AIVI

International AI Enhanced Value Fund

Published July 17, 2025

Global Head of Research

For over a decade, U.S. equities—especially large-cap technology—enjoyed an aura of invincibility. From the end of the global financial crisis through to the artificial intelligence (AI)-fueled performance of 2023 and 2024, the S&P 500 Index outpaced almost every major global benchmark, driving narratives around American economic dominance, innovation and valuation resilience.1 But the edifice of U.S. equity exceptionalism may be showing cracks. In 2025, the long-ignored international developed markets—represented by the MSCI EAFE Index—are staging a performance renaissance, with European and Japanese equities quietly outperforming their U.S. counterparts for the first six months of the year.

This turning point is not a simple story of mean reversion. Rather, it reflects a multilayered rotation in both market structure and macroeconomic regime. In Europe, the decade-long underinvestment in energy infrastructure is giving way to a €2 trillion capital expenditure (capex) supercycle, driven by power grid modernization, data center expansion and electrification—all occurring with low regulatory risk and mid-to-high single-digit EPS growth expectations.2 Meanwhile, Japan, long mired in deflationary stagnation, is enjoying a convergence of factors—export resilience despite tariffs, consumer sentiment inflection and corporate governance reforms—that make its equity market appear structurally re-rated rather than cyclically rebounding.

The U.S., by contrast, faces valuation fatigue and a growing set of external vulnerabilities. It's possible that much of the U.S. outperformance in the past decade stemmed not from superior fundamentals, but from valuation expansion—a trend possibly at risk of reversal amid policy uncertainty, AI competition from China and the fading of dollar strength.3 Simultaneously, tariff policy and geopolitical friction are acting as catalysts for global capital reallocation—prompting corporates and allocators to de-risk their exposure to U.S. assets and re-engage with overlooked international equities.

This backdrop creates fertile ground for a thematic shift in portfolio construction. Developed international markets are not just cyclical beneficiaries of a weaker dollar—they are structurally underappreciated sources of real earnings growth, cash flow yield and industrial reinvestment. The market's current re-rating of European utilities, industrials and Japanese capital goods stocks suggests that investors are increasingly valuing stability, domestic orientation and regulated profitability over high-multiple growth narratives.4 It’s possible that a new phase of international equity leadership may be just beginning.

As the performance tide shifted in favor of developed international markets, investors have been increasingly drawn to exposures that transcend traditional cap-weighted benchmarks like the MSCI EAFE Index. This shift is not just about rotating into cheaper markets—it reflects a renewed appreciation for the structural resilience found in sectors such as European utilities, capital-intensive industrials and Japan's export-driven manufacturing base. In this environment, value strategies have re-emerged as particularly relevant—not merely as mean-reversion trades, but as targeted expressions of enduring cash flow strength, capital discipline and embedded macro defensiveness. These strategies offer a framework for engaging with regions and sectors where fundamentals are stabilizing or even accelerating, despite a backdrop of global volatility and policy fragmentation.

Two strategies that stand out are the WisdomTree International High Dividend Fund (DTH) and the WisdomTree International AI Enhanced Value Fund (AIVI). While both operate within the same geographic universe as MSCI EAFE, their methodologies diverge significantly. DTH tracks an underlying index5 that takes a stronger stance on dividend yield, weighting companies by the size of their dividend distributions rather than by their market capitalization.

AIVI, by contrast, leverages a fundamentally grounded artificial intelligence model—developed in partnership with Voya Investment Management—to dynamically assess value across a complex and evolving factor landscape. The strategy employs machine learning to identify patterns in over 250 features across fundamentals, sentiment, macro indicators and other data. It is not bound to static valuation metrics, enabling the portfolio to adapt its definition of value as market regimes shift.

The Bottom-Line Question: Which of these strategies has performed better over different horizons and what types of attributes have been associated with each?

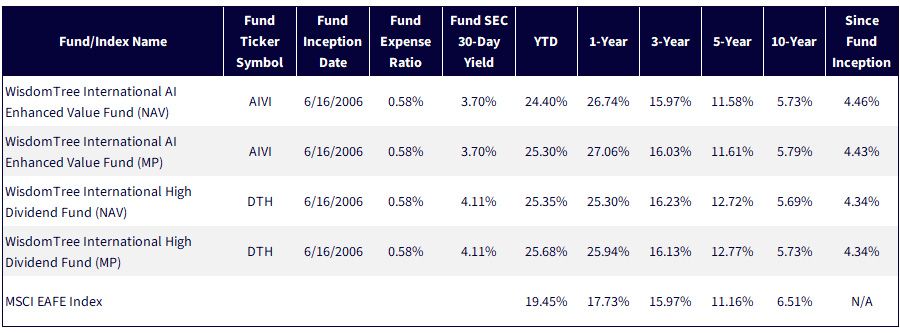

Figure 1: Standardized Returns

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/11/25, with returns as of 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. AIVI's objective and strategy changed effective 1/18/22. Prior to this date, AIVI performance reflects the investment objective of the Fund when it was the WisdomTree International Dividend ex-Financials Fund (DOO) and tracked the performance, before fees and expenses, of the WisdomTree International Dividend ex-Financials Index. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: AIVI, DTH.

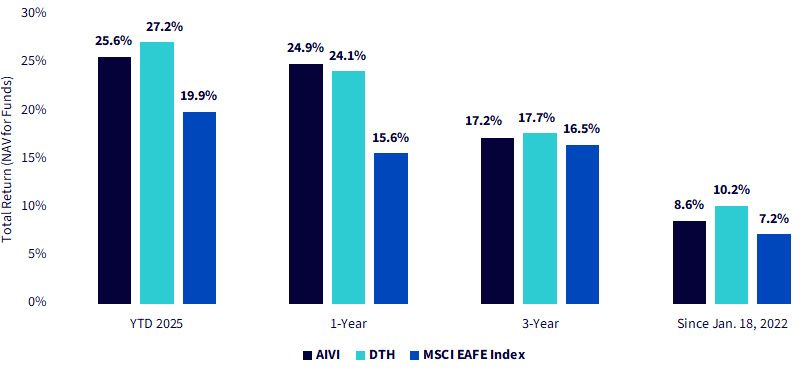

As visible in Figure 2, year-to-date in 2025, both value-oriented strategies—AIVI and DTH—have meaningfully outpaced the broad MSCI EAFE Index, returning 25.6% and 27.2%, respectively, versus 19.9% for the benchmark. This pattern holds over the one-year horizon, where AIVI leads with 21.8%, followed by DTH at 24.1%. Again, both are well ahead of MSCI EAFE's 15.6%. Even over longer timeframes (three years and since January 2022), the value strategies remain competitive or ahead, reinforcing the view that international value is not only rebounding—but leading. We think this may surprise many U.S.-based investors with large allocations to their home equity market.

Figure 2: The Leadership of Developed International Value

Sources: WisdomTree, FactSet, specifically data from the Fund Comparison Tool in the PATH suite of tools, accessed 7/11/25, with returns as of 7/10/25. NAV denotes total return performance at net asset value. MP denotes market price performance. AIVI's objective and strategy changed effective 1/18/22. Prior to this date, AIVI performance reflects the investment objective of the Fund when it was the WisdomTree International Dividend ex-Financials Fund (DOO) and tracked the performance, before fees and expenses, of the WisdomTree International Dividend ex-Financials Index. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: AIVI, DTH.

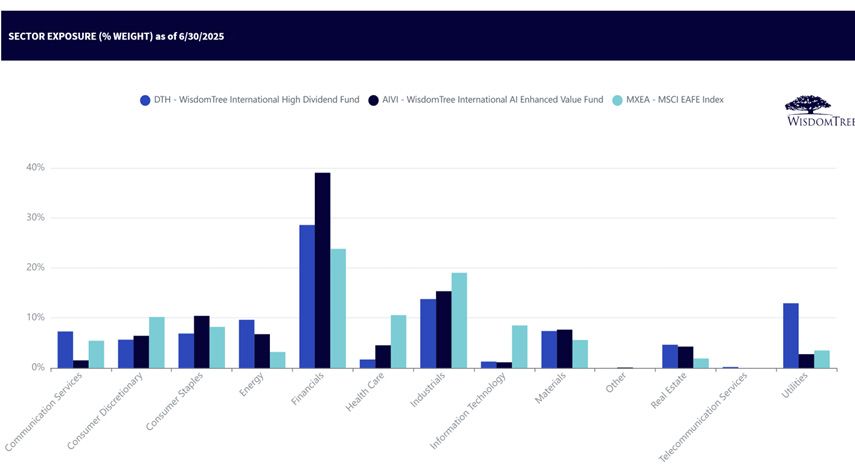

Though AIVI and DTH both operate within the value universe, their sector compositions reflect fundamentally different philosophies. AIVI concentrates its exposure in Financials (almost 40%), expressing conviction through a machine learning framework that dynamically allocates based on multifactor fundamentals. DTH, while also over-weight in Financials, distinguishes itself with a far more pronounced tilt toward Utilities. It’s interesting that AIVI had less weight, as of June 30, 2025, in Utilities than even the MSCI EAFE benchmark. This reflects DTH's dividend-weighted approach, which naturally favors sectors with steady payouts and higher dividend yields.

Meanwhile, AIVI shows relatively lower exposure to Energy, an area where DTH remains more meaningfully allocated. Both strategies are under-weight in Information Technology compared to the broad MSCI EAFE, reinforcing their focus on valuation and fundamental income streams over momentum or growth. To be fair, the MSCI EAFE benchmark had less than 10% exposure to Information Technology, making its look on a sector basis quite different than what typical U.S. equity investors may be used to seeing.

Figure 3: Two Very Different ValueTilts

Sources: WisdomTree, FactSet. Subject to change.

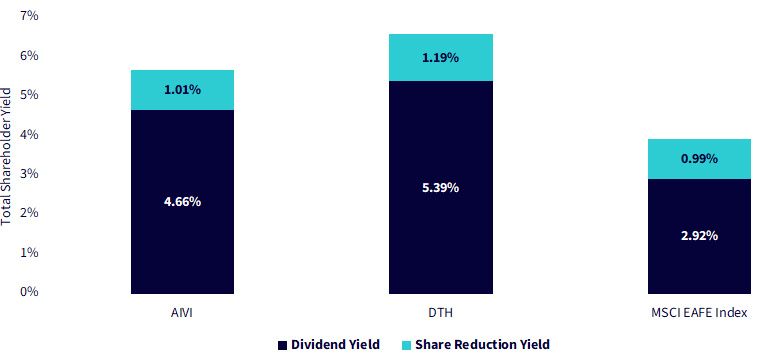

Both AIVI and DTH tilt meaningfully toward higher-yielding equities compared to the MSCI EAFE Index—but their motivations differ. AIVI incorporates dividend yield as one input among many in its machine-driven value framework, resulting in a strong 4.66% yield, strongly above the benchmark. DTH, on the other hand, is purpose-built for this attribute, explicitly weighting by dividends. It shows the highest total shareholder yield at nearly 7%, powered by a 5.39% dividend yield plus additional share reduction activity. This positioning affirms DTH's direct income orientation and its strong over-weight to traditional dividend sectors like Utilities and Energy.

Figure 4: Value with an Income Backbone

Sources: WisdomTree, FactSet, with data as of 6/30/25. Subject to change.

Growth Tradeoff: Not All Value Strategies Sacrifice Earnings Growth Upside

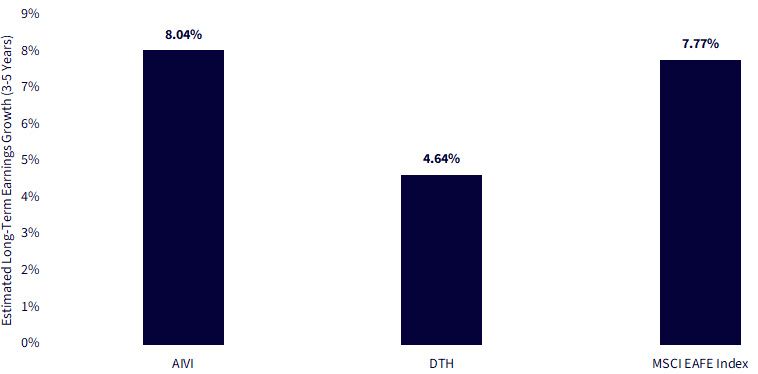

A common challenge for income-focused strategies is the growth concession—high-yielding stocks often come with slower earnings growth trajectories. That pattern is clearly reflected in DTH, which shows an estimated long-term earnings growth rate of 4.64%, well below the 7.77% projected for the MSCI EAFE Index. AIVI, however, tells a different story. Despite its value orientation, its 8.04% estimated earnings growth effectively exceeds the broad benchmark. This highlights the strength of AIVI's machine learning model, which dynamically identifies undervalued stocks without locking into slow-growth companies—potentially offering value exposure without the growth penalty.

Figure 5: A Value Exposure without Sacrificing Estimated Earnings Growth

Sources: WisdomTree, FactSet, with data as of 4/30/25. Subject to change.

As international equities re-emerge as credible leaders in global portfolios, investors have more reason than ever to move beyond generic benchmark exposure. AIVI and DTH both offer compelling access to the value premium across developed markets, but they do so through fundamentally distinct lenses.

DTH is a high-conviction dividend strategy—targeting income, leaning into Utilities and Energy, and delivering the highest shareholder yield of the group. AIVI, by contrast, uses artificial intelligence to flex across valuation signals, balancing yield with growth potential and sector agility. Its ability to exceed the MSCI EAFE Index in estimated earnings growth while maintaining a disciplined value orientation makes it uniquely adaptive.

Together, these strategies demonstrate that value in international markets is far from monolithic. DTH may appeal to income-seeking investors looking for payout durability, while AIVI offers a more growth-aware approach to value, suited for investors seeking adaptability in a shifting macro regime.

In a world where developed international equities are once again being valued on their own terms—rather than in the shadow of U.S. tech dominance—strategies like DTH and AIVI may be better aligned with the new structural realities taking shape across Europe and Japan.

1 Source: K. Martin, "Investors Ask ‘What Next' as the American Fever Breaks: Inflated Stock Prices May Have Been Mistaken for Growth-Driven Superiority," Financial Times, 5/22/25.

2 Source: A. Gandolfi, et al., Powering up Europe: Domestic, Defensive and Growing; ANew Era for Utilities (Goldman Sachs Global Investment Research Report), Goldman Sachs, 5/28/25.

3 Source: Martin, 2025.

4 Sources: Gandolfi, 2025, and D. Takayama, et al., Japan Export Tracker #3: What Corporates Are Telling Us (Goldman Sachs Global Investment Research Report), Goldman Sachs, 5/16/25.

5 DTH tracks the total return performance, before fees and expenses, of the WisdomTree International High Dividend Index.

DTH: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

AIVI: There are risks associated with investing, including the possible loss of principal. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in U.S. securities. For example, foreign securities may be subject to risk of loss due to foreign currency fluctuations, political or economic instability, or geographic events that adversely impact issuers of foreign securities. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on a quantitative model and the model may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.