DLN

U.S. LargeCap Dividend Fund

Published March 2, 2026

Global Head of Research

For nearly two decades, U.S. equity leadership had a clear pattern: own growth stocks, concentrate in the innovation complex and avoid high dividend yield strategies that seemed anchored to an earlier market regime. The rise of the ‘Magnificent 7’ reinforced the idea that reinvestment, not dividend income, was the path to outperformance.

Yet 2026 is telling a different story.

The WisdomTree U.S. High Dividend Fund (DHS), a strategy with a nearly 20-year history, has broken into performance leadership. What makes this shift notable is not simply that dividends are working. It’s that the definition of “value” itself has evolved. Today’s value exposures can include companies like Alphabet and Amazon, businesses once synonymous with pure growth. As cash flow generation matures across mega-cap tech and earnings dispersion widens, dividend yield is no longer a signal of stagnation. It may be a signal of durability.

Markets change slowly, until they don’t. This could be one of those moments.

In Figure 1, I was surprised by two things in the year-to-date period so far in 2026:

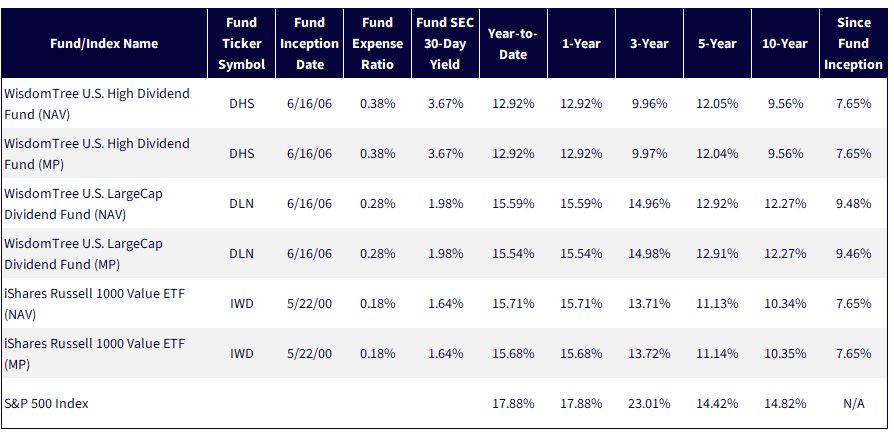

Sources: WisdomTree, FactSet, Morningstar specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed February 14, 2026 with returns as of February 13, 2026 for Figure 1a and as of December 31, 2025 for Figure 1b. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: DHS, DLN, IWD.

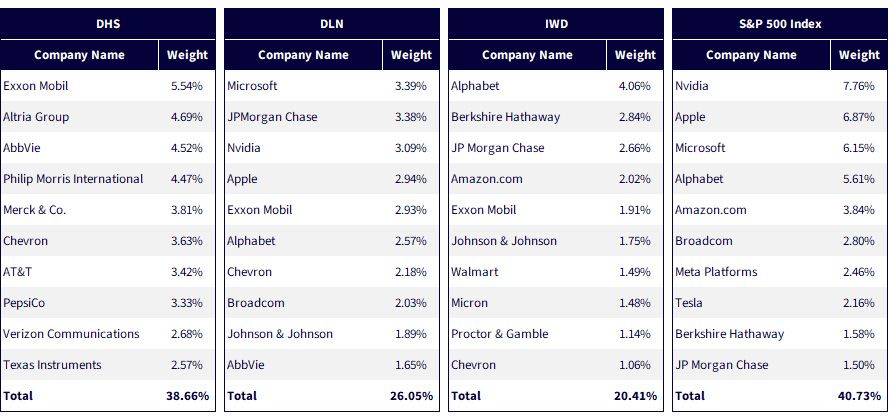

Look at the top holdings and the evolution becomes obvious. DHS still reflects what many would recognize as classic value, with focal points in energy, tobacco, pharmaceuticals and telecom. These are cash-generative, higher-yielding businesses that historically define dividend and value investing. The profile is distinct.

DLN and IWD tell a different story. Microsoft, Nvidia, Apple, Alphabet and Amazon now sit comfortably inside “value” portfolios. That doesn’t mean these strategies have abandoned discipline. It means the definition of value has expanded alongside the market itself. Mega-cap technology companies matured, generated enormous free cash flow and, in some cases, initiated large streams of cash dividends, qualifying for inclusion.

But composition matters. On a top-10 basis, DLN and IWD now resemble the S&P 500 more closely than in the past, something many investors may not realize. DHS remains structurally differentiated. If leadership rotates away from mega-cap tech and toward more traditional cyclical or defensive value sectors, that distinction becomes meaningful.

To start 2026, it already has.

Sources: WisdomTree, Morningstar, FactSet, with data as of January 31, 2026. Subject to change.

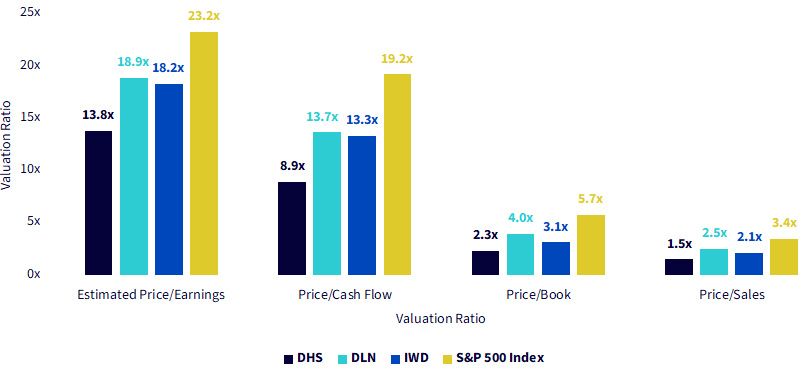

DHS is not just different in composition—it is materially different in valuation. On estimated price-to-earnings, DHS sits at 13.8x versus 18–19x for DLN and IWD and more than 23x for the S&P 500. The gap widens on price-to-cash-flow: 8.9x for DHS compared with roughly 13–14x for DLN and IWD and 19x for the broad market. Even on price-to-book and price-to-sales, DHS trades at a meaningful discount. This is not a subtle spread—investors are paying materially less for each dollar of earnings, cash flow and assets. If market leadership broadens beyond mega-cap growth, that valuation cushion could matter significantly—as it has so far in 2026.

Sources: WisdomTree, Morningstar, FactSet, with data as of January 31, 2026. Subject to change.

For years, market leadership rewarded concentration in growth and the reinvestment trade. Dividend strategies, especially those rooted in more traditional sectors, often lagged as capital gravitated toward mega-cap innovation. But markets are adaptive systems. As growth matured into cash flow, “value” evolved, absorbing many of yesterday’s disruptors into today’s income and value portfolios.

That evolution creates nuance, and opportunity.

Some value strategies now look structurally closer to the S&P 500 Index benchmark than many investors appreciate. Others remain distinctly positioned in classic, higher-yielding sectors and trade at materially lower multiples. When leadership narrows, convergence helps. When leadership broadens or rotates, differentiation matters.

The early leadership of 2026 suggests the market may be reassessing what it is willing to pay for growth versus what it demands in return for cash flow. If that repricing continues, structure, not just style labels, could define the next phase of outperformance.

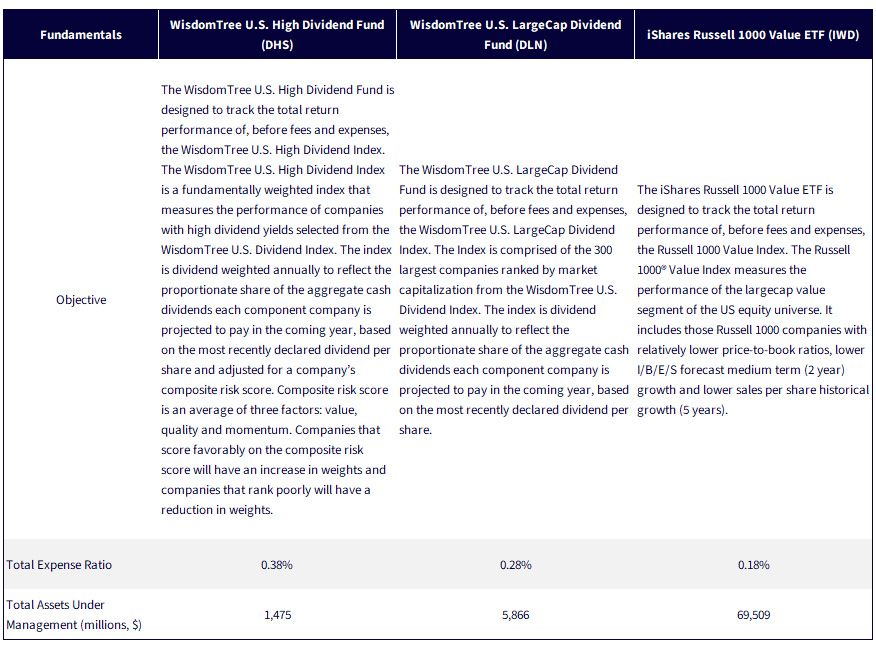

Sources: Respective ETF fund pages, with Assets Under Management as of February 13, 2026. Subject to change.

There are risks associated with investing, including possible loss of principal. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DHS: Funds focusing their investments on certain sectors and/or regions increase their vulnerability to any single economic or regulatory development. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

DLN: The Fund invests primarily in the securities of large-capitalization companies. As a result, the Fund’s performance may be adversely affected if securities of these companies underperform securities of smaller capitalization companies or the market as a whole. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended.

For IWD’s risk disclosures, click here.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.