WDEF

Europe Defense Fund

Published August 25, 2025

Global Head of Research

Macro Strategist, Model Portfolios

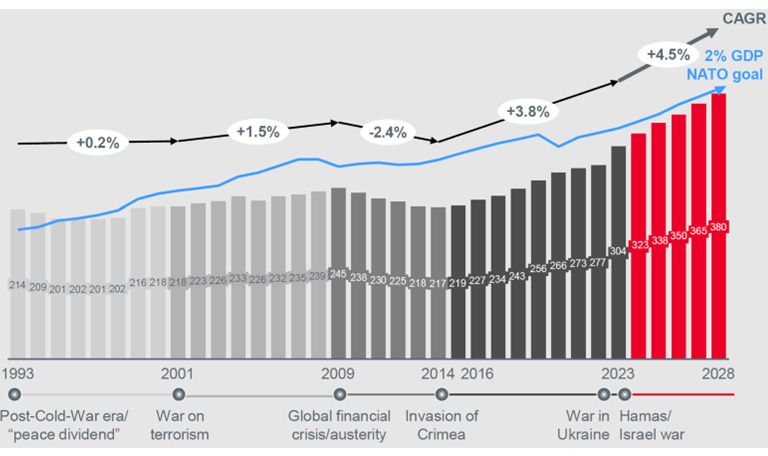

Europe's defense landscape has undergone a paradigm shift—a rearmament cycle unfolding at a velocity unseen since the Cold War. For three decades, the prevailing narrative was defined by the so-called "peace dividend," a period of underinvestment in military capabilities as geopolitical risks were deemed manageable and budgets were redirected elsewhere.2 But that thesis has cracked. In 2022, military spending in Central and Western Europe surged to €345 billion—finally eclipsing the 1989 peak.3 This is not just a cyclical response to one war. It's a structural recalibration, driven by a geopolitical regime shift. Frontline states like Poland, Estonia and Finland are no longer debating whether to hit the North Atlantic Treaty Organization's (NATO's) 2% of gross domestic product (GDP) target—they're aiming for 3%–4% and building force postures accordingly.4 The market doesn't always recognize turning points until they're obvious, but in European defense, the inflection is already behind us.

When monetary policy makers start commenting on defense strategy, you know the priorities are shifting. European Central Bank official Olli Rehn has gone on record calling for EU-level funding initiatives for drone production and air defense systems, explicitly acknowledging that treaty-bound fiscal constraints may need to be softened.5 The logic is compelling: if monetary and fiscal tools were coordinated to fight a pandemic and sustain economic demand, why wouldn't they be deployed to ensure geopolitical sovereignty? Brussels, once a symbol of austerity discipline, is now being reimagined as the financial engine of joint European defense industrial policy. The language of economic stimulus is being replaced with that of deterrence, resiliency and kinetic readiness.6 That's not just political rhetoric—it's a reordering of priorities that investors cannot ignore.

The 2% GDP spending target—once aspirational, often missed—is quickly becoming a floor, not a ceiling. We're now seeing credible conversations, particularly in U.S.- and NATO-aligned think tanks, about the need for European countries to spend as much as 4%–5% of GDP if they are to deter both conventional and gray-zone threats in a multipolar world. The underlying logic? Defense inflation is real, platforms are more complex, the cost of deterrence is rising faster than the cost of confrontation, and peer adversaries aren't standing still. The compound annual growth rate (CAGR) of European defense spending, already tracking 4.5% from 2023–2028 based on current commitments, could accelerate further if joint procurement programs, industrial subsidies and public-private defense tech partnerships scale.7 For investors, that's not just a policy signal—it's a generational capital expenditure (capex) evolution unfolding in real time.

Source: Leonardo S.p.A. (2024). "Industrial Plan 2024–2028: Executive summary." € stands for euros. CAGR refers to compound annual growth rate. GDP stands for gross domestic product. NATO stands for the North Atlantic Treaty Organization. https://www.leonardo.com

Dassault Aviation: Stealth, Sovereignty and Systems Thinking

Dassault Aviation is not just a French aerospace champion—it is the architect of Europe's vision for independent airpower. Known globally for the Rafale, Dassault's real strategic significance lies in how it pushes the frontier of sovereignty-enabling technologies. Nowhere is this more evident than in its leadership of the nEUROn unmanned combat air vehicle (UCAV) program—a stealth demonstrator that predates many U.S. and Chinese efforts in the same domain.8 Developed alongside firms like Leonardo (then Alenia), Saab and EADS, nEUROn is more than a platform; it's a European answer to the question of 21st-century air dominance. Stealth shaping, autonomous mission execution and collaborative weapons integration are all baked into the DNA of the project.

Dassault is also deeply entangled in Europe's next-generation airpower initiative—GCAP (Global Combat Air Programme)—through its experience in the still-contentious FCAS (Future Combat Air System) partnership with Airbus and Indra.9 While political friction among France, Germany and Spain occasionally clouds the FCAS timeline, Dassault remains the indispensable systems integrator. Its decades-long ability to shepherd complex aircraft from blueprint to battlespace gives it a central role as European air forces rethink survivability, data fusion and combat cloud architectures. In the language of capital markets: few firms offer such asymmetric upside tied to geopolitical hardening and intra-European industrial sovereignty.

Even as the UCAV and sixth-generation fighter programs command headlines, Dassault's broader value lies in its end-to-end integration model—something that appeals to customers who want sovereign control over design, intellectual property (IP) and lifecycle. In an era when European nations are questioning the strategic cost of U.S. platform dependence, Dassault's business model is effectively a hedge against American primacy in the defense aerospace sector. Its potential revenue streams span from export Rafale contracts (India, United Arab Emirates (UAE), Egypt) to eventual scaled programs in high-autonomy drone swarms and AI-assisted pilot-vehicle teaming. This is not a legacy aerospace firm—it's a sovereign systems house in stealth mode.

Sometimes, it's helpful to see some of this in a picture, which we have in figure 2:

Source: "2024 Annual Report," Dassault Aviation, 3/4/25. https://www.dassault-aviation.com. M stands for meters. T stands for tons.

Leonardo SpA: Multi-Domain Depth Meets Modular European Relevance

Leonardo SpA is arguably the most underappreciated systems integrator in the European defense ecosystem. Born from a national champion mentality but evolving into a multi-domain industrial platform, Leonardo is touching every layer of Europe's strategic autonomy stack—from air and cyber to space and EW (electronic warfare). Its industrial plan for 2024–2028 signals a clear transformation: digitalized manufacturing, platform rationalization and targeted global alliances are converging into a streamlined—but diversified—machine. The company isn't just participating in programs like Global Combat Air Programme and Eurofighter Typhoon; it's helping define the standards and enabling architectures across platforms.10

In the UAV space, Leonardo complements Dassault's stealth-first focus with operational versatility. Its Falco series has long been deployed in surveillance missions across NATO and UN theaters, and its ongoing development of heavier, more autonomous variants suggests a clear path toward expanded mission profiles, including target acquisition and ISR11-strike integration. Meanwhile, Leonardo's role in Proteus and other rotary-wing UAV projects underscores its ambition to define the European approach to unmanned vertical lift.12 And while it isn't a small-drone manufacturer, that's a feature, not a bug—Leonardo is building into the higher-value layers of the UAV stack: secure communications, command-and-control and layered counter-drone capabilities.

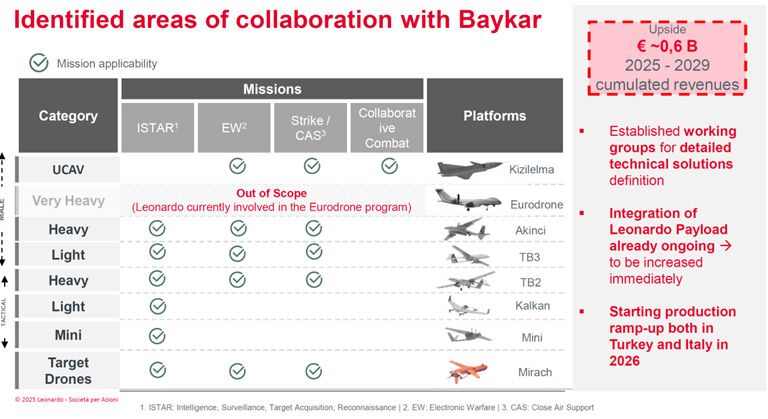

Figure 3 draws out Leonardo's emerging collaboration with Baykar—Turkey's leading UAV manufacturer, and it is a strategically important extension of its unmanned systems strategy, particularly as European defense shifts from platform independence to interoperable coalition capabilities. The partnership spans a wide range of drone categories—from heavy MALE (Medium Altitude Long Endurance) systems like the Akıncı and Tactical Block (TB2) to mini and tactical drones like the Kalkan and Mirach—and covers critical mission domains including ISTAR,13 electronic warfare and close air support. While Leonardo is currently committed to the Eurodrone program and thus excluded from the "very heavy" segment, its payloads are already being integrated into Baykar platforms, with technical working groups established to define deeper joint solutions. The joint production ramp-up planned for 2026 across both Turkey and Italy underscores the seriousness of this industrial axis, with €0.6 billion in cumulative revenue projected through 2029.14 Beyond revenue, the real upside is strategic: this partnership extends Leonardo's sensor, electronic warfare and payload integration footprint into one of the most battle-tested UAV families globally, while offering NATO-aligned modularity across future drone fleets.

Source: "Annual Shareholder Meeting 2025: Industrial Plan Update 2025–2029," Leonardo S.p.A., 5/6/25. https://www.leonardo.com

Perhaps Leonardo's most strategically leveraged position lies in counter-UAV systems—where it's investing in radar, laser and EW-based neutralization tech. In a post-Ukraine defense environment, where drones are cheap and ubiquitous, the demand for effective counter-drone solutions is set to outstrip even the UAV boom itself. Leonardo's electronics division, with its heritage in airborne and naval radar, is pivoting naturally into this space. Add to this its cyber and space segment growth—areas reinforced by joint ventures like Telespazio—and Leonardo increasingly looks like the glue holding together Europe's fragmented but fast-evolving defense tech map. It is a horizontal enabler of vertical sovereignty—and investors should not underestimate that role.

Europe is not just rearming—it is reindustrializing for deterrence, redefining fiscal priorities and accelerating a sovereign defense ecosystem built for a multipolar era. From Dassault's leadership in stealth and next-gen combat systems to Leonardo's multi-domain integration and drone-era adaptability, the continent is executing an ambitious, multi-decade capital expenditure cycle rooted in strategic autonomy.

For U.S. investors, this shift presents an underappreciated opportunity: participation in Europe's defense renaissance through publicly listed, high-conviction companies at the heart of this transformation. The WisdomTree Europe Defense Fund (WDEF), which is tracking the returns of the WisdomTree Europe Defense Index, is a strategy uniquely designed for this moment. It offers targeted exposure to European defense and aerospace innovators—not just headline contractors, but the critical enablers of next-gen platforms, cyber resiliency, secure communications and unmanned systems.

In a world where industrial policy, defense posture and market opportunity are converging, WDEF is a timely bridge between macro-level geopolitics and portfolio-level precision. As European defense spending structurally resets, the real question is no longer whether this transformation will happen—but how to allocate capital to it. WDEF answers that question with a thematic framework and investment precision built for this new arsenal economy.

Source: WisdomTree, with data as of the market's open on 7/17/25, the first day of trading for WDEF. Subject to change.

1 UAV stands for "Unmanned Aerial Vehicle"

2 Source: "The costly end of Europe's ‘peace dividend'," Financial Times, 3/17/25.

3 Source: "Trends in world military expenditure, 2022," Stockholm International Peace Research Institute, 4/24/23.

4 Source: G. Szakacs and K. Badohal, "Poland leads NATO on defence spend—but can it afford it?" Reuters, 10/22/24.

5 Source: "ECB's Rehn calls for joint European investment in air defence, drones," Reuters, 3/11/25.

6 Source: "Brussels to exempt defence spending from EU budget constraints," Reuters, 2/14/25.

7 Source: "EMEA defence contractors boosted by increased govt spending," Fitch Ratings, 3/27/24.

8 Source: "nEUROn: Unmanned combat air vehicle demonstrator," Dassault Aviation (n.d.),

9 Source: Airbus CEO Michel Schoellhorn (via Financial Times), "Airbus CEO suggests merging Europe's fighter jet programmes," Reuters, 1/15/25.

10 Source: "Global Combat Air Programme — Developing the future of combat air," Leonardo S.p.A., 6/1/24.

11 ISR stands for intelligence, surveillance and reconnaissance.

12 Source: "Leonardo unveils design of Proteus uncrewed rotorcraft technology demonstrator," Leonardo UK, 1/7/25.

13 ISTAR stands for intelligence, surveillance, target acquisition and reconnaissance.

14 Source: T. Kington, "Leonardo predicts massive revenue leap to €32.5 billion by 2029" [industry report], Defense News, 3/11/25.

There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. This Fund focuses its investments in Europe, thereby increasing the impact of events and developments in Europe that can adversely affect performance. Europe has and may continue to experience security concerns, war, threats of war, aggression and/or conflict, terrorism, economic uncertainty, sanctions or the threat of sanctions, natural and environmental disasters, the spread of infectious illness, widespread disease or other public health issues and/or systemic market dislocations that lead to increased short-term market volatility and have adverse long-term effects on European and world economies and disrupt the orderly functioning of securities markets generally, which may negatively impact the Fund’s investments. Many countries within Europe are closely connected, and their economies and markets are largely interdependent. As such, economic and political events in one European country, including monetary exchange rates between European countries and armed conflicts among two or more European countries, may have adverse effects across Europe. European countries that are members of the European Union (“EU”) and the European Economic and Monetary Union (“EMU”) are subject to certain economic and monetary policies and controls and the risks associated with such coordinated economic and fiscal policies. Because the Fund invests primarily in the securities of companies in Europe, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Europe and to be more volatile than the performance of more geographically diversified funds. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger-capitalization stocks or the stock market as a whole. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Europe Defense Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.