WDAF

Asia Defense Fund

Published October 31, 2025

Global Head of Research

Macro Strategist, Model Portfolios

A Catalyst Born of Pressure, and Pragmatism

For decades, Washington's Indo-Pacific posture has depended on forward-deployed U.S. forces and an implicit guarantee of regional security. But that framework is changing. On his most recent Asia tour, President Trump made his message unambiguous: it's time for America's Asian allies to shoulder a greater share of their own defense.

The Wall Street Journal headline captured the moment, "Trump Tells Asia Allies: It's Your Turn to Boost Military Spending."1 From Gyeongju to Yokosuka, Trump's team pressed leaders in Japan, South Korea and Taiwan to accelerate defense buildouts amid rising threats from China and North Korea.

This isn't an isolated request. It's the logical sequel to a geopolitical pattern already in motion. European allies began hiking budgets after similar prodding during Trump's first term; Asian governments, facing sharper and more proximate threats, are now doing the same. The political rhetoric may sound transactional, but the underlying forces are structural. The Asia-Pacific is entering what one could call the era of defensive autonomy, a long-cycle transformation in which nations rearm, reorganize and reshore their defense industrial bases.

China's military modernization continues to accelerate, with live-fire drills rehearsing a Taiwan blockade and a growing maritime militia pushing into disputed South China Sea waters. North Korea, meanwhile, keeps testing cruise and hypersonic missiles with minimal external pushback.

In response, regional powers are rewriting their playbooks2:

Each of these developments—accelerating budgets, supply chain reshoring and defense tech localization—feeds into a sustained regional investment supercycle. It's not just about building tanks and ships; it's about upgrading industrial ecosystems, stimulating employment and embedding defense innovation into national development strategies.

Global defense spending surged to record highs in 2024, and Asia-Pacific accounted for nearly a quarter of the total.4 Investors have been quick to price U.S. and European defense primes into this new reality. Lockheed Martin, BAE Systems and Rheinmetall have already re-rated.5 But in Asia, the story is still young.

Despite their centrality to global rearmament, Asian defense champions have been structurally under-represented in global portfolios. Most defense exchange-traded funds (ETFs) are U.S.-centric, leaving a gap where the next decade's growth is most likely to occur. The result? A disconnect between geopolitical reality and capital allocation, a classic inefficiency that the WisdomTree Asia Defense Fund (WDAF) was designed to correct.

The WisdomTree Asia Defense Fund (WDAF) tracks the WisdomTree Asia Defense Index, and was launched in 2025 to capture the economic and industrial renewal underpinning Asia's rearmament. The Fund's methodology is not merely regional, it's strategically thematic.

The strategy targets companies that derive at least 10% of their revenue from defense activities and tilts toward those with higher exposure. This approach offers a pure-play orientation, filtering out conglomerates whose defense operations are marginal and amplifying those positioned at the heart of the military modernization wave.

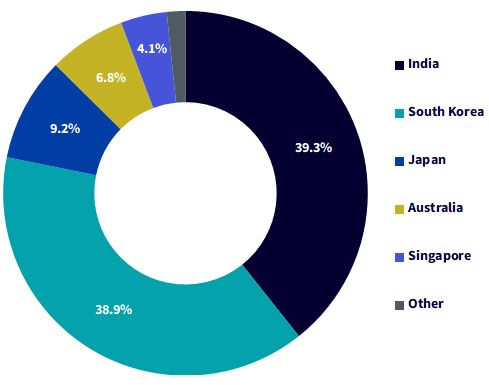

As is visible in figure 1, this Index includes companies from across Japan, South Korea, India, Taiwan and Southeast Asia. It is reconstituted semi-annually to reflect dynamic changes in the defense sector.

Figure 1: Country Exposures Emphasize the Markets Seeing the Spending Boost

Source: WisdomTree. Holdings for the WisdomTree Asia Defense Index as of 10/28/25. Subject to change. You cannot invest directly in an index.

The weighting system adjusts for both free-float market capitalization and exposure intensity, with caps to preserve liquidity and diversification.

Figure 2: Asia's Emerging Defense Primes

Source: WisdomTree. Holdings for the WisdomTree Asia Defense Index as of 10/28/25. Subject to change. You cannot invest directly in an index.

As is visible in figure 2, the strategy's top holdings illustrate its design logic. As of late October 2025, the portfolio's 10 largest names, ranging from Hanwha Aerospace and LIG Nex1 in South Korea to Hindustan Aeronautics, Mazagon Dock Shipbuilders and Bharat Electronics in India, represented about 57% of total weighting.

These companies aren't just national champions; they are exporters of security. Hanwha's joint venture in Poland for missile production, India's Cochin Shipyard expansion and Japan's Kawasaki Heavy Industries' global supply chain all point to the rise of Asia as not just a defense buyer, but a defense supplier.6

Where traditional ETFs often dilute exposure with adjacent sectors, such as transport, logistics or IT services, WDAF is architected to be undiluted and directional. Its revenue-adjusted weighting ensures that capital flows to the companies most directly benefiting from defense expenditure, not those tangentially related.

In a world of contested supply chains and shifting alliances, defense spending is one of the few areas where political consensus transcends party lines. Asian governments, whether democratic or autocratic, see military modernization as both a deterrent and a domestic growth engine.

The underinvestment gap is the crucial concept. Decades of limited regional capability have created an enormous catch-up opportunity. Now, with defense budgets rising and local champions scaling production, that gap is closing, fast.

Moreover, these defense ecosystems are technologically rich. Aerospace, cybersecurity, AI-driven command systems and precision manufacturing are increasingly interlinked. WDAF's Index captures this cross-sectoral synergy by including firms in advanced engineering, electronics and materials sciences that form the backbone of next-generation deterrence systems.

It's also notable that WDAF sits at the intersection of reshoring and strategic autonomy, two of the defining macro trends of the 2020s. Just as Europe is repatriating energy and semiconductor production, Asia is localizing defense supply chains, from munitions to propulsion to software. Investors who miss this parallel could underestimate the compounding nature of the theme.

Defense spending is fiscal stimulus with a flag on it. The capital that governments channel into defense rarely disappears. Instead, it circulates through supply chains, spurring high-value employment, research spending and manufacturing resilience.

Japan's $50 billion annual defense budget expansion, for instance, stimulates both heavy industry and semiconductor tooling; South Korea's naval buildout reinforces steel and shipbuilding demand; India's aerospace indigenization nurtures private-public R&D clusters.7

In aggregate, these effects resemble the "green energy multiplier" of the past decade, but this time, the driver is security, not sustainability. Both are forms of industrial policy, and both redirect capital toward long-duration assets with geopolitical tailwinds.

Why Now, and Why WisdomTree

Timing matters. Asia's defense modernization is not hypothetical, it's budgeted, legislated, and politically incentivized. Yet, the public market instruments to express this view have been sparse until now.

The WisdomTree Asia Defense Fund (WDAF) converts this strategic realignment into an investment that mirrors an index, sitting between two poles: the macro reality of rising security expenditure and the micro opportunity of under-owned Asian defense equities.

WisdomTree's innovation lies in translating a political transformation into a portfolio architecture, one that balances concentration (in high-exposure firms) with breadth (across the region). This is not a short-term trade on conflict; it's a long-term structural allocation to the economics of deterrence.

1 Source: A. Ward et al., "Trump Tells Asia Allies: It's Your Turn to Boost Military Spending," The Wall Street Journal, 10/29/25.

2 Source for bullets: Ward et al., 2025.

3 Refers to North Atlantic Treaty Organization.

4 Source: "Global Defense Spending Annual Snapshot," Forecast International, 2024.

5 Source: Bloomberg, with year-to-date data as of 10/29/25.

6 Sources: S. Seo, "South Korea's Hanwha Bets Big on Europe with Polish Missile Venture," KED Global, 9/3/25; "Cochin Shipyard Launches Three Complex Ships Showcasing India's Shipbuilding Capabilities," Economic Times, 10/17/25; E. Grant, "Kawasaki Heavy Industries: Navigating Global Shifts with Strategic Agility and Defense-Driven Growth," AINvest, 8/8/25.

7 Sources: G. Arthur, "Japan Passes Record Defense Budget, while Still Playing Catch-Up," Defense News, 1/16/25.; "South Korea's Shipbuilding and Steel Industry," Commodity Insights, 4/3/25; P. Nath, "How Private Players are Driving India's Defence Manufacturing Boom," ET Manufacturing, 9/14/25.

There are risks associated with investing, including the potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. Because the Fund invests primarily in the securities of companies in Asia, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Asia and to be more volatile than the performance of more geographically diversified funds. Many countries in the region have historically faced political uncertainty, corruption, military intervention and social unrest. To the extent that such events continue in the future, they can be expected to have an unpredictable effect on economic and securities market conditions in the region and may impact the ability of the Fund to buy, sell or otherwise transfer securities and cause the Fund to decline in value. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.