India’s Growth Story: Opportunities Rising amid Global and Domestic Challenges

Published February 13, 2025

Global Head of Research

Key Takeaways

- India’s rapid digitalization and youthful population position it for long-term economic expansion, with its internet economy projected to reach $1 trillion by 2030.

- Despite macroeconomic challenges like capital outflows and regulatory hurdles, India’s manufacturing push, digital payments growth and rising middle class continue to drive investment opportunities.

- The WisdomTree India Earnings Fund (EPI) offers a valuation-conscious approach to India’s premium equity market, leveraging earnings-weighted indexing to mitigate valuation risks.

India, the world's fifth-largest economy, stands at a pivotal moment. With a population of more than 1.4 billion—65% of whom are under the age of 35—the nation boasts one of the youngest demographics globally,1 a powerhouse for innovation and productivity. India is in its "Digital Decade," with the country on a path to reach a $1 trillion internet economy by 2030.2 Simultaneously, India's digital ecosystem is rewriting the rules of engagement: Internet penetration has leapt from 20% in 2015 to more than 60% in 2023, connecting more than 900 million people.3 Digital payments through platforms like UPI, which processed more than 15 billion transactions per month through November 2024,4 exemplify this transformative shift. Yet, alongside these strengths lie challenges—structural inefficiencies, job creation hurdles and global economic pressures—that complicate India's growth narrative. This article weaves through the problems and solutions, unpacking India's complex economic potential.

The Debate: India's Growth and Equity Markets

India's economic engine has recently encountered significant resistance. Real GDP growth has averaged more than 6% since 2000, on the back of a large and expanding services sector. This growth has lifted an estimated 415 million people out of multidimensional poverty since 2005. At the same time, manufacturing sector growth has remained sluggish, and more than half of all workers remain in low productivity jobs in agriculture, construction and trade.5 Average deposit growth for rated banks of 11%–13% remains lower than credit growth of 15%–17%. This has led to a rise in loan-to-deposit ratios (LDR) compared with levels at the end of March 2023.6 Meanwhile, foreign direct investment (FDI) inflows hover around $70 billion annually.7

Take the Goods and Services Tax (GST) system, intended to simplify taxation but often criticized for its complexity and frequent rule changes. These bureaucratic hurdles, paired with unpredictable regulatory shifts, leave investors cautious. For example, industrial clusters in sectors like electronics and auto components struggle to attract consistent foreign capital despite their potential.

But even as these challenges mount, India's demographic and consumption strengths shine through.

If we consider India's middle class, it's important to define the term:8

- Spending US$2–US$10 per capita per day: more than 600 million people

- Approximately US$17–US$100: 432 million Indians

Programs like "Make in India" are designed to capitalize on this momentum, encouraging investments in sectors such as manufacturing and renewable energy. For instance, Apple's decision to manufacture iPhones in India demonstrates the growing trust global corporations place in the nation's industrial capabilities.9

Job Creation: A Demographic Balancing Act

Around 270 million people are expected to join India's workforce by 2040.10 Infosys and Wipro collectively hire tens of thousands of engineers and support staff every year, while the organized retail and logistics sectors drive job growth in warehousing and customer service.

Yet, more than 90% of India's workforce remains employed informally,11 often in low-productivity roles such as small-scale farming or street vending. Consider the rural worker in Bihar, whose seasonal livelihood is worlds apart from the high-skill, high-wage roles emerging in cities like Bengaluru. This disparity underscores the need for transformative interventions.

Digitalization offers a compelling answer. In December 2024, Unified Payments Interface (UPI) transactions saw a record 8% month-over-month growth, with 16.73 billion transactions worth roughly $272 billion. For the year, UPI saw 172 billion total transactions, worth $2.88 trillion.12 This exemplifies how digital ecosystems can integrate informal economies into formal frameworks. Capital markets are also evolving, with IPO activity and private equity funding driving entrepreneurship and job creation.

Headwinds for Equity Investors in Early 2025

External forces, particularly rising U.S. Treasury yields, have introduced new complexities for India. Higher returns in developed markets draw capital away from emerging economies like India's. Global investors have withdrawn $6 billion this month, leading to the worst start for the NSE Nifty 500 Index in nine years. Domestic institutions and retail investors remained buyers, with net purchases of $8 billion, solidifying their role as market drivers.13

India's equity markets, though commanding a premium over other emerging markets, remain a beacon for long-term investors. Valuation concerns aside, sectoral growth stories are compelling. Technology remains a cornerstone, with TCS and Infosys leading the charge in IT services. The green energy sector is thriving, propelled by investments in solar and wind projects aligned with government sustainability targets. India's drug and pharmaceutical exports have increased from $2.13 billion in 2023 to $2.31 billion in 2024,14 while financial services benefit from rising digital penetration and the formalization of transactions. Together, these sectors underscore India's robust growth potential.

WisdomTree Directly Addresses India's Premium Equity Valuations

In February 2008,15 India Earnings Fund (EPI). EPI is designed to track, before fees and expenses, the total return performance of the WisdomTree India Earnings Index. This Index focuses on profitable companies in India and weights them not by market capitalization but by earnings. The biggest weight is the company that had the most earnings. What we tend to see in the annual rebalances:

- Companies where share prices outperform earnings growth see weight trimmed.

- Companies where share prices underperform earnings growth see weight increased.

- This bias toward following the fundamentals has been a notable valuation hedge, keeping the earnings-based valuation metrics for the WisdomTree India Earnings Index consistently below those of the MSCI India Index, a popular benchmark weighted by free float market capitalization.

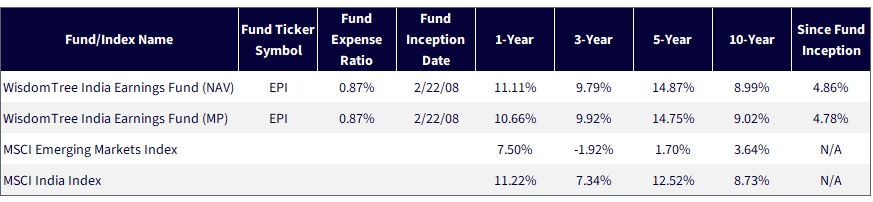

Figure 1: Standardized Performance

Sources: WisdomTree, FactSet, LSEG, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 1/23/25, with returns as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

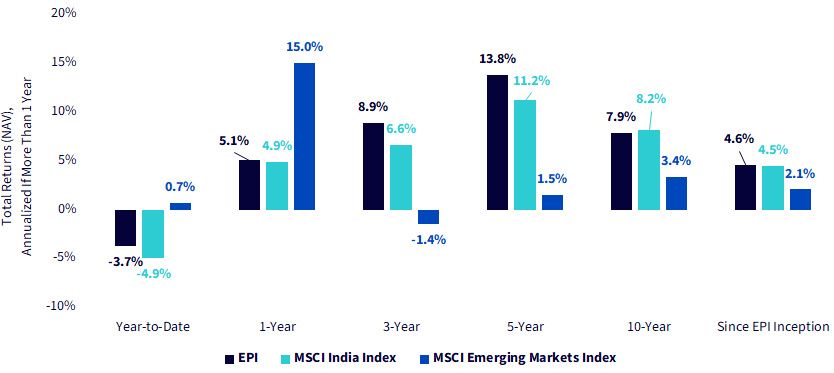

When we look at the case for India, a lot is founded on things that will occur in the coming decades, not necessarily next week or next month. Coming off of stronger performance in recent years, India's equity performance to start 2025, at least so far, has not been great, but it's also true we are talking about roughly three weeks—a very short period.

As we see in figure 2, over 3, 5 and 10 years, India's equities have dramatically outperformed those of broad emerging markets.

Figure 2: India Has Been a Longer-Term Performance Story

Sources: WisdomTree, FactSet, LSEG, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 1/23/25, with returns as of 12/31/24. EPI returns are shown at NAV. EPI inception date was 2/22/08. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

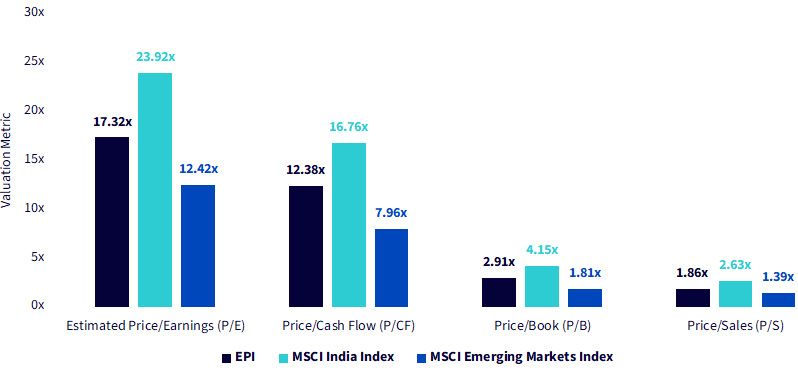

In figure 3, we see how EPI is controlling the risk of India's valuation, which is typically higher than broader emerging markets. Overall, India tends to be a high-growth market, and many are familiar with the demographics and other stories that can fuel this trend. However, even with all of that known, EPI's valuation metrics still look attractive relative to the MSCI India benchmark.

Figure 3: EPI Looks Less Expensive on a Range of Valuation Measures Relative to MSCI India

Sources: WisdomTree, FactSet, LSEG, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 1/23/25, with valuation metrics as of 12/31/24. Past performance is not indicative of future results. Subject to change.

Conclusion: The India Thesis Is Based on Seeing Certain Things over 10–20 Years

In looking at India as a possible investment thesis, we continually note that there is short-term, and there is long-term. If interest rates in developed markets remain higher for the near term, can this take focus and momentum away from investing in India? Absolutely. However, when we recognize that the political polarization, particularly of U.S. vs. China, doesn't appear to be diminishing, the focus on India may never be too far from focus. If emerging markets equity investors actively seek to tilt away from China, in many cases, this leads them tilting toward India.

There can be volatility and correction, but if people are looking to align with a high-growth story in emerging markets within a democratic country, India could be worth consideration.

1 Source: "What does the future hold for India?" McKinsey & Company, 7/24.

2 Source: e-Conomy: India 2023, the economy of a billion connected Indians, 2023.

3 Source: https://www.statista.com/topics/2157/internet-usage-in-india/

4 Source: Cornelli et al., "The organization of digital payments in India—lessons from the Unified Payments Interface (UPI)," Bank of International Settlements, 12/24.

5 Source: Christian Alonso & Margaux MacDonald ,"Advancing India's Structural Transformation and Catch-up to the Technology Frontier," IME eLibrary, 7/9/24.

6 Source: Anand et al., "Tight Liquidity Shackles Indian Banks' Robust Credit Growth," S&P Global, 2024.

7 Source: James Hsiao and Royston C. Tan, "Foreign direct investment reviews 2024: India," White & Case, 2024.

8 Source: Sandya Krishnan, "Understanding India's evolving middle classes," East Asia Forum, 5/21/24.

9 Source: Suprita Anupam, "Behind Apple's ‘Make In India' Push for iPhone," Inc 42, 11/29/24.

10 Source: Reed et al., "Can India Unlock the Potential of its Youth," Financial Times, 4/28/23.

11 Source: Sonal Khetarpal, "Why informal jobs rule the roost in India, hurting development," India Today, 4/1/24.

12 Source: "UPI transactions surged to a record 16.73 billion in December, value at Rs. 23.25 trillion (US$ 271.96 billion)," India Brand Equity Foundation, 1/2/25.

13 Source: "India's stock market needs domestic investors now more than ever," Economic Times, 1/23/25.

14 Source: Karan Kashyap, "The Rise of India's Pharmaceutical Industry to a Forecasted $450 Billion," Forbes, 11/16/24.

15 The WisdomTree India Earnings Fund was launched on February 22, 2008.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. As this Fund has a high concentration in some sectors, the Fund can be adversely affected by changes in those sectors. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.