Greg nor I believe we can forecast market prices of major currencies. We also don't believe we can hire anyone with this ability."3

WisdomTree created indexes and ETFs that neutralize the impact of currency fluctuations on returns—in other words, that hedge the currency exposure—and allows the investor to do two things:

1. Gain exposure to the performance of the equities in the local market without any direct influence of the currency's exchange rate changing.

2. Gain exposure to the difference in short-term interest rates, since the tool being used is one-month non-deliverable forward contracts. If the U.S. interest rate is higher, the U.S. investor is able to collect the difference between the U.S. short-term interest rate and the Japanese short-term interest rate. However the equities perform, this can be thought of as another source of incremental return.

Buffett has access to other, more complex tools, writing:

Berkshire has financed most of its Japanese position with the proceeds from ¥1.3 trillion of bonds. This debt has been very well-received in Japan, and I believe Berkshire has more yen-denominated debt outstanding than any other American company. The weakened yen has produced a year-end gain for Berkshire of $1.9 billion, a sum that, pursuant to GAAP rules, has periodically been recognized in income over the 2020–23 period.4

Buffett is essentially borrowing money in Japan at a much lower interest rate than would be available in the U.S. and then taking the proceeds and investing them in Japanese equities. The key point is that he is exposed to the performance of the companies in the local market and pocketing the spread of the lower cost of borrowing in Japan.

In 2024, he wrote:

Meanwhile, Berkshire has consistently—but not pursuant to any formula—increased its yen-denominated borrowings. All are at fixed rates, no "floaters." Greg and I have no view on future foreign exchange rates and therefore seek a position approximating currency-neutrality. We are required, however, under GAAP rules to regularly recognize in our earnings a calculation of any gains or losses in the yen we have borrowed and, at year-end, had included $2.3 billion of after-tax gains due to dollar strength of which $850 million occurred in 2024.5

For anyone curious about how the cost of the debt compares to a certain aspect of the return of the Japanese equities, Buffett writes, "We like the current math of our yen-balanced strategy as well. As I write this, the annual dividend income expected from the Japanese investments in 2025 will total about $812 million and the interest cost of our yen-denominated debt will be about $135 million."6

It's always fun to pick up the breadcrumbs that Buffett gives us about his investments, since he is known to never disclose anything until well after it happens. In his 2023 letter, Buffett wrote:

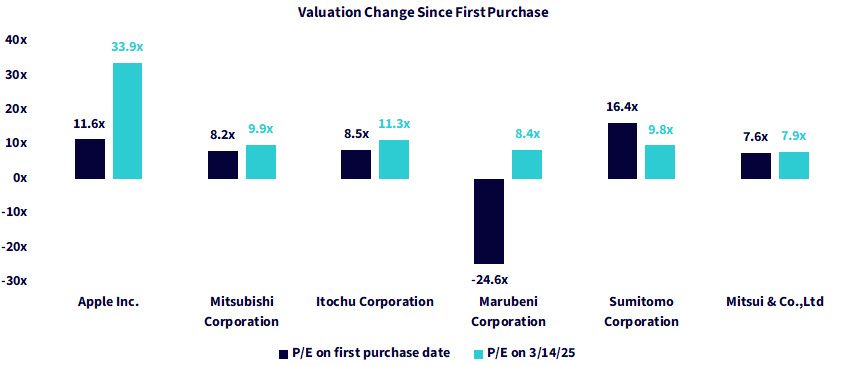

Our Japanese purchases began on July 4, 2019. Given Berkshire's present size, building positions through open-market purchases takes a lot of patience and an extended period of "friendly" prices. The process is like turning a battleship. That is an important disadvantage which we did not face in our early days at Berkshire.7

The companies are, "(alphabetically) ITOCHU, Marubeni, Mitsubishi, Mitsui and Sumitomo. Each of these large enterprises, in turn, owns interests in a vast array of businesses, many based in Japan but others that operate throughout the world."8

In terms of the rationale behind taking up these positions, Buffett wrote, "We simply looked at their financial records and were amazed at the low prices of their stocks."

Let's pull up some reference points to the actual valuation of these names. When it says "first purchase date," remember the aforementioned July 4, 2019:

Sources: WisdomTree, FactSet. The first purchase data is as of 7/4/19. Past performance is not indicative of future results.

Continuing with Buffett's Letters, "As the years have passed, our admiration for these companies has consistently grown. Greg has met with them many times, and I regularly follow their progress. Both of us like their capital deployment, their managements and their attitude in respect to their investors."11

Speaking of the ultimate vote of confidence, on March 17, 2025, it was reported that Berkshire has been buying even more of these five stocks, upping its stakes to between 8.5% and 9.8% according to regulatory filings12.

At WisdomTree, we have had a focus on dividends since we launched our first strategies in 2006, and we have run strategies focused on shareholder yield—favoring companies that decrease rather than increase their share issuance—since 2017.13 Buffett writes of his five Japan investments, "Each of the five companies increase dividends when appropriate, they repurchase their shares when it is sensible to do so, and their top managers are far less aggressive in their compensation programs than their U.S. counterparts."14

Buffett has noted many times that his favorite investment holding period is forever,15 emphasizing the benefit of a long-term focus where the compounding of returns can have time to build its impact. We see many investors focusing on the U.S. market with a long-term mindset, but it often feels like they hold non-U.S. markets to a different standard—if these markets underperform the S&P 500 or Nasdaq 100 Indexes for certain periods, we see a lot of focus back on the U.S. and away from lagging international markets.

Buffett writes of his Japan positions:

Our holdings of the five are for the very long term, and we are committed to supporting their boards of directors. From the start, we also agreed to keep Berkshire's holdings below 10% of each company's shares. But, as we approached this limit, the five companies agreed to moderately relax the ceiling. Over time, you will likely see Berkshire's ownership of all five increase somewhat. At yearend, Berkshire's aggregate cost (in dollars) was $13.8 billion and the market value of our holdings totaled $23.5 billion.16

As we noted, during the time we took publishing this article it has already been announced that Berkshire has been buying more shares in these companies17.

While it is fascinating to dissect the thoughts and positions of Warren Buffett over time, most cannot hope to copy exactly what he is doing. However, if there are investors who are thinking about a long-term Japan equity exposure, we at WisdomTree do have a particular tool that could be worth a further look.

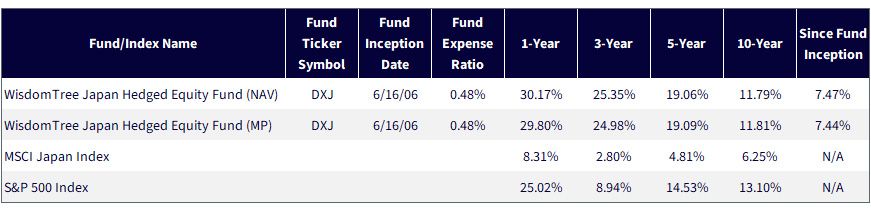

The WisdomTree Japan Hedged Equity Fund (DXJ) is designed to track the total return performance, before fees and expenses, of the WisdomTree Japan Hedged Equity Index. This strategy focuses solely on Japanese companies that pay dividends and generate less than 80% of their revenues from inside of Japan—in other words, those that focus on exporters.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 3/11/25 with returns as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

We have been hearing a lot about and seeing many headlines covering U.S. equity performance exceptionalism. Depending on where you see the article and who wrote it, it might be arguing U.S. equity leadership can continue…or it may be arguing the future could look different. Now, the period that makes us think about the strong U.S. equity performance is largely the recovery from the Covid-19 pandemic lows, just about five years back from the present day.

If we look at figure 3:

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 3/11/25 with returns as of 3/10/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

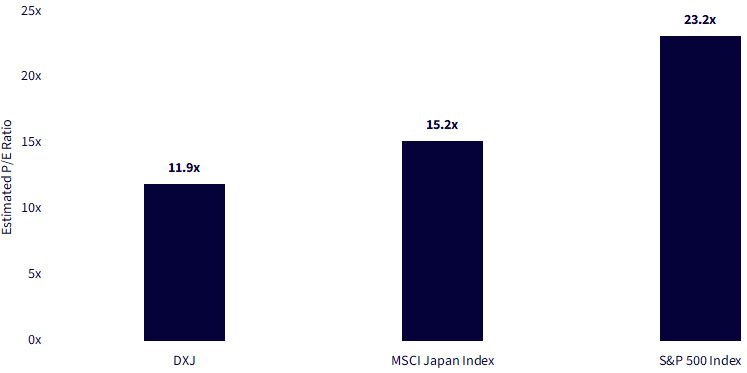

Even after those returns, if you were to ask, what is the valuation picture, you would see that Japan is still relatively much less expensive than the U.S. We see that in the forward P/E ratio comparisons in figure 4.

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 3/11/25 with fundamentals as of 2/28/25. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance and to download the respective Fund prospectuses, click here.

If people are thinking that they have a lot of U.S. exposure and need that international diversification, Japan, in our opinion, is a very interesting market to consider.

1 Source: https://en.wikipedia.org/wiki/2012_Japanese_general_election

2 Source: Laura He, "Japan's Stock Market Cheers First Record High in 34 Years," CNN, 2/22/24.

3 Source: 2023 Letter.

4 Source: 2023 Letter.

5 Source: 2024 Letter.

6 Source: 2024 Letter.

7 Source: 2023 Letter.

8 Source: 2024 Letter.

9 Source: 2024 Letter.

10 Source: Sean Williams, "Billionaire Warren Buffett Sold 67% of Berkshire's Stake in Apple and Is Piling into a Beloved Consumer Brand Whose Stock Has Soared by 7,000% since Its IPO," Yahoo! Finance, 11/18/24.

11 Source: 2024 Letter.

12 Japan's FSA Electronic Disclosure for Investors' Network, or EDINET.

13 Source: Refers to the WisdomTree Value Fund (WTV). The Fund's objective changed, effective 12/18/17. Prior to 12/18/17, Fund performance reflects the investment objective of the Fund when it tracked the performance, before fees and expenses, of the WisdomTree U.S. LargeCap Value Index.

14 Source: 2024 Letter.

15 Source: Buffett wrote the following in his 1988 shareholder letter: "When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever." https://www.berkshirehathaway.com/letters/1988.html

16 Source: 2024 Letter.

17 Japan's FSA Electronic Disclosure for Investors' Network, or EDINET.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations, and from derivative investments, which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Japan Hedged Equity Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.