DXJ

Japan Hedged Equity Fund

Published October 8, 2025

Global Chief Investment Officer

Sanae Takaichi won the leadership of Japan's Liberal Democratic Party (LDP). Her election marks a historic turning point in Japanese politics as the LDP's first female president. The symbolism and characterization as Shinzo Abe 2.0 is powerful, yet markets care more about the scope of her mandate and the policies that follow. The LDP lost majorities in both chambers, so Takaichi must build bridges across a fragmented Diet, steady household confidence and convince a younger electorate that policy can deliver.

The election results add an important fiscal angle. Takaichi has signaled her plan to actively use the budget while promising responsibility. She has discussed a flat tax program that would lower rates to 10%, which we believe would boost consumption and support local economic stocks. She advocates strengthening Japan's semiconductor industry as part of her economic security agenda, which should benefit tech exporters via policy support alongside a weaker yen (JPY).

The early expectation is for a front-loaded package that leans into public investment, energy security and defense.

Equities would welcome a growth impulse. The public is not happy with rising prices and inflation partly been fueled by a weak yen, so there is some discussion about whether Takaichi and U.S. President Donald Trump could coordinate to support a rising yen.

The risk is that a thin governing margin forces political compromise, yet the direction of travel points to a larger fiscal footprint that tries to put real income back into households without derailing the disinflationary path now underway.

Tariffs and Localization

Trade policy has also moved from existential threat to manageable constraint. Tokyo and Washington have largely wrapped up a trade deal that caps auto tariffs at 15% rather than the original 25%. That is still a headwind for margins in parts of the value chain, yet the worst case receded. Japanese manufacturers have long since diversified production. Automakers assemble most North American sales inside the region. Approximately 70% of Japanese brand vehicles sold in the U.S. are made in North America.1 Machinery and electrical firms have meaningful footprints across the Association of the Southeast Asian Nations (ASEAN) and Europe, and 71.5% of Japanese manufacturers developed new suppliers over the past five years.2 When tariffs change, production schedules change with them.

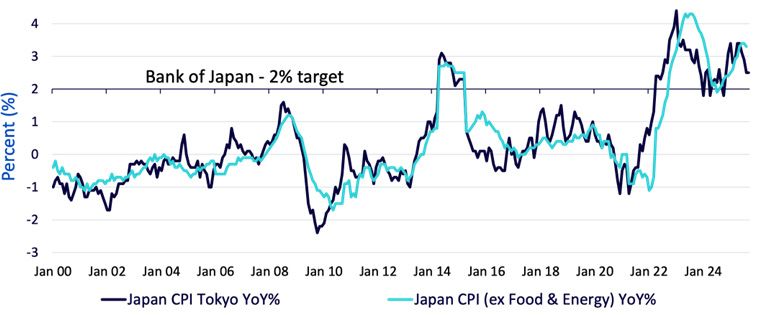

Monetary policy sits in the middle of this story. Governor Ueda has kept his options open. Inflation has been above target since October 2022, yet the Bank of Japan (BOJ) wants more evidence that the underlying trend is sustained by wages and demand.

Figure 1: Key Inflation Gauges above Bank of Japan's 2% Target

Sources: WisdomTree, Bloomberg, as of 9/30/25.

The BOJ would prefer not to hike into a fresh round of tariff uncertainty, yet the economic and wage trackers are consistent with cautious normalization. Takaichi has also called for monetary policy to remain accommodative, and her desire to be slow and deliberate in hiking may hinder its path.3

Takaichi Trades: WisdomTree Japan Playbook

Takaichi's victory brings a larger and earlier fiscal package that should support consumption. Factory automation and electrical machinery still benefit from reshoring and the energy transition build-out. Semiconductor equipment and components remain tied to a secular capital spending cycle in chips, with artificial intelligence (AI) orders a positive swing factor.

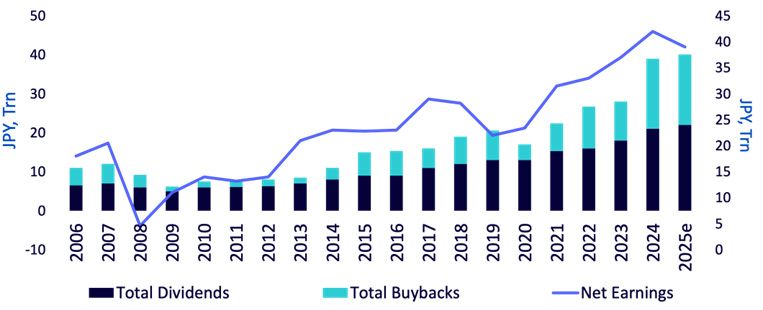

Corporate behavior has been a quiet force behind the recent strength in equity markets. Boards are returning more cash. Authorizations for buybacks have surged, and dividends are trending higher. The Tokyo Stock Exchange's push on cost of capital and low price-to-book laggards continues to change incentives. Idle assets are being sold. Cross holdings are slowly unwound. The outcome is a thicker cushion under earnings per share when top-line growth is modest. It is also the reason any cyclical pause feels less threatening than in past decades. Companies have more tools to defend results. They also have stronger balance sheets.

Sources: Universe of Tokyo Stock Exchange and Prime Market firms; net profits in fiscal year 2025 based on latest Toyo Keizai forecasts, WisdomTree, Bloomberg, FactSet, as of 6/30/25. Forecasts are not an indicator of future performance, and any investments are subject to risks and uncertainties.

For over five years, we have counseled investors to follow Warren Buffett into Japan, as his investments with Berkshire Hathaway have reinvigorated investor interest. But today, Buffett's ownership limits are capped as he aims to keep equity ownership levels around 10%.

That ceiling locks Buffett out of buying significantly more, even if his conviction deepens. The WisdomTree Japan Opportunities Fund (OPPJ) faces no such limits. With roughly 45% of its weight in the "Buffett basket" comprising his original investment in five Japanese trading houses, OPPJ gives investors access to the same exposure at a greater scale.

But OPPJ goes further. The portfolio layers in three additional pillars of corporate governance improvers, capital return champions and potential thematic opportunities, the core of which may be direct beneficiaries of Takaichi's agenda.

This broader set of Japanese companies are buying back stock, raising dividends and aligning compensation with shareholder value. This is not a cultural aspiration anymore. It's happening. Shareholder payouts in Japan have quadrupled over the past decade, with buybacks alone now eclipsing the total dividends of just 10 years ago.

OPPJ's thematic ideas are positioned in the industrial and defense sectors.

Takaichi has framed defense not as a peripheral issue, but as a core pillar of her "crisis management investment" agenda, explicitly naming defense among the strategic sectors to receive prioritized government backing. She has advocated for revising Japan's postwar constraints (including Article 9) to strengthen the Self-Defense Forces and expand Japan's military role while promoting domestic procurement and development of advanced defense technologies. In her view, defense is both a sovereignty imperative and a growth lever—government contracts, research and development (R&D) funding and export support under her policies could create sustained demand for domestic aerospace, weapons systems, cyber and defense supply chain firms. Because of that, Japanese defense and dual-use technology stocks may stand to gain disproportionately under her proposed fiscal, procurement and tax regime tilt.

OPPJ also incorporates a dynamic currency hedge that adapts yen exposure to prevailing market conditions on a monthly basis. The current hedge ratio is 75%, which helps performance during weak yen environments by avoiding depreciation headwinds, but it can be reduced if Takaichi pivots her focus to yen-strengthening dynamics.

While OPPJ includes several companies that may benefit from Takaichi's views, the WisdomTree Asia Defense Fund (WDAF) may be even more targeted.

If Europe's defense wake-up call came first, Asia's response is accelerating. South Korea, India and Japan sit at the heart of the region's transformation.

These programs are not temporary. Backlogs stretch years, exports diversify revenue streams and governments co-fund capacity expansions, turning cyclical manufacturing into something closer to utility-like cash flows.

The WisdomTree Asia Defense Fund (WDAF) is designed to track the WisdomTree Asia Defense Index, a strategy built to capture this regional surge. While global benchmarks may underrepresent Asia's defense revenues, this Fund aims to give investors direct access to Asia's defense buildout.

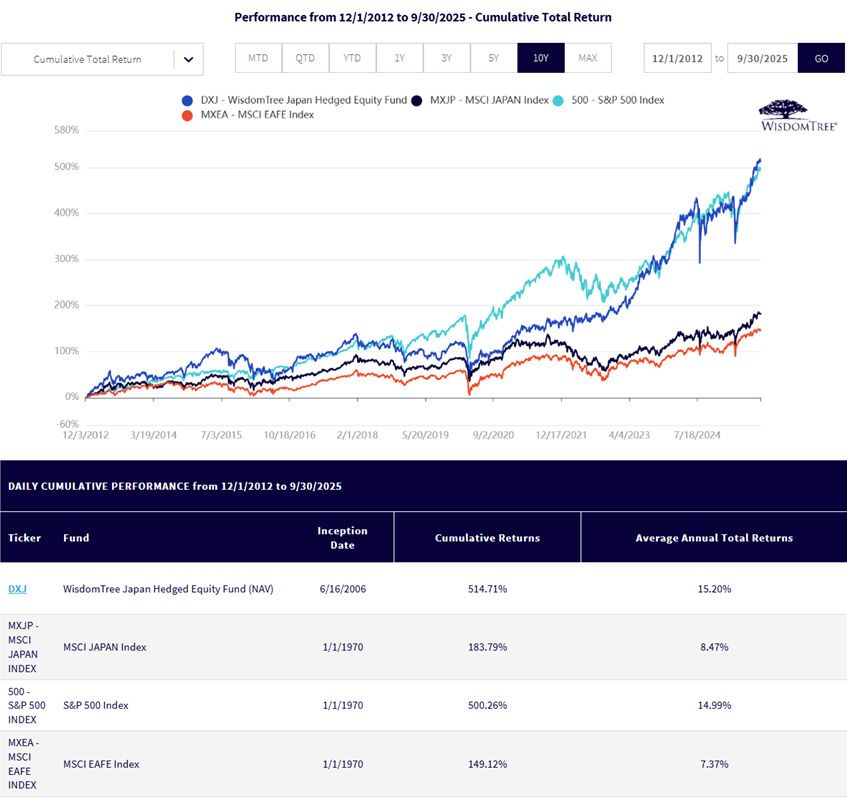

Let's review Japan's performance since Shinzo Abe first became prime minister. Few international equity benchmarks have kept up with the market-leading S&P 500. Broad international stocks that include currency exposure had literally half the annualized return over the last 13 years and led to cumulative total returns of just 150% versus 495% for the S&P 500.

Yet WisdomTree's currency-hedged DXJ did not just keep pace with the S&P 500 over this period; it slightly beat it. This shows the long-term compounding benefit of the currency component, but also the benefits of implementing a hedging program over the long run.

Source: WisdomTree Fund Comparison Tool, as of 10/3/25. You cannot invest directly in an index. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click here.

DXJ aligns well with the expected beneficiaries of Sanae Takaichi's victory and the sector-specific mix. DXJ has meaningful allocations to Materials, Financials and Industrials, sectors that we expect will benefit from increased fiscal stimulus.

DXJ incorporates a dividend-weighting methodology that tilts toward higher-quality companies with stable cash flows and strong shareholder return profiles. As investor preference rotates toward income-generating, capital-efficient businesses, DXJ is well placed to capture this shift.

The dividend orientation also aligns with the ongoing transformation in Japanese corporate behavior, where firms are increasingly deploying capital via share buybacks and great dividend payments—trends that have accelerated since the implementation of governance reforms and pressure from the Tokyo Stock Exchange (TSE).

DXJ's static currency hedge may also help isolate equity alpha from FX noise and potentially provide a cleaner and more stable source of return exclusively tied to the underlying equities.

This is especially important at a time when global macro conditions, particularly diverging central bank policies, are driving currency volatility.

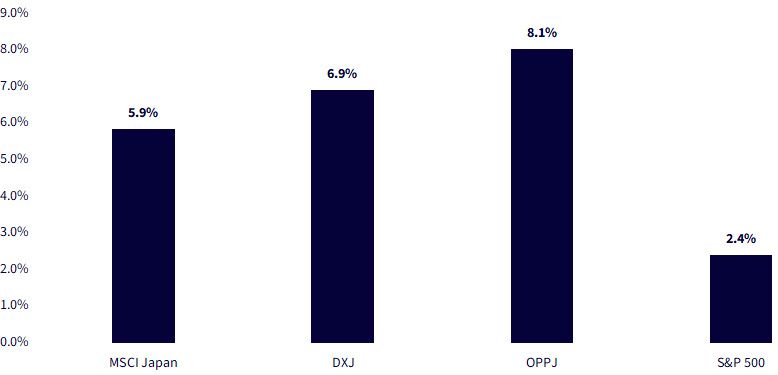

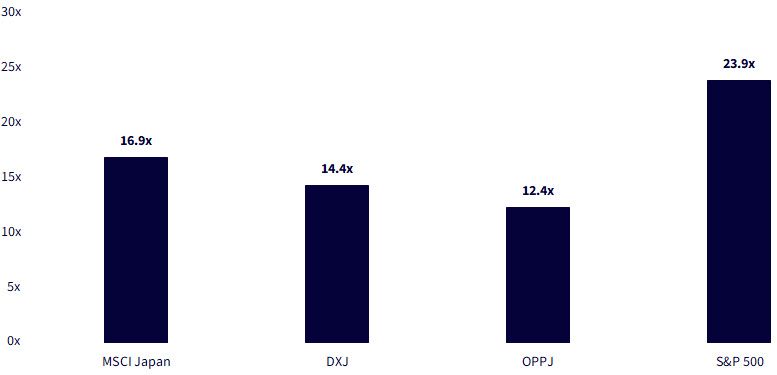

On the valuation front, while there are concerns that the U.S. market has elevated multiples, Japan is comparatively inexpensive despite starting to outperform the S&P 500 in 2025.

Sources: WisdomTree, FactSet, as of 9/30/25. You cannot invest directly in an index.

Sources: WisdomTree, FactSet, as of 9/30/25. You cannot invest directly in an index.

Japan has a new political anchor and a clearer economic path. Domestic demand appears resilient, trade frictions look manageable and the BOJ is edging toward normalization without stifling growth. Corporate reforms are simultaneously turning cash into returns. We think there are several interesting ways to target Takaichi's reform agenda and the emerging defense, export and economic growth themes through targeted strategies that also eliminate unnecessary volatility from yen exposure.

1 JETRO, Japan External Trade Organization.

2 JETRO, Japan External Trade Organization.

3 Kyodo News, 10/2/25.

There are risks associated with investing, including potential loss of principal. Foreign investing involves specific risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DXJ: The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs.

OPPJ: The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

WDAF: Funds focusing their investments on certain sectors may be more vulnerable to any single economic or regulatory development. This may result in greater share price volatility. Because the Fund invests primarily in the securities of companies in Asia, the Fund’s performance is expected to be closely tied to social, political and economic conditions within Asia and more volatile than the performance of more geographically diversified funds. Many countries in the region have historically faced political uncertainty, corruption, military intervention and social unrest. To the extent that such events continue, they can be expected to have an unpredictable effect on economic and securities market conditions in the region and may impact the ability of the Fund to buy, sell or otherwise transfer securities and cause the Fund to decline in value. Investments in non-U.S. securities involve political, regulatory and economic risks that may not be present in investments in U.S. securities. The Fund invests in the securities included in, or representative of, its Index. The Index may not perform as intended.

Global Chief Investment Officer

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.