The Rhythm of Style: Value vs. Growth in Developed International Markets—Part 2

Published April 10, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- So far this year, the WisdomTree International High Dividend Fund (DTH) has delivered relative outperformance in a market environment that has become challenging in light of Trump Administration Tariff discussions.

- Despite offering a lower yield, the WisdomTree International Quality Dividend Growth Fund (IQDG) continues to seek superior profitability and earnings growth potential, reinforcing its long-term appeal to investors focused on quality and compounding.

- The stark sector differences between DTH and IQDG, especially in Financials and Information Technology, underscore the importance of understanding what’s driving returns beneath the surface and how to consider broad-based international exposures in the current environment.

Dividends: Quality-Growth or High-Yielding?

WisdomTree has been managing a suite of developed international dividend-oriented equity strategies for a long time. Similar to how the MSCI EAFE Growth and MSCI EAFE Value Indexes move in different regimes, dividend-oriented strategies can be aligned toward "quality-growth" and "higher-yielding" orientations that can behave similarly:

- WisdomTree International Quality Dividend Growth Fund (IQDG): This strategy is designed to track, before fees and expenses, the total return performance of the WisdomTree International Quality Dividend Growth Index. The focus is on equities within developed international markets that have strong earnings growth and quality characteristics, weighted on the basis of cash dividends paid.

IQDG exemplifies what we think of as the "quality-growth" dividend payers in developed international stocks.

- WisdomTree International High Dividend Fund (DTH): This strategy is designed to track, before fees and expenses, the total return performance of the WisdomTree International High Dividend Index. The focus is on relatively higher-yielding dividend payers across developed international markets, weighted on the basis of cash dividends paid.

DTH exemplifies what we think of as "higher-yielding" dividend payers in developed international markets.

We can compare these strategies to the MSCI EAFE Index benchmark.

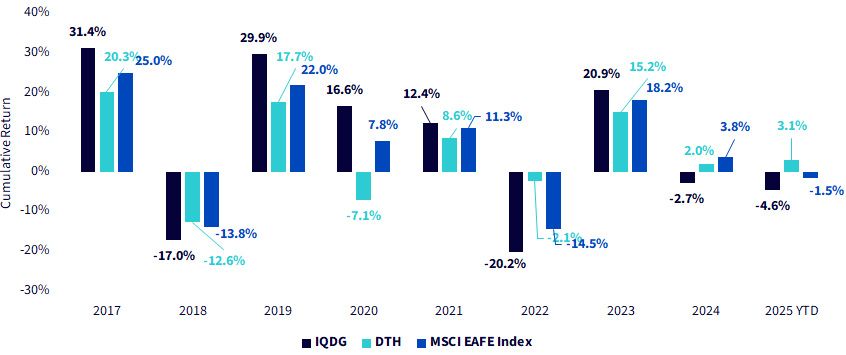

Every Year Can Look Quite Different, Performance-Wise

While it would be simpler if a single strategy always outperformed, the reality is that none of these strategies always underperformed or always outperformed on a calendar year basis.

- IQDG looked particularly strong in 2017, 2019, 2020 and 2023. From a relative performance perspective, 2020 was a complete blowout year for this strategy. In fairness, IQDG had a tougher 2018, 2022 and 2024 relative to the others.

- Our initial expectation of DTH would be for the most defensively oriented construction, meaning that it could lag in up markets (true in 2017, 2019, 2021 and 2023) and outperform in rougher markets (not true in 2020, but true in 2022). 2025 YTD has seen DTH delivering relative outperformance, signifying that “value” and “defensive” types of allocations may be particularly in favor.

Figure 1: What a Difference a Year Can Make

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with returns for the 2025 YTD period as of 4/8/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: DTH, IQDG.

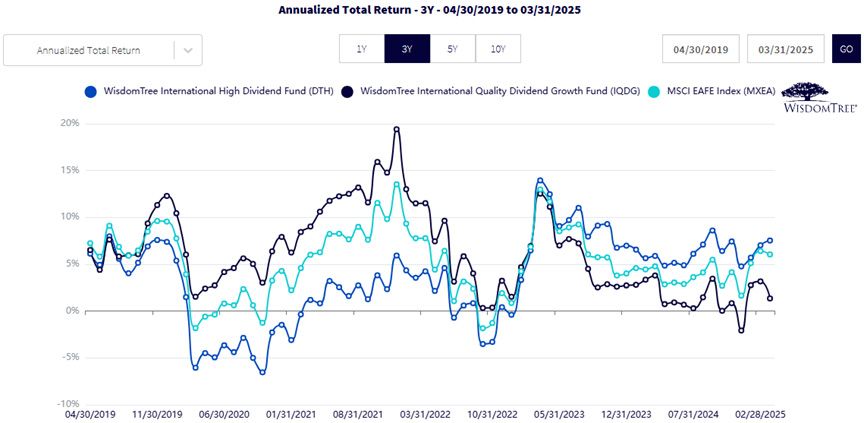

A Shift from Quality Dividends to High Dividends

The rolling three-year returns paint an interesting picture:

- Over the beginning of the available history, IQDG was the top performer, whereas DTH was the bottom.

- As the period shifted from 2022 to 2023, the script flipped, and DTH became the leader and IQDG the laggard.

Figure 2: Quality Dividends vs. High Dividends over Time—Rolling Three-Year Annualized Returns

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with returns, calculated monthly, as of 3/31/25. NAV denotes total return performance at net asset value. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: DTH, IQDG.

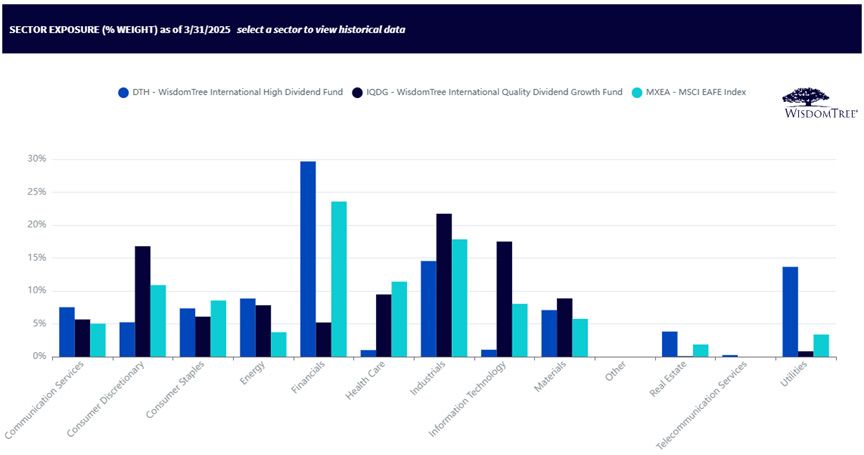

High Dividends for Defensive and Value-Oriented Exposures

Did you realize that you could have two dividend-focused strategies focused on developed international equities that differ in their exposure to Financials by 25%? This is the case for DTH (30% Financials) and IQDG (roughly 5% Financials). When we see periods of differentiated performance, this is obviously the first stone that should be overturned.

Financials as strong performers in developed international equities is a primary factor explaining DTH's stronger start to 2025 and relative outperformance so far in a tougher market environment.

It's also interesting to see that IQDG gets close to 20% exposure to Information Technology, whereas DTH is closer to 0% than it is to 5% exposure. Developed international markets do not have as large tech companies as is the case in the U.S. market.

Figure 3: High Dividends and Quality Dividends Have a Massive Degree of Sector Dispersion

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with sector exposure data as of 3/31/25. Subject to change.

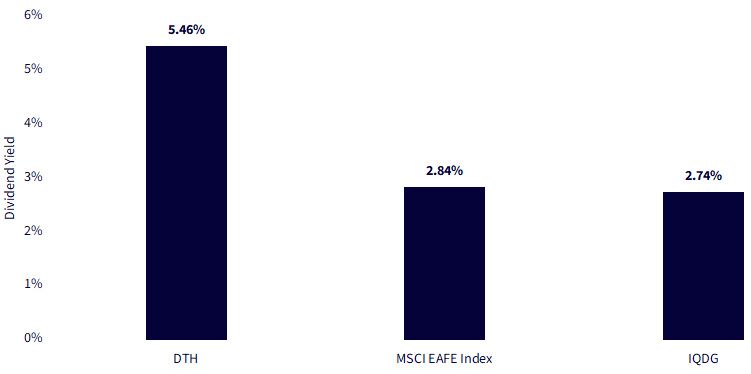

Dividend Yield: DTH Leads, But at What Cost?

The first chart is a yield chaser's dream. DTH boasts a 5.46% dividend yield, significantly above the MSCI EAFE Index (2.84%) and IQDG (2.74%). At first glance, this positions DTH as a go-to vehicle for income-seeking investors.

However, this superior yield may mask hidden trade-offs. High yields often reflect concentrations in slower-growth, lower-multiple, more cyclical sectors like Financials, Utilities or Telecoms. As we'll see, this plays out across other metrics.

Takeaway: DTH wins on yield, but the full picture requires looking deeper.

Figure 4: A Comparison of Dividend Yields

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with trailing 12-month dividend yield as of 3/31/25. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: DTH, IQDG.

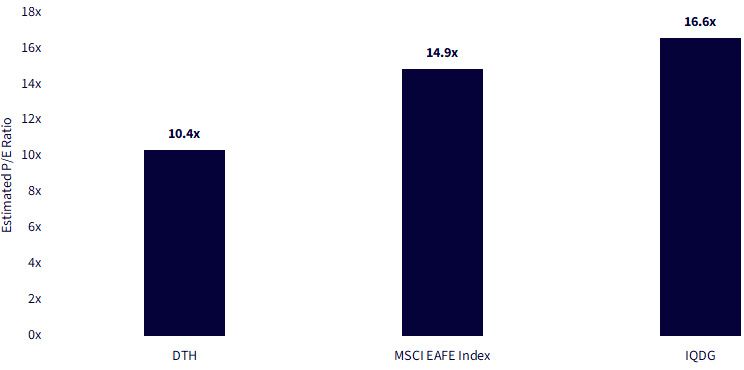

Valuation: Lower Multiples, Lower Growth?

On valuation, DTH again stands out—this time for its low price-to-earnings ratio (10.4x), a potential draw for value-oriented investors. The EAFE Index and IQDG are meaningfully richer at 14.9x and 16.6x, respectively.

IQDG's high multiple aligns with its emphasis on quality factors—companies with consistent earnings, strong balance sheets and capital discipline. These attributes command premium valuations, but they are often justified by long-term compounding potential.

Takeaway: DTH offers cheap exposure. IQDG, while pricier, may be paying up for durability and growth.

Figure 5: A Comparison of Estimated P/E Ratios

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with estimated P/E ratio as of 3/31/25.

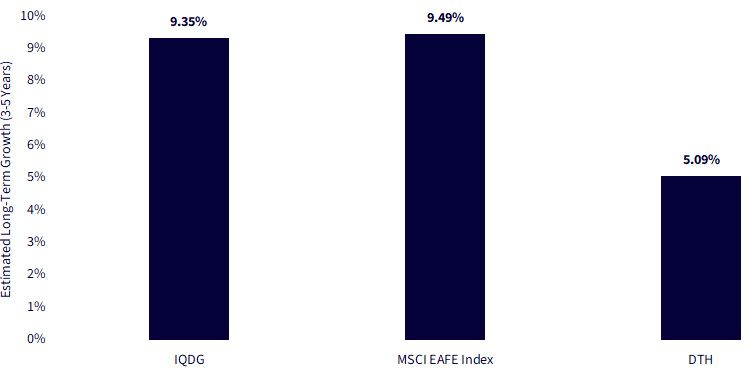

Growth: IQDG as the Compounder's Choice

Growth expectations flip the script. IQDG delivers 9.35% estimated long-term earnings growth, while the EAFE benchmark delivered 9.49% and DTH trailed with 5.09%.

This reinforces the narrative: DTH is built for yield today; IQDG is built for growth tomorrow.

Takeaway:IQDG appears to offer the best shot at compounding earnings power, while DTH prioritizes income now over growth later.

Figure 6: A Comparison of Forward-Looking Earnings Growth Estimates

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with estimated long-term earnings growth (3–5 years) as of 3/31/25.

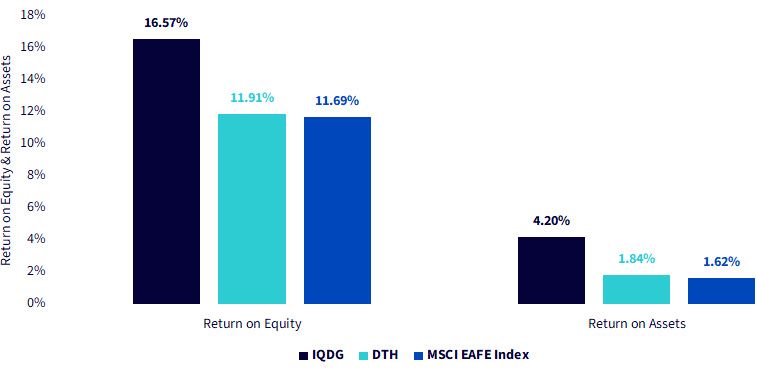

Profitability: Quality Dominates

The final chart drives home the quality premium. IQDG companies deliver a return on equity (ROE) of 16.57% and a return on assets (ROA) of 4.20%—far superior to peers. DTH and the MSCI EAFE Index cluster around 11.5% to 12% ROE and 1.6%–1.9% ROA.

This is a critical distinction. High profitability often signals pricing power, operational efficiency and resilience during downturns—all foundational to consistent dividend payments.

Takeaway: IQDG's profitability metrics support its quality tilt and may justify the valuation premium.

Figure 7: A Comparison of Quality Metrics

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 4/9/25, with return on equity and return on assets as of 3/31/25.

Conclusion: Value Has Been Outperforming, But Need to Understand the Trade-Offs

Hopefully, the details of this piece help investors see the underlying rationale as to why we may see a lot of attention on the outperformance of value-oriented strategies beyond U.S. borders as we start 2025. The heavy exposure to Financials is a very important consideration. Over the longer term and depending on individual outlooks, there are cases where quality and growth may prove a better fit.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Funds' prospectus for specific details regarding the Funds' risk profile.

DTH: Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility.

IQDG: Heightened sector exposure increases the Fund’s vulnerability to any single economic, regulatory or other development impacting that sector. This may result in greater share price volatility. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs.

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.