DXJ

Japan Hedged Equity Fund

Published February 19, 2026

Global Chief Investment Officer

Investors are increasingly grappling with a familiar problem: U.S. equities are expensive, concentration risk is high and forward returns may look different than the last cycle. That does not mean opportunities are scarce. It means they are shifting.

Japan is one of the clearest examples. The combination of attractive valuations, improving domestic fundamentals and renewed global investor attention is creating an unusually compelling setup. Add evolving political dynamics and a changing global security backdrop, and Japan looks less like a tactical trade and more like a structural allocation investors should reassess.

A useful place to start is the relative opportunity set. The S&P 500 is not at bubble levels, but it is priced above its long-term norms. When markets trade at elevated multiples, the math tends to work against investors. Future returns typically compress and the margin for error shrinks.

Japan, by contrast, offers a very different valuation and risk premium profile. Although sovereign bond yields have risen, Japanese equities still offer a significantly higher equity risk premium. That is an important signal that stocks remain more compelling relative to bonds than they are in the U.S.

Higher Japanese yields are not automatically competition for stocks. Given starting valuations, Japan's equity market still looks attractively priced for long-term investors.

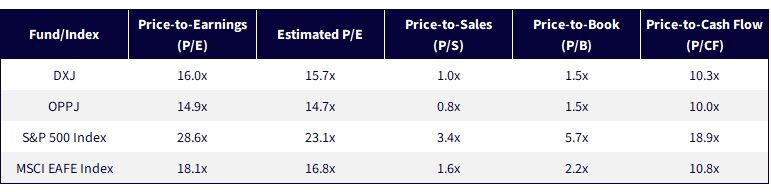

The global valuation gap is not marginal. It is significant. We see this in Figure 1 where we note an array of different equity indexes compared to two of WisdomTree's Japanese equity funds. Those two are:

Figure 1: Valuation Ratios

Sources: WisdomTree, FactSet, MSCI, S&P as of 1/31/2026. You cannot invest directly in an index.

Our two Japanese equity funds trade at a meaningful discount to U.S. large cap benchmarks, with forward price-to-earnings (P/E) valuations roughly nine turns below the S&P 500. Lower starting valuations historically provide a wider margin of safety and stronger long-term compounding potential.

One of the biggest questions investors raise is whether Japan's shifting interest rate regime is a problem. The more helpful framing is why yields are rising.

Japan's yield curve has steepened in recent quarters. Much of that steepening reflects improving macroeconomic conditions, including stronger growth and modest inflation. Those are the right reasons for rates to rise.

It also matters that Japan's debt dynamics differ from many Western economies. A large share of Japanese government debt is owned domestically, including by the Bank of Japan. Japan is not dependent on foreign demand to fund itself in the same way others are. Higher rates can even support consumption by improving returns for domestic savers and recycling savings back into the economy.

This is a meaningful shift. Japan is moving from economic stagnation to a more normal cycle where growth, inflation and yields interact in healthier ways.

Political catalysts matter when they accelerate structural change. Japan's latest election cycle and the policy direction that emerged have sharpened investor focus on several themes, including household support measures and national security.

Policy priorities have included potential tax relief and other initiatives aimed at reinforcing a more durable domestic recovery. At the same time, a firmer stance on China and a clearer push toward rearmament signal that defense spending may become a multi-year priority.

Investors have already seen how geopolitics can create sustained spending cycles. Japan's position in Asia and its alignment with U.S. strategic interests suggest that defense investment could become a long duration theme. Investors may gain exposure to a structural spending cycle without needing to assume an escalation scenario.

Japan's aging population has often been framed as a headwind. In an AI-driven world, that dynamic can shift.

AI and automation can help offset workforce constraints in aging societies by improving productivity and supporting output. Japan sits at the intersection of demographic pressure and industrial strength. It has an ecosystem of companies that participate in automation, advanced manufacturing and semiconductor supply chains.

Japan's relevance to AI infrastructure and enabling technologies adds another structural reason investors are reassessing the market. This is not simply a cyclical rebound story. It is a long-term positioning opportunity tied to global technological change.

A common investor objection is that single country exposure equals more risk. In practice, risk depends on how an allocation behaves inside a portfolio.

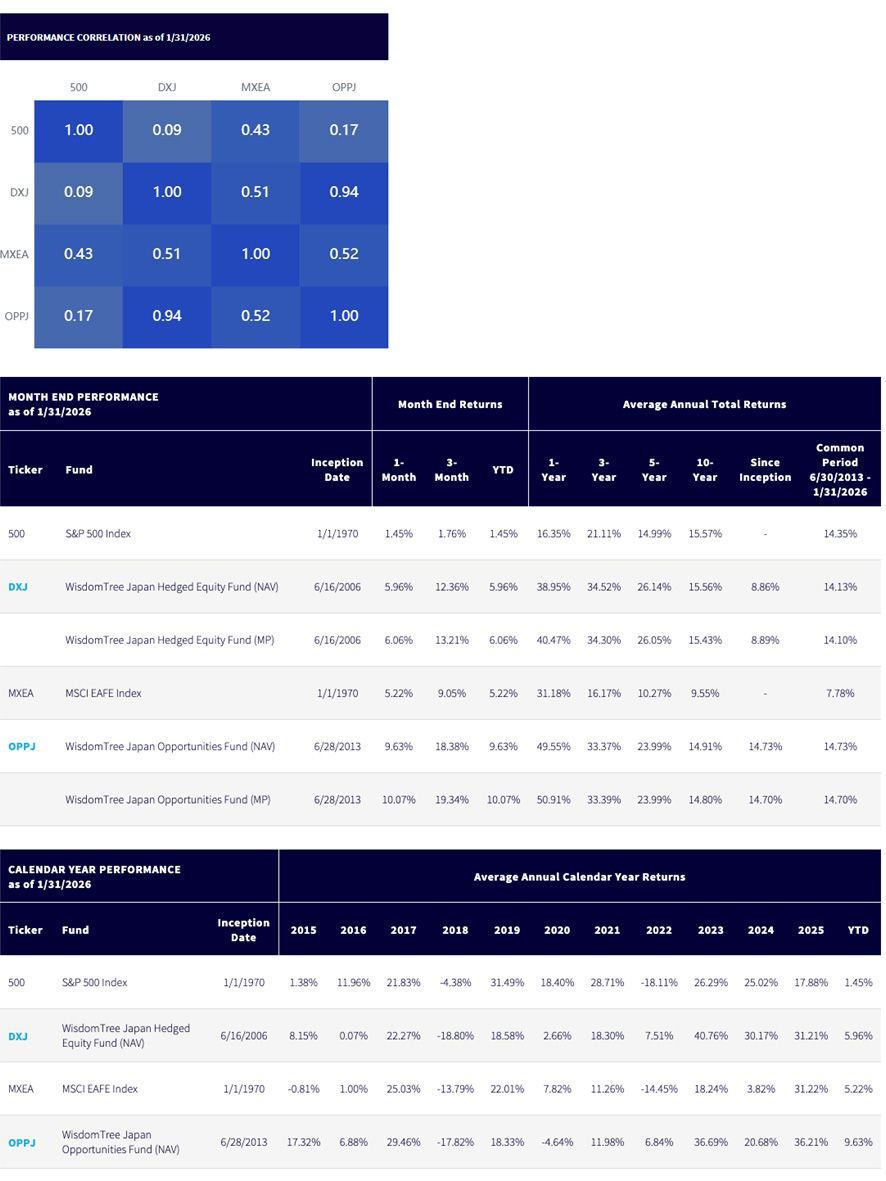

Correlation data highlights how differently Japanese equities have historically behaved relative to U.S. large cap—notably DXJ and OPPJ had a very low correlation with U.S. equities—showing how they can add diversifying properties to a portfolio.

Source: WisdomTree Fund Comparison Tool, as of 1/31/26. Past performance is not indicative of future results. You cannot invest directly in an index. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: DXJ, OPPJ.

Calendar Year Returns

Japanese equities have also demonstrated competitive or less severe downside characteristics relative to U.S. large caps over the past decade—note the 2022 downside markets when the S&P 500 sold off and Japanese funds performed positively that year—showing that low correlation property.

The worst calendar year for the U.S. markets over the last decade was in 2022 when the S&P 500 declined -18%. Japan's worst year was in 2018 when it also declined 18-19%.

Currency effects can materially shape long-term outcomes. Japan offers a clear example of how currency exposure can alter investor returns over time.

A currency-hedged approach allows investors to focus on equity fundamentals rather than the yen's path. When interest rate differentials are wide, hedging can also generate positive carry, meaning investors are compensated for neutralizing currency risk.

This is not a forecast about the yen's direction. It is a recognition that currency is a separate risk factor. For many U.S.-based investors, hedging the yen has historically reduced volatility and improved the clarity of the Japan equity exposure.

Investors looking to express the Japan thesis have several implementation paths within WisdomTree's lineup.

From a portfolio construction perspective, Japan can serve as a strategic overweight within the international sleeve. For example, in a portfolio allocating 20 percent to international equities, investors may consider maintaining 10 to 15 percent in broad developed exposure and allocating 5 to 10 percent directly to Japan. This structure preserves diversification while leaning into a market that offers differentiated valuation and correlation characteristics.

Japan's investment case today is not about short-term headlines. It is about a market that combines attractive valuations, improving domestic momentum, structural tailwinds from technology and reform and meaningful diversification benefits.

For investors facing elevated U.S. valuations and a compressed equity risk premium, Japan stands out as a differentiated global opportunity. A disciplined, portfolio-aware approach to implementation can help investors position for what may be a durable shift in global leadership.

DXJ: There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

OPPJ: There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund's prospectus for specific details regarding the Fund's risk profile.

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.