DHS

U.S. High Dividend Fund

Published April 16, 2025

Global Head of Research

At WisdomTree, our journey began in 2006 with a foundational belief: that dividends matter. The market regime following the global financial crisis1 often rewarded high-growth, non-dividend-paying companies—particularly in the U.S. Technology, Consumer Discretionary and Communication Services sectors. A core tenet of portfolio construction became easy to ignore: the importance of defense.

For much of the past two decades, dividend strategies were overshadowed by the rise of mega-cap growth. But there's a principle in investing—defense can appear as annoying underperformance…until you need it. In 2025, with rising volatility and a difficult-to-predict Trump Administration, there is a growing market rotation away from the Magnificent 7,2 and dividend-paying companies have come back in focus.

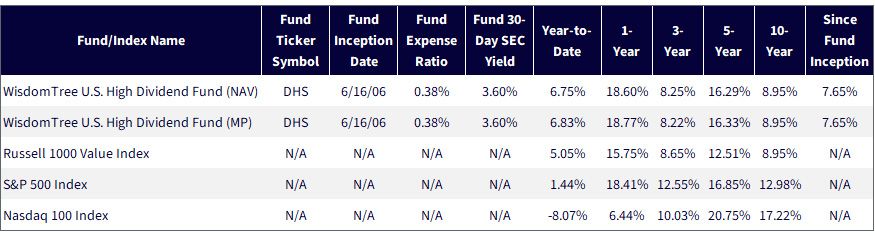

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 3/31/25. Fund 30-Day SEC Yield as of 3/31/25. 30-Day SEC Yield = The yield figure reflects the dividends and interest earned during the period, after deduction of the Fund’s expenses. This is also referred to as the “standardized yield". NAV denotes total return performance at net asset value. MP denotes market price performance. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For DHS's most recent month-end and standardized performance, click here. Performance of less than one year is not annualized.

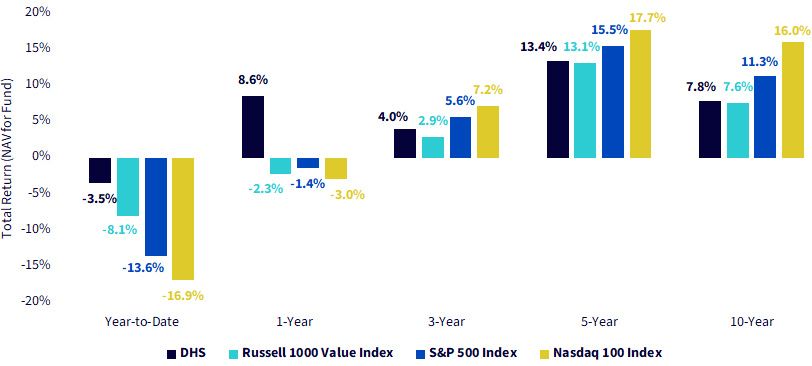

So far, 2025 has been a rough ride—and in a year where everything feels a bit painful return-wise, the WisdomTree U.S. High Dividend Fund (DHS) has been less painful. Down −3.5% year-to-date (YTD), it's held up meaningfully better than the Russell 1000 Value Index (−8.1%) and especially the S&P 500 (−13.6%). The Nasdaq 100 Index has been the leader for some time, emphasizing exposure to the mega-cap technology-oriented companies we mentioned earlier, and it is down 16.9% over this YTD period. When the market starts to question the price it pays for forward-looking expectations, cash in hand—in the form of dividends—suddenly looks like a more favorable deal.

Zoom out to the one-year view, and DHS has maintained its prominence. While broad value and the S&P 500 still reflect losses (−2.3% and −1.4%, respectively), DHS is up 8.6%. Again, the Nasdaq 100 Index faced the toughest result, down 3.0%. That's not a fluke. It's a signal. Market leadership is starting to rotate, and strategies that favor durability over disruption are gaining ground.

But move further out—three, five and 10 years—and the gravitational pull of megacap tech becomes unavoidable. The S&P 500, supercharged by a handful of dominant growth stocks, lapped both dividend and value benchmarks, and the Nasdaq 100 Index did even better. It's a reminder that in certain regimes, concentration can look like genius…until it doesn't.

In our opinion, the point isn't that dividends always win. It's that they show up when you need them most—and they do so without requiring you to bet the farm on what's next in AI, semiconductors or space colonization.

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 4/7/25. NAV denotes total return performance at net asset value. MP denotes market price performance. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For DHS's most recent month-end and standardized performance, click here. Performance of less than one year is not annualized.

Sometimes the standard periods of multiple years can mask the experience that many of us might remember during individual years. For example:

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. You cannot invest directly in an index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For DHS's most recent month-end and standardized performance, click here.

What You Don't Own Matters Just as Much as What You Do

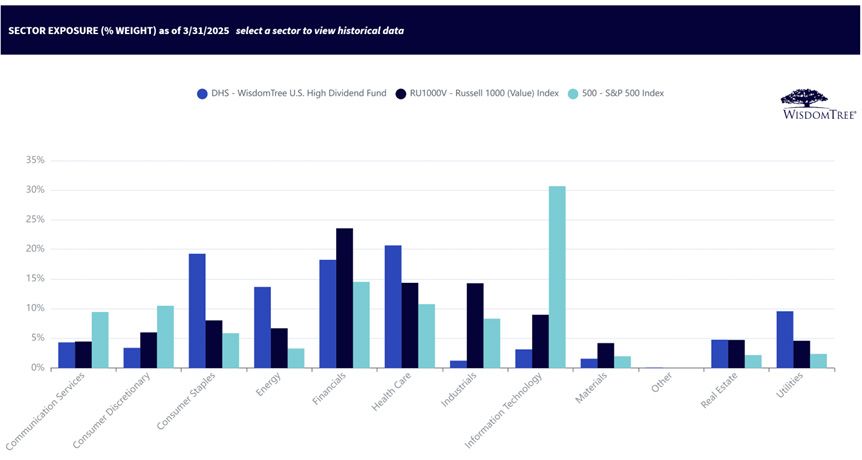

One look at figure 4 and the story becomes obvious: DHS is not trying to be everything to everyone. It's deliberately not chasing tech. While the S&P 500 leans hard into Information Technology (north of 30% exposure), DHS sits comfortably with single-digit weight. That's not an accident—it's the product of a strategy that asks a different question: "Who's paying shareholders today?" rather than "Who's growing the fastest?"

That sector tilt—away from the frothy and toward the fundamental—defines the defensive DNA of DHS. It's right there in the over-weight allocations to Consumer Staples, Utilities, Energy and Health Care. These aren't the sectors that dominate headlines, but they do tend to hold up when the headlines turn sour.

Financials and Energy together account for over 30% of DHS—two sectors that, while cyclical, also represent valuation discipline and free cash flow. These are businesses that have had to prove themselves in high-rate environments. And in a world where capital is no longer free, that starts to matter again.

The under-weight to Information Technology, and to a lesser extent to Communication Services, has felt like a liability in the growth-dominated years. But in 2025, it's looking more like a cushion.

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 3/31/25. The Nasdaq 100 Index holdings and sector exposures are not accessible in this system. You cannot invest directly in an index. Exposures are subject to change.

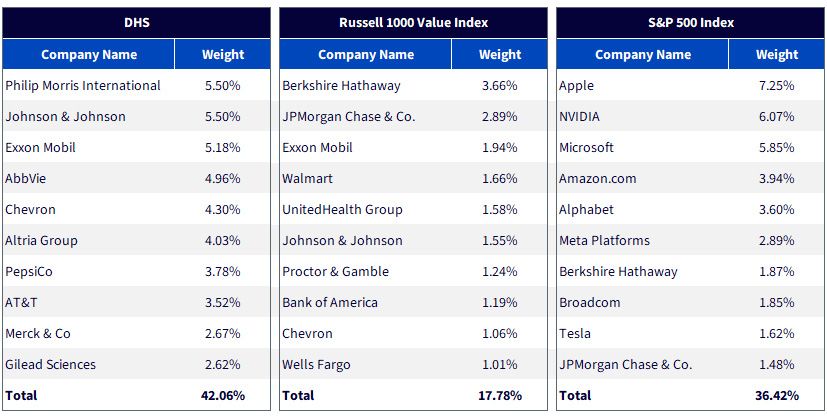

Look at DHS's top holdings. There's no Apple. No NVIDIA. No Microsoft. No Alphabet, Amazon, Meta or Tesla. In fact, the total exposure to the Magnificent 7 is zero. This is a portfolio that has deliberately not owned the market's most talked-about—and most concentrated—drivers of return over the past five years.

Names like Philip Morris, Johnson & Johnson, Exxon Mobil and AbbVie—these are household names, yes, but also steady compounders with strong balance sheets and consistent dividend policies. In fact, the top 10 names in DHS account for over 42% of the portfolio, and every one of them pays you to own them.

Contrast that with the S&P 500, where more than a third of the index is concentrated in just 10 companies—seven of which are tech-driven giants. That's a bet on continued dominance by a handful of firms that have already defied gravity for a decade.

The Russell 1000 Value Index may be Value, but its top holdings do overlap with those of the S&P 500 Index and total only about 18% of the portfolio.

DHS expresses something different: intentional concentration in income-generating companies. It's not designed to beat the S&P 500 Index in momentum-driven bull markets. It's designed to act like ballast when the future starts to feel uncertain.

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 3/31/25. The Nasdaq 100 Index holdings and sector exposures are not accessible in this system. You cannot invest directly in an index. Holdings subject to change.

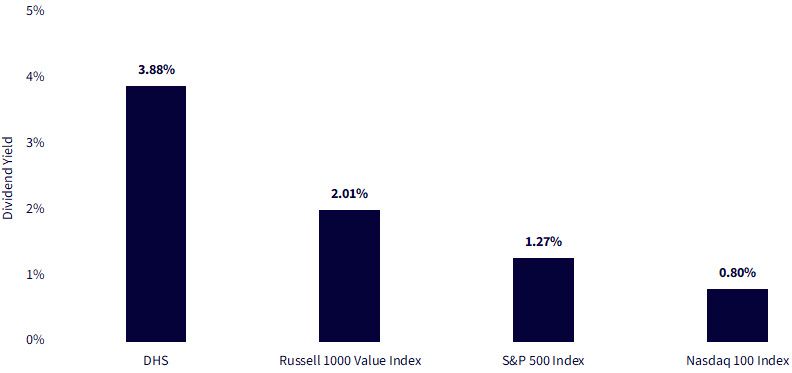

DHS offers a 3.88% dividend yield3—nearly double the Russell 1000 Value Index and more than triple the S&P 500. That's not a rounding error. That's a fundamentally different approach to equity investing.

Where most portfolios today are implicitly betting on multiple expansion, DHS delivers a return stream that doesn't require perfect timing or endless growth. It pays you to be patient. It pays you through the volatility.

Importantly, this isn't yield for yield's sake. These are not distressed businesses with unsustainable payout ratios. DHS is built from the ground up and seeks to mitigate the risk of exposure to value traps and companies paying unsustainable dividends. The highest weight is not in companies with the highest yields but rather in those companies that are distributing the most cash in aggregate to their shareholders.

In a world where cash once again has a cost and equity markets are repricing risk, income is strategy—not just an outcome.

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 3/31/25. You cannot invest directly in an index.

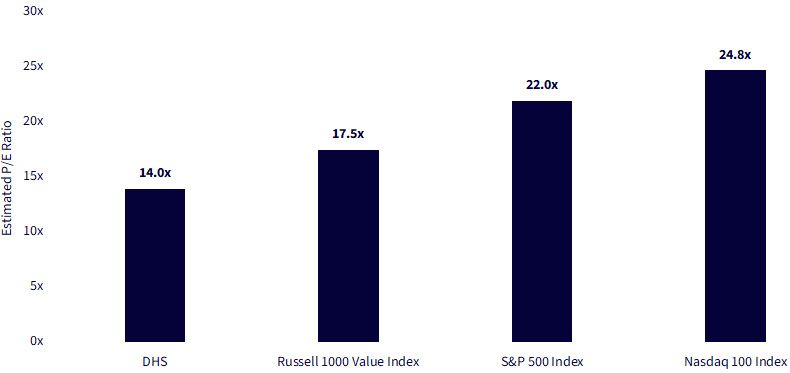

With the S&P 500 trading at 22 times forward earnings, investors are once again leaning heavily on the idea that growth will justify the price. The Nasdaq 100 Index saw an even higher valuation. The Russell 1000 Value Index is more modest, but still sits at 17.5 times. Neither feels particularly cheap by historical standards, especially with real rates now positive and capital no longer free.

Then there's DHS—clocking in at just 14.0 times.

That number isn't just lower; it's anchored in a portfolio of dividend payers with high return-on-equity metrics and a strict valuation discipline at the time of rebalancing. It reflects a different logic: don't pay up for potential, pay less for profitability that already exists.

In an era where multiple expansion may be limited, we believe starting valuation matters more than ever.

Sources: WisdomTree, Morningstar and FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, as of 3/31/25. You cannot invest directly in an index.

For much of the last decade, being under-weight in tech or over-weight in dividends felt like a drag—an anchor in a market that rewarded speed over stability, potential over profit. But in 2025, the narrative is shifting, and DHS is meeting the moment.

In a market defined by extreme concentration, extended valuations and rising macroeconomic uncertainty, DHS offers something refreshingly scarce: balance. It is a portfolio built not on dreams of disruption but on durable cash flows, capital return and valuation discipline. The Fund has delivered strong relative performance in a tough environment, and its sector and stock positioning shows a clear intentionality: real businesses, paying real income, at reasonable prices.

Where others are asking, "How much longer can the Magnificent 7 lead?", DHS has already moved on.

1 The global financial crisis played out in global markets during portions of 2008 and 2009. After this period, interest rates across much of the developed world were at or near record lows for extended periods, an environment that was very favorable for growth-oriented equities.

2 Refers to Apple, Amazon.com, Alphabet, Microsoft, Meta Platforms, Nvidia and Tesla.

3 As of 4/15/25, DHS's SEC 30-day Yield = 3.94%. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For DHS’s prospectus, click here. For DHS’s most recent month-end and standardized performance, click here.

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. High Dividend Fund

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.