EPI

India Earnings Fund

Published August 22, 2025

Global Head of Research

The Indian equity market in 2025 hasn't quite captured headlines like China's tactical rebound or the broader emerging markets resurgence. On a relative basis, India looks like it's taking a breather. But under the surface, it's anything but stagnant. From a fundamental investor's lens, this is precisely when narratives get dislocated from reality—and when forward-looking capital should be sharpening its focus.

Think of what's happening as a shift, not a stall. The National Stock Exchange Fifty Index is up roughly 3% year-to-date, a modest showing in comparison to benchmarks like the MSCI Emerging Markets Index, up closer to 20% over the same period.1 This isn't a time to lose confidence in the India story—it's a time to adjust expectations with the long-term in mind. Beneath the index-level quiet, capital markets are alive. India is pacing toward a record IPO year, with more than $6.7 billion raised so far—surpassing even the same period last year. Domestic appetite is deep, and post-IPO performance has been encouraging.2 This isn't speculative froth; it's institutionalization in motion.

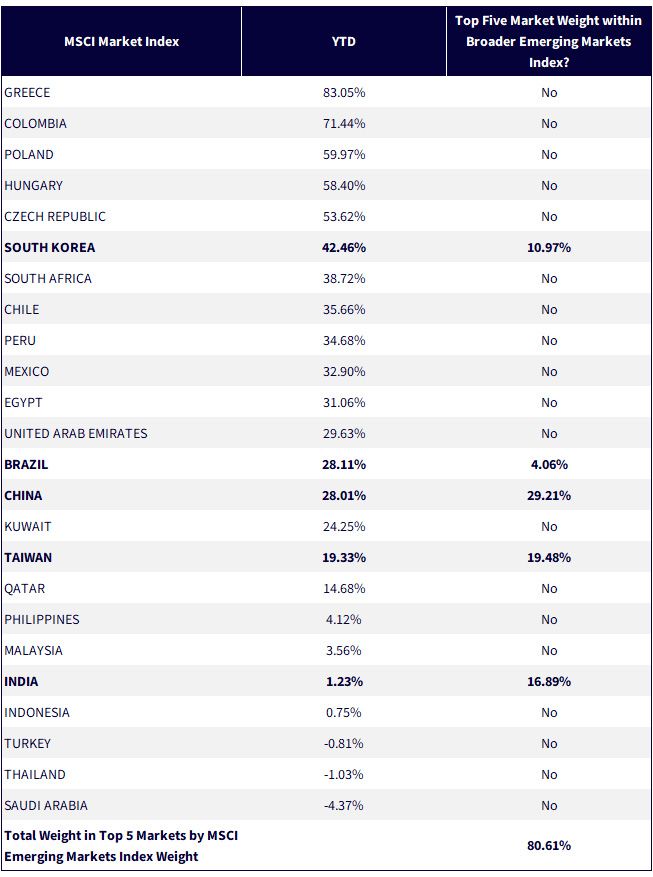

Looking to figure 1:

Figure 1: The Disconnect: 2025's Top EM Performers Hold Little Index Weight

Source: MSCI. Performance is YTD 2025, through 8/18/25. Weight is as of 7/31/25. Any market labeled "no" has a weight less than 4.06%, Brazil's weight as the fifth-largest market exposure in the Index. Bold type notes weight within the top five market exposures of the MSCI Emerging Markets Index as of 7/31/25. Subject to change.

India's Household Balance Sheets Are Evolving—Fast

There's a quiet revolution underway in how Indian households allocate capital. We talk often about the U.S. 401(k) moment—India is building its own version. With more than $42 billion in year-to-date domestic fund inflows dwarfing $8 billion in foreign outflows, the marginal buyer of Indian equities is no longer an offshore account manager in Singapore or London—it's a domestic retail investor with a growing systematic investment plan (SIP) account,3 tax incentives and mobile-first access to capital markets.4

This shift matters. It builds resilience. It creates a funding base that doesn't get spooked by short-term geopolitics or a bad U.S. consumer price index (CPI) print. And more importantly, it lays the foundation for long-term valuation support. Price-to-earnings (P/E) multiples across discretionary and retail sectors are running below historical averages—even with robust return on equity (ROE) and earnings growth outlooks.5

India's macro toolkit is hitting stride. A decade ago, CPI inflation and oil imports would have dictated the market's every move. Today, the Reserve Bank of India has defanged volatility through inflation targeting and policy credibility. The result? A smoother glidepath for interest rates and, by extension, market multiples. Fiscal prudence hasn't meant austerity—it's meant a redirection toward capex, infrastructure and productivity.

The next major shift is likely to come through Goods and Services Tax (GST) reform. Nearly a decade after its introduction, policy makers are preparing the system's next iteration—simplifying rate structures and reducing today's patchwork of slabs into a more streamlined two- or three-tier model. For companies, this means lower compliance costs, greater clarity in planning and a more predictable investment environment. For consumers, it translates into fewer distortions across categories and a smoother national marketplace.

Equally important is the rise of digital integration and enforcement. The government has been piloting real-time invoice matching, e-way bill harmonization and AI-driven fraud detection. These aren't just efficiency upgrades—they expand the formal economy, improve tax buoyancy without raising rates and strengthen the state's fiscal resilience.

2025 has been a reminder: market narratives often lag fundamentals. For patient capital, that's an opportunity, not a frustration. India is now contributing one-fifth of global working-age population growth and could account for a similar share of incremental global gross domestic product (GDP) by 2035.6 Markets may get temporarily distracted by what's happening in AI trade rotations or Chinese property rescue packages, but the underlying compounding in India is still happening—with increasing clarity.

The investment thesis here doesn't hinge on this quarter's PMI print or the timing of the next Fed cut. It hinges on a regime shift: from external dependence to internal strength, from volatility to durability and from promise to scale.

Conclusion: A Strategy More Aligned with India's Long-Term Equity Potential

Against this backdrop of temporary performance dislocation and index concentration, investors need to ask not just where they are invested in India—but how. The MSCI Emerging Markets Index remains heavily skewed toward mega-cap names and countries with large weightings but uneven fundamentals. Even within India itself, many index-linked strategies are top-heavy, overexposed to high-P/E growth narratives and reliant on a narrow group of market leaders. This leaves portfolios vulnerable to valuation shocks and style rotations. In contrast, India's real economic dynamism—especially in 2025—is increasingly powered by mid-sized firms across industrials, financials, consumer cyclicals and technology services, many of which are consistently profitable but underrepresented in capitalization-weighted benchmarks.

The WisdomTree India Earnings Fund (EPI) offers a structurally differentiated solution. Designed to track the total return performance of the WisdomTree India Earnings Index, the strategy deliberately screens for profitability, including only companies that generate positive earnings from core operations. This earnings-weighted methodology naturally tilts exposure away from speculative high-P/E names and allocates capital based on real business performance—not market cap alone. As a result, EPI has historically delivered a more balanced blend of large-, mid- and small-cap Indian equities, capturing the depth of India's economic base while mitigating valuation risk. In a year like 2025—where headline returns don't tell the full story—this approach becomes particularly powerful.

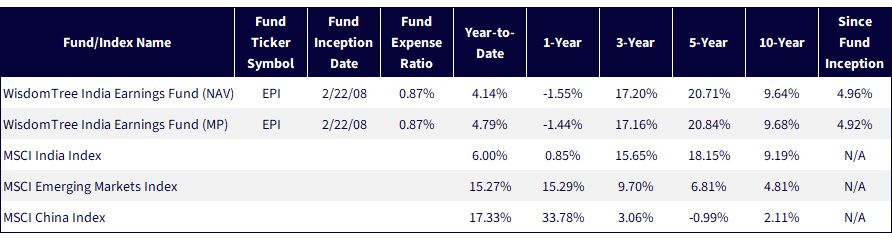

Figure 2: Standardized Performance

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/19/25, with returns as of 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click here.

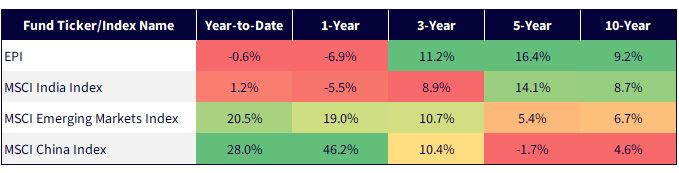

It's important to recognize that China is the single largest market within the MSCI Emerging Markets Index, accounting for more than 29% of the benchmark's weight. This dominant position means that even modest outperformance by Chinese equities can significantly influence the total return of the MSCI EM Index—especially when countries like India, with a nearly 17% weight, are appreciating at a slower pace. In 2025, we've seen precisely this dynamic at play: China has staged a tactical rebound from depressed levels, driven by a mix of policy support, improved investor sentiment and a bounce in select tech and consumer sectors.7 Meanwhile, India's performance, though solid in absolute terms, appears more muted in comparison. For investors benchmarking to MSCI EM, this can create a false sense of missed opportunity—as if India is falling behind, when in fact, the composition of the benchmark is doing much of the performance lifting.

But that short-term framing misses the deeper, more durable trend. As is visible in figure 3, over a 3-, 5- and 10-year horizon, India has consistently outperformed China on both equity returns and earnings growth metrics. India's structural drivers—demographics, macro stability, domestic consumption and a reform-oriented policy regime—have created a fertile environment for long-term capital compounding. In contrast, China faces persistent headwinds from demographic decline, real estate overhangs and a slower transition to consumption-led growth. So, while China may look like the performance leader in select quarters or even years, it has done so from a lower base and with greater volatility. For investors focused on sustained exposure to emerging market growth, India's long-term leadership remains the more resilient,especially when paired with strategies that move beyond simple market-cap exposure.

Figure 3: India's Near-Term Underperformance andLonger-Term Outperformance

Sources: WisdomTree, MSCI, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 8/19/25, with returns as of 8/18/25. NAV denotes total return performance at net asset value. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click here.

If Prime Minister Modi is successful at creating potentially positive catalysts, like GST reforms, as one example, it could unlock what we view as the underlying strength of India's market—a strength that we have not really seen for much of 2025.

1 Source: FactSet, with year-to-date measured through 8/18/25.

2 Source: M. Mishra, "India on track for record IPO year as equity market booms," Financial Times, 7/10/25.

3 A systematic investment plan is a method or mechanism for investing in mutual funds—specifically designed for retail investors to contribute fixed amounts at regular intervals (e.g., monthly or quarterly) into selected mutual fund schemes.

4 Source: Mishra, 2025.

5 Source: A. Menon, S. Rathi, S. Vohra and G. Varma, "India Consumer Discretionary" [investor presentation], Morgan Stanley India Company Private Limited, 7/17/25.

6 Source: Desai & Parekh, 2025

7 Source: W. Sandlund and C. Kay, "Chinese equities rebound on policy boost and tech recovery," Financial Times, 7/8/25.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region that can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. As this Fund has a high concentration in some sectors, the Fund can be adversely affected by changes in those sectors. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

India Earnings Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.