EPI

India Earnings Fund

Published May 6, 2025

Global Head of Research

Macro Strategist, Model Portfolios

When Suzuki entered India in 1982, it didn't just launch a car company—it helped write the first chapter of a new industrial story. In partnership with the Indian government, it formed Maruti Udyog, a modest joint venture that would eventually become Maruti Suzuki—now a market titan controlling roughly half of India's passenger vehicle market. Four decades later, Suzuki's India bet hasn't just paid off; it has redefined the center of gravity for the company. India isn't a growth market for Suzuki—it's the market, its largest globally.

And Suzuki isn't alone. Hitachi, long known for cooling and refrigeration in India's sweltering summers, has quietly pivoted into the software space through its acquisition of GlobalLogic—marking a deeper integration into India's booming IT sector. Sharp and Casio have carved out their own lanes in consumer electronics and appliances.

But the real connective tissue often goes unnoticed: the Japanese trading houses—Mitsubishi, Mitsui, Sumitomo, Itochu—the very firms Warren Buffett has quietly been accumulating. These conglomerates don't shout, but they shape. They've helped fund and coordinate ventures in specialty chemicals, steel and infrastructure—like Nippon Steel's partnership with Tata Steel. Meanwhile, in transport, Hitachi and Mitsubishi Heavy Industries are bringing Japanese precision to India's rapidly expanding rail and metro systems.

Today, Japanese firms aren't just manufacturing or building infrastructure in India—they're branching into the digital, the logistical and even the agricultural. Rakuten has set up R&D hubs, signaling Japan's ambitions in e-commerce and digital services. Yamato Transport, Japan's logistics heavyweight, is forming alliances that hint at a deeper supply chain integration. Japanese breweries are entering the Indian market, while trading giants like Mitsui are deploying capital into the backbone of agriculture—cold storage, distribution networks and farm-to-market systems.

What began as a focused presence in autos and electronics has evolved into a broad-spectrum strategy. The Japanese playbook in India is no longer sector-specific; it's ecosystem-wide. This is what long-term commitment looks like—starting with a beachhead and then quietly compounding into something far more expansive.

This isn't just economics—it's alignment by design. As the Indo-Pacific takes center stage in global geopolitics, India and Japan find themselves not just trading partners but strategic complements. Both see the value in a stable, open, rules-based regional order—and both recognize the need for balance as China's assertiveness grows more visible.

What's emerging is a kind of strategic flywheel: shared security interests deepen trust, that trust fuels more investment, and that investment tightens the partnership further. It's diplomacy powered by economics—and economics shaped by geopolitics. The result is a relationship that's no longer reactive but compounding.

One of the clearest signals of this deepening alignment is the Quadrilateral Security Dialogue—the Quad—linking Japan, India, the U.S. and Australia. It's often framed as a geopolitical counterweight, but beneath the surface, it's also an economic architecture in the making. The Quad is about securing supply chains, shaping technology standards and building infrastructure outside the gravitational pull of Chinese capital.

For India and Japan, it has unlocked a new level of coordination—across 5G, semiconductors and other strategic technologies. The trust built at the top—among heads of state and national security advisors—filters down to boardrooms and R&D labs. In sectors like telecom and AI, Japanese and Indian firms are now forming partnerships not just because it makes business sense but because the geopolitical foundation is aligned. When governments are in sync on trusted networks and supply chain resilience, it becomes easier for companies to move fast—and move together.

Another key piece of the puzzle is the Supply Chain Resilience Initiative (SCRI), launched by Japan, India and Australia as a direct response to the hard lessons of the pandemic and the systemic risks of overdependence on China. On the surface, it's a policy agreement—but in practice, it's a strategy to rewire the plumbing of global trade.

The idea is simple: combine complementary strengths to build a more shock-resistant Indo-Pacific. Japan brings capital and manufacturing precision. India offers scale and labor depth. Australia adds raw materials and geographic balance. Together, they're creating new pathways—investment forums, policy alignment, even cross-country supplier matchmaking—to shift critical links in the supply chain away from single-country exposure.

For India, this means an influx of manufacturing investment. For Japan and Australia, it means a more diversified and dependable supply base. The SCRI isn't just a hedge—it's a new operating model for regional trade built on shared strategic logic.

Behind the headlines, a quiet architecture has been taking shape. Since 2006, the "India-Japan Strategic and Global Partnership"—upgraded in 2014 to "Special Strategic and Global Partnership"—has built a durable institutional framework: 2+2 ministerial dialogues, annual leadership summits and deep-working groups focused on everything from defense to trade. This scaffolding keeps the relationship on track even as governments and global conditions change.

But it's not just pageantry. Political alignment at the top has real-world spillovers—accelerated approvals for Japanese industrial zones, yen-denominated loans to cushion currency risks and smoother regulatory pathways for joint ventures. It's diplomacy that translates directly into lowered friction and faster execution.

The bigger picture? India and Japan are not just cooperating—they're synchronizing. Security and economics are no longer separate lanes; they're running in parallel. In a world where geopolitical alignment increasingly dictates economic opportunity, this partnership stands as one of the clearest examples of that convergence in action.

What's unfolding between India and Japan isn't just bilateral trade—it's a blueprint for strategic convergence in the 21st century. By investing in each other, Japan and India are co-authoring a vision for regional stability and shared prosperity—one that deliberately moves beyond the gravitational pull of any single dominant power.

Japan's approach—long-term, patient and embedded—has earned it more than just economic returns. It has bought influence, credibility and a seat at the table of India's rise. This isn't extractive capital; it's participatory. Japan doesn't just sell to India—it builds with India, hires locally and co-develops infrastructure that endures.

For Japan, India represents a democratic, if messy, hedge against geopolitical concentration—a youthful, fast-growing market with immense upside. For India, Japan is proof that global partnerships can be high-trust, high-impact and long-term.

The India-Japan story is what it looks like when strategic intent aligns with economic substance. It shows how resilient capital, layered with geopolitical foresight, can reshape not just economies but the very architecture of the Indo-Pacific. With the groundwork laid, the next chapter could move faster than the last. The compounding has already begun.

India andJapan as Investment Options

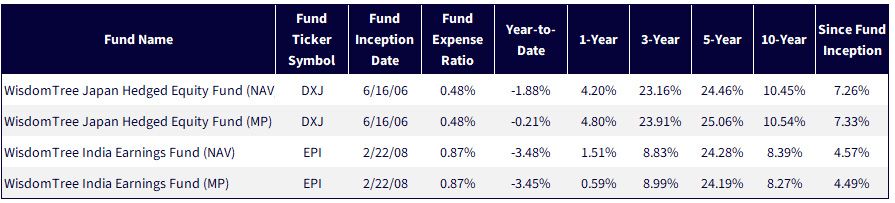

To contextualize the aforementioned ideas, it's worthwhile to take an investment exposure to Japanese export-oriented companies like the WisdomTree Japan Hedged Equity Fund (DXJ) and compare it to an investment exposure to broad-based, profitable companies across India with the WisdomTree India Earnings Fund (EPI).

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 4/10/25, but showing returns for the period ended 3/31/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: DXJ, EPI.

From a high level, the intuition regarding Japan is that it is a highly educated, technologically advanced society, but one that has a slow-growth timbre and a demographic quite advanced in age. India is largely the opposite—a younger population seeking to become more and more technologically advanced as the country with the largest overall population in the world.

Figure 2: 3-Year Returns Stood Out

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 4/30/25, but showing returns for the period ended 4/29/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performances and to download the respective Fund prospectuses, click the relevant ticker: DXJ, EPI.

A perennial issue with India is that people get excited about its prospects and expect things. The narrative of a "young, highly educated population" is repeated time and again, and the economic growth statistics in the range of 5%–6% get people who are used to 1%–2% growth in developed markets quite excited. This pushes equity valuations for India's market higher.

Japan, on the other hand, is known as the slow-growth, economic laggard in many respects. Even if we can cite facts and statistics where this simply isn't true, it creates an advantage for Japan's equities in that they can quietly maintain a lower valuation.

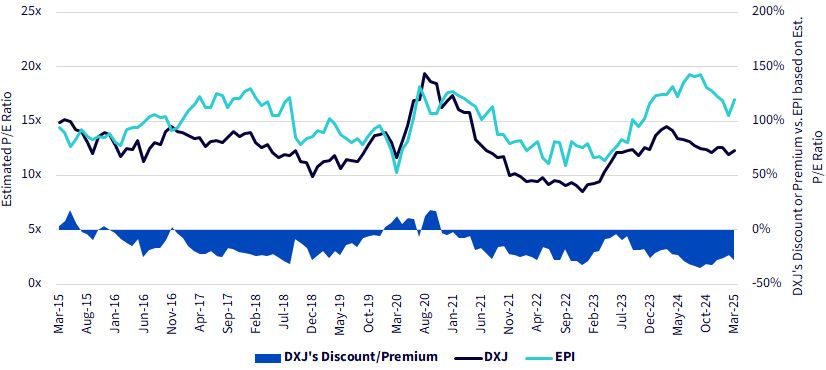

We can see in figure 3:

Figure 3: 10Years of Valuation History (DXJ vs. EPI)

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 4/10/25. Past performance is not indicative of future results.

True, the majority of Japan's revenues are not coming from India, but if Japan's companies are leaning into the India growth story AND there are avenues to access the equities at a 25%–30% discount on certain measures, Japanese equities, exemplified through DXJ, may be quite worthy of consideration for those looking at how the Asia story could evolve from 2025 to 2030.

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. As these Funds have a high concentration in some sectors, the Funds can be adversely affected by changes in those sectors. Due to the investment strategy of these Funds, they may make higher capital gain distributions than other ETFs. Please read the Funds’ prospectuses for specific details regarding the Funds’ risk profiles.

DXJ: The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and may be less liquid than other securities and more sensitive to the effect of varied economic conditions.

EPI: This Fund focuses its investments in India, thereby increasing the impact of events and developments associated with the region that can adversely affect performance. Investments in emerging, offshore or frontier markets such as India are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments.

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.