A Nice Dose of “Don’t Fight the Fed”

Published June 21, 2023

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Throughout this Fed rate hike cycle, there always seemed to be some sort of disconnect between what the policy makers were saying and what the money and bond markets were thinking. At various times, you got the sense it was a case of either “don’t fight the tape” or “don’t fight the Fed.” Based upon recent developments in the Fed Funds Futures arena and the U.S. Treasury (UST), it’s increasingly looking like a “sea change” in sentiment has occurred where “don’t fight the Fed” is now winning out.

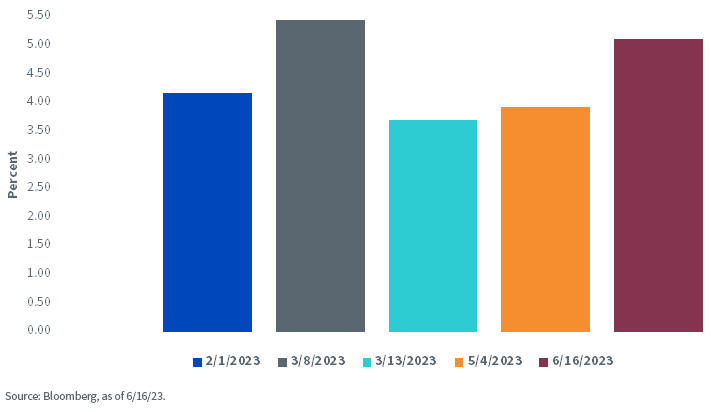

Let’s first take a look at Fed Funds Rate expectations for the remainder of 2023 now that we’re in a post-June FOMC world. It has been truly remarkable to see how these expectations have shifted in just a very short time. Literally the day after the May Fed gathering, the implied Fed Funds Rate for January 2024 stood at 3.93%, or close to the lows that were being posted in the immediate aftermath of the regional banking fears around mid-March. As of this writing, the implied level has soared to 5.12%, or the mid-point of the current Fed Funds trading range, an incredible turnaround of nearly 120 basis points (bps). Essentially, the market went from pricing in more than 100 bps worth of rate cuts by the beginning of next year to a scenario of only one cut, “tops,” and that’s assuming the Fed raises rates one more time this year.

Implied Fed Funds Rates - Jan 2024

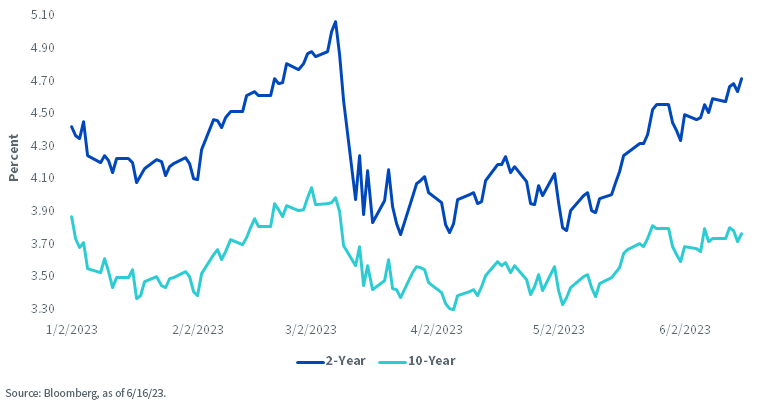

Needless to say, this shifting Fed rate outlook has also had a rather visible impact on UST yields. In terms of the widely followed 10-Year note, the yield has risen to just under 3.80% as I write this blog post, or about 45 bps from its low point in early May. While this is certainly a noteworthy increase, the spike in the UST 2-Year note yield has been twice this amount over the last month or so. To provide perspective, the 2-Year yield has risen almost 95 bps and is trading around the 4.75% threshold. While the UST 2-Year yield has not made it back to its pre-regional-banking turmoil high watermark of 5.07%, this recent move may still have more upside, given the shifting Fed rate outlook (see graph).

U.S. Treasury Yields

Conclusion

It’s fascinating to see that as we move into full summer mode, you don’t hear much, if any, talk about rate cuts. What was at one point supposed to be a time when the Fed was going to begin pivoting toward rate cuts, the discussion has now changed to whether Powell & Co. will implement one or two rate increases before this hiking cycle is over. As we’ve seen time and time again, monetary policy dynamics in the money and bond markets can change quickly and in a very notable fashion, which keeps elevated volatility in play for the fixed income investor.

Categories

Related articles

‘Warsh’ and Dry

What’s ‘Under the Hood’ of Your Core Bond Position?

Powell Stays…Should the Dot Plot?

Fed Watch: Powell’s Last Stand & What Comes Next?

Inflation’s First Official Debut

Nowhere to Hide…Except Maybe Treasury Floating Rate Notes

How to Mitigate Software Exposure in Bonds

Fed Watch: Between a Rock and a Hard Place

One Week Later

About the contributor

Kevin Flanagan

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.