AI Gold Rush: Who Wins the Battle for Compute, Capital and Open-Source Dominance?

Published February 18, 2025

Christopher Gannatti, CFA

Global Head of Research

Key Takeaways

- The rise of DeepSeek’s cost-efficient artificial intelligence (AI) models is challenging the dominance of high-cost, proprietary AI systems, potentially accelerating a shift toward decentralized AI development.

- As AI infrastructure investment soars—with Microsoft and Meta leading spending—Jevon’s Paradox suggests that greater AI efficiency will drive even higher demand for compute power and cloud services.

- With software-focused Funds like the WisdomTree Cloud Computing Fund (WCLD) and WisdomTree Cybersecurity Fund (WCBR) outperforming in early 2025, investors should watch for a potential leadership shift from semiconductor-driven AI growth to software-based AI innovation.

The AI ecosystem is evolving at an unprecedented pace, with innovations such as DeepSeek's latest models challenging traditional AI economics. Alongside this, capital investment in AI infrastructure, cloud computing and reasoning models is reshaping industry landscapes.

One of the key economic principles at play in this transformation is Jevon's Paradox—the idea that as technological efficiency increases and costs decrease, overall consumption tends to rise rather than fall. This was evident during the Industrial Revolution when advancements in coal-powered steam engines, which made energy cheaper, led to a surge in coal demand rather than a decline.1 Similarly, as AI models become more cost-efficient, we may witness an explosion in AI adoption across industries, driving increased demand for compute power, storage and AI-enabled applications.

For much of the past two years, the AI space has been dominated by a "winner-takes-all" paradigm, where a small number of highly capable players, such as OpenAI, Google DeepMind and Anthropic, controlled the majority of cutting-edge AI innovation. The assumption was that only a handful of well-funded firms would be able to push the frontier of AI due to the massive compute costs involved. However, DeepSeek and other emerging players are demonstrating that we may be moving toward a world with multiple competitive AI developers—many more than previously expected. This shift, driven by new efficiency techniques and open-source advancements, suggests that the future of AI will be more decentralized than previously thought.

Open Source vs. Closed Source

One of the major differentiators emerging in the AI space is the contrast between open-source and closed-source models. DeepSeek and Meta's Llama represent the growing trend of open-source AI development, allowing researchers and businesses to build upon existing architectures. Open-source AI promotes innovation, transparency and community-driven improvements, leading to faster iteration and potential security benefits. In contrast, proprietary models like OpenAI's GPT-4 and Google's Gemini operate in a closed-source manner, emphasizing control, monetization and competitive secrecy.

Meta has explicitly acknowledged that DeepSeek's rise reinforced its commitment to open-source AI. The company sees Llama as a critical component in fostering a decentralized AI landscape, allowing a broader audience to access and improve large language models. Meta's approach stands in stark contrast to OpenAI's shift toward proprietary commercialization, indicating a strategic divergence in how AI leaders envision the future of model accessibility.2

Historically, similar battles between open and closed ecosystems have played out in the technology sector:

- The competition between Microsoft's Windows and the open-source Linux operating system mirrored this dynamic. While Windows dominated commercial adoption due to extensive enterprise support, Linux gained traction in cloud computing, servers and developer communities, ultimately proving essential in shaping modern infrastructure.

- The Android vs. iOS ecosystem presents another example—Android's open-source nature led to widespread adoption and device diversity, while Apple's closed system optimized security, performance and seamless integration. In the AI space, the long-term viability of open-source models will likely depend on sustained community contributions and enterprise adoption, as well as the ability to monetize open AI solutions.

The DeepSeek Disruption: Cost Efficiency and Model Advancements

DeepSeek's introduction of reasoning models, such as DeepSeek-R1, has sent shockwaves across the AI industry. These models boast significantly lower training and inference costs compared to their Western counterparts, with training costs estimated at approximately $5.6 million—a fraction of OpenAI's GPT-4o.3 However, it is important to note that this figure likely reflects only the final training run, excluding the broader research, failed iterations, data acquisition and infrastructure expenses that contribute to the total cost of developing such a model.4 This cost reduction is attributed to novel efficiency techniques such as 8-bit precision, optimized phrase processing and selective activation of model components.5

Benchmark Performance and the Rise of Reasoning Models

DeepSeek's models have demonstrated strong performance in key AI benchmarks, including reasoning tasks and mathematical problem-solving, positioning them as formidable competitors to existing LLMs.6 Specifically:

- MMLU-Pro Benchmark: This test measures an AI model's proficiency across multiple-choice questions spanning various academic subjects, including mathematics, science and history. A higher score signifies a model's ability to generalize knowledge effectively across disciplines. DeepSeek-R1 achieved a performance score of more than 90%, rivaling models such as OpenAI's o1 and Google's Gemini.7

- AIME 2024 Evaluation: Designed to assess mathematical reasoning and problem-solving skills, AIME (American Invitational Mathematics Examination) presents challenging algebra and geometry problems typically solved by high school students competing at the national level. DeepSeek's performance in this benchmark indicates strong numerical reasoning capabilities.8

- GPQA Diamond Evaluation: This benchmark focuses on general problem-solving ability, evaluating how well an AI model can tackle complex logical reasoning problems with limited contextual information. Higher scores in this test signify improved inferential thinking and decision-making accuracy, positioning DeepSeek models as competitive in high-level academic and research-grade tasks.9

The Future of Semiconductors and AI Infrastructure

The rapid expansion of AI and the increasing efficiency of models like DeepSeek-R1 are placing new demands on the semiconductor industry. The business models for semiconductor companies are evolving as AI workloads continue to shift from general-purpose computing to highly specialized AI accelerators. Companies such as Nvidia, AMD and Intel, alongside emerging players in AI chip design, are now focusing on developing specialized chips that optimize inference and training efficiency. The demand for high-performance GPUs, tensor processing units (TPUs) and domain-specific accelerators is driving both innovation and strategic capital investment.10

A key driver of this shift is the rising demand for AI-specific semiconductor designs, with foundries like TSMC projecting that AI-related revenue will account for 25% of their total revenue in 2025.11 Additionally, the distribution of AI chip consumption is becoming increasingly consolidated, with Nvidia alone expected to account for 72% of the global high-bandwidth memory (HBM) demand in 2025.12

Geopolitical tensions and supply chain challenges are also reshaping the semiconductor landscape. Export restrictions on high-performance AI chips have forced Chinese firms to innovate around hardware limitations, leading to the development of more efficient AI models that require fewer computational resources.13 Meanwhile, the U.S. and European nations are ramping up domestic semiconductor production efforts through initiatives like the CHIPS Act to mitigate dependency on foreign suppliers.14

Capital Investment in AI: A Shifting Landscape

Apple, Meta and Microsoft recently released their earnings reports, revealing key shifts in their AI-related capital expenditure plans. Apple signaled a steady but measured increase in AI investment, focusing primarily on integrating AI capabilities into its existing ecosystem rather than large-scale AI infrastructure spending.15 Meta, on the other hand, reaffirmed its aggressive stance on AI infrastructure, increasing its AI spending to $65 billion to accelerate GPU-enabled computing.16 Microsoft announced an estimated $85–$90 billion in AI-related expenditures for 2025, reflecting a 57% year-over-year increase, driven largely by expanding cloud AI services.17

These companies also indirectly acknowledged Jevon's Paradox in their reports. Microsoft, in particular, emphasized that as AI becomes more efficient and accessible, its demand across enterprise and consumer applications continues to rise, necessitating further investment in AI infrastructure.18 Meta's continued expansion in AI-driven services suggests a similar trend, where improved AI efficiency is driving broader adoption and increased infrastructure needs.19

The Road Ahead

DeepSeek's innovations represent a significant inflection point in AI development, demonstrating that cost-efficient models can rival—or even surpass—Western AI counterparts. This has profound implications for capital investment strategies, infrastructure planning and global AI competition.

As AI capabilities become more accessible, companies will need to rethink their approach to model deployment, compute scaling and monetization strategies. The interplay between cost reduction, increased adoption and the evolving geopolitical landscape will shape the next phase of AI's growth trajectory. The coming years will reveal whether established tech giants can adapt or new challengers will redefine the AI paradigm.

Software or Semiconductors?

The aforementioned context is helpful, but one of the bottom-line questions for investors moving forward from what we saw in late January 2025 regards whether semiconductors will continue their leadership in investment returns OR if these events represent a catalyst to shift the trend toward a leadership amongst software companies.

At WisdomTree, we have an array of strategies that will allow us to monitor performance for the signs of such a shift:

- WisdomTree Artificial Intelligence & Innovation Fund (WTAI): WTAI is designed to track the total return performance, before fees and expenses, of the WisdomTree Artificial Intelligence & Innovation Index. The strategy is focused on an overall exposure to the "AI Ecosystem," which includes significant exposure to semiconductors, but also to software, other hardware areas like robotics, and innovative companies doing interesting things with AI technology.

- WisdomTree Cloud Computing Fund (WCLD): WCLD is designed to track the total return performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index. The strategy is focused on companies employing the Software-as-a-Service (SaaS) business model and notably avoids the three largest public cloud infrastructure providers: Google Cloud, Microsoft Azure and Amazon Web Services.

- WisdomTree Cybersecurity Fund (WCBR): WCBR is designed to track the total return performance, before fees and expenses, of the WisdomTree Team8 Cybersecurity Index. The strategy is focused on companies using software to provide cybersecurity services to protect against what Team8 believes to be the primary potential threats of tomorrow.

Put simply, while WTAI represents a mixed exposure to software AND hardware, both WCLD and WCBR are basically fully exposed to software companies. We can show these strategies against the S&P 500 Index benchmark, which we know is heavily exposed to the Magnificent 7 (Amazon, Alphabet, Apple, Microsoft, Meta Platforms, Nvidia and Tesla).

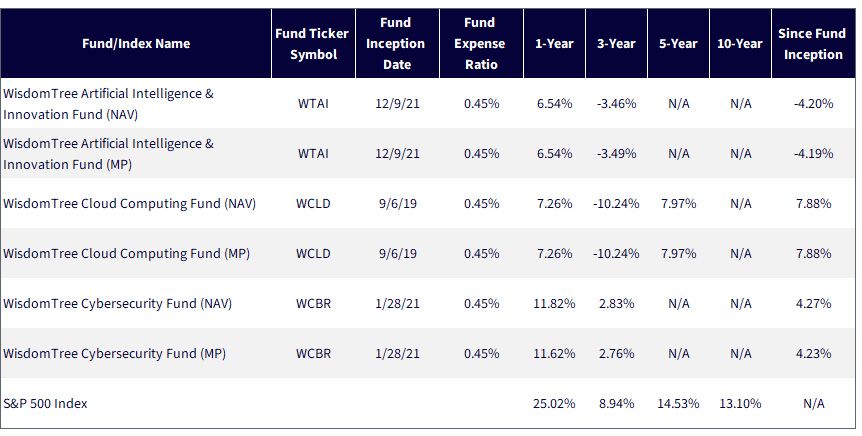

Figure 1 provides the standardized performance of these specific strategies.

Figure 1: Standardized Performance

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/1/25, with returns as of 12/31/24. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: WTAI, WCLD and WCBR.

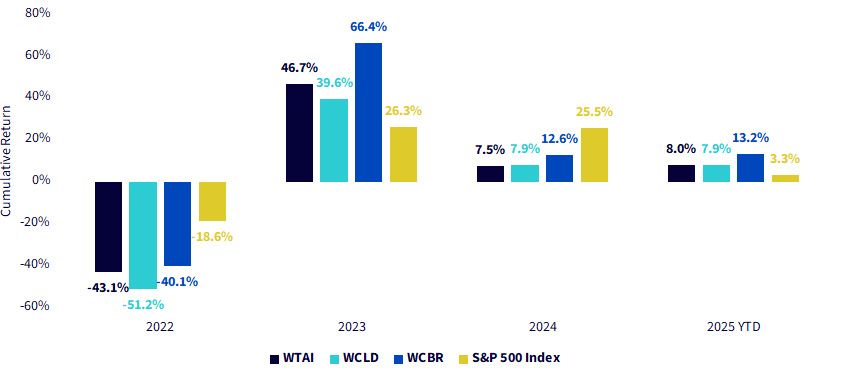

The performance that we saw in January 2025 is more interesting if we are able to consider how it looks relative to the three prior calendar years, all shown in figure 2:

- 2022: The dominant driver of market returns in this period was the very fast pace of interest rate hikes employed by the U.S. Federal Reserve in seeking to get inflation under control. Companies in WTAI, WCLD and WCBR had become used to roughly 0% interest rates during the pandemic period, so the stark transition led to a very sharp correction. The S&P 500 Index benchmark was also down nearly 20% for the year.

- 2023: While parts of 2023 could be characterized by a natural "recovery rally" after a year of tough equity market performance, the latter part of 2023 contained an implicit expectation—the U.S. Federal Reserve was thought to have conquered inflation, so many expected a fast pace of interest rate cuts to begin in early 2024. WCBR was the strategy that received the biggest relative boost from this expectation, exhibiting a return of 66% for the year.

- 2024: In hindsight, we know that the U.S. Federal Reserve did not rush to cut interest rates in 2024—the first cut came in September. For much of the year, strategies like WCBR that had run up based on a certain set of expectations were searching for the more appropriate level and valuation. While the year ended okay, it was clear that the overall market preferred a focus on the world's largest companies—the Magnificent 7—and not necessarily a focus on the smaller companies in WTAI, WCLD and WCBR that more precisely embodied specific themes. It was also clear that the market was very focused on hardware, especially semiconductors and Nvidia, and not as much on software.

- 2025 YTD: Now that we are nearly halfway through February 2025, we can see that WCBR, WTAI and WCLD took up performance leadership over the S&P 500 Index. It may be too early to indicate that this is THE shift signifying that from here, software company returns should be stronger than hardware company returns or that the market's rally is broadening out beyond the largest companies—but it is important to note anything that moves the focus from Nvidia toward something else. Maybe DeepSeek, when we look back, was this event. For those looking to position in this manner, WCLD, WTAI and WCBR could look interesting.

Figure 2: Setting Context with Prior Calendar Year Performance

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/12/25, with returns as of 12/31/24 and 2025 YTD meaning through 2/11/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: WTAI, WCLD and WCBR.

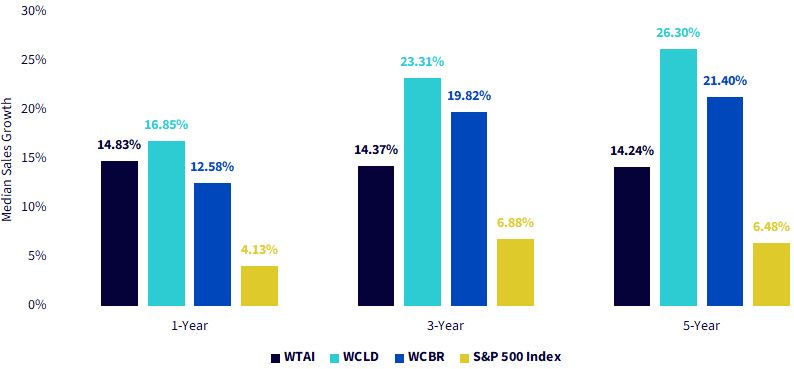

In figure 3, we simply remind ourselves of the basis thematic rationale. The S&P 500 Index—many view these statistics as those of the broad U.S. market. We see the median sales growth figures here. WTAI, WCLD and WCBR all indicate median sales growth figures significantly above these levels, which is important as these strategies also contain much higher risk than that of the S&P 500 Index. The stronger potential growth is the reason this incrementally higher risk could make sense.

Figure 3: Strong Historical Sales Growth of WTAI, WCBR and WCLD

Source: WisdomTree, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 2/1/25, with median sales growth as of 12/31/24. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: WTAI, WCLD and WCBR.

Conclusion: WCLD and WCBR for Specific Software Exposure

As we move through 2025, it will be interesting to see if software stocks truly take over the performance leadership from hardware stocks. If this does indeed happen, WCLD and WCBR are two investment tools in the toolkit that could benefit. WTAI does include a significant software exposure, but this is combined with a significant exposure to semiconductors, albeit not with a majority in Nvidia, the largest company in that particular space.

1 Source: Anita Hamilton, "What Is ‘Jevons Paradox ‘and Why Was Microsoft's CEO Posting About It Late at Night?" Barron's, 1/28/25.

2 Source: Nowak et al., "Meta Platforms Inc.: Is the Bull Case Ahead?" Morgan Stanley Research, 1/30/25.

3 Source: Patel et al., "DeepSeek Debates: Chinese Leadership On Cost, True Training Cost, Closed Model Margin," Semi Analysis, 1/31/25.

4 Source: Patel, 1/31/25.

5 Source: "The Current State of AI," Social Capital, 1/25.

6 Source: Patel, 1/31/25.

7 Source: "The Current State of AI," Social Capital, 1/25.

8 Source: Patel, 1/31/25.

9 Source: Patel, 1/31/25.

10 Source: Chan et al., "AI Semi: Additional thoughts on DeepSeek Impact," Morgan Stanley Research, 1/30/25.

11 Source: Chan, 1/30/25.

12 Source: Chan, 1/30/25.

13 Source: "The Current State of AI," Social Capital, 1/25.

14 Source: Chan, 1/30/25.

15 Source: Woodring et al., "Apple, Inc.: Better-than-Feared March Q Creates Cleaner Catalyst Path," Morgan Stanley Research, 1/31/25.

16 Source: Nowak, 1/30/25.

17 Source: Weiss et al., "Microsoft: 2Q25 Results—Working to Find the Right Balance," Morgan Stanley Research, 1/30/25.

18 Source: Weiss, 1/30/25.

19 Source: Nowak, 1/30/25.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WTAI: The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended.

WCLD: The Fund invests in cloud computing companies, which are heavily dependent on the internet and utilizing a distributed network of servers over the internet. Cloud computing companies may have limited product lines, markets, financial resources or personnel and are subject to the risks of changes in business cycles, world economic growth, technological progress and government regulation. These companies typically face intense competition and potentially rapid product obsolescence. Additionally, many cloud computing companies store sensitive consumer information and could be the target of cybersecurity attacks and other types of theft, which could have a negative impact on these companies and the Fund. Securities of cloud computing companies tend to be more volatile than securities of companies that rely less heavily on technology and, specifically, the internet. Cloud computing companies can typically engage in significant amounts of spending on research and development, and rapid changes to the field could have a material adverse effect on a company’s operating results. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

WCBR: The Fund invests in cybersecurity companies, which generate a meaningful part of their revenue from security protocols that prevent intrusion and attacks to systems, networks, applications, computers and mobile devices. Cybersecurity companies are particularly vulnerable to rapid changes in technology, rapid obsolescence of products and services, the loss of patent, copyright and trademark protections, government regulation and competition, both domestically and internationally. Cybersecurity company stocks, especially those that are internet-related, have experienced extreme price and volume fluctuations in the past that have often been unrelated to their operating performance. These companies may also be smaller and less-experienced companies, with limited product or service lines, markets or financial resources and fewer experienced management or marketing personnel. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is heavily dependent on quantitative and qualitative information and data from one or more third parties, and the Index may not perform as intended.

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.