US Dollar trifecta: inflation, elections, policy

Published 20 June 2018

Christopher Gannatti, CFA

Global Head of Research

As we seek to understand movements of the US dollar, we’ve noticed that there are three major factors that come up time and again:

- Inflation

- Elections

- Policy

Let’s evaluate each of these in turn1.

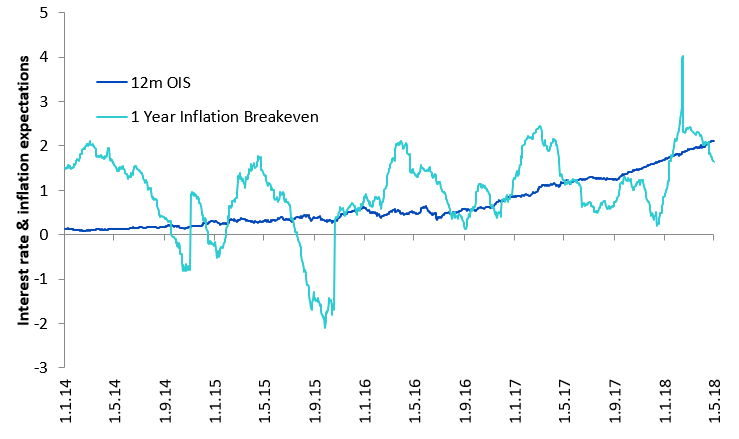

Rising inflation can push US Dollar towards weakness

Figure 1: Interest rate and inflation expectations

Sources: Bloomberg, Record, 31 March 2014 to 2 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Monitoring the picture of US inflation using market-oriented gauges like this is of great value because it can help us look even beyond the US Dollar towards a toolkit of investments that might respond in a rising inflation environment. Stocks with growing dividends are of interest, as are other real assets, like commodities, which can see their prices rise as somewhat of an inflation hedge.

US Dollar positioning has indicated disappointment with President Trump

Figure 2: Citi FX Positioning Alert Indicator (PAIN) index: USD positioning

Sources: Citi, Macrobond, Record, 29 December 2015 to 29 December 2017.

Past performance is not indicative of future results. You cannot invest directly in an Index.

The election and inauguration of President Trump saw great enthusiasm amongst dollar bulls that positioned themselves with lots of long US Dollar exposure. The basis of this view was that the new administration would have the potential to extend the natural growth cycle, doing things like tax cuts and infrastructure spending late in the economic cycle.

With the benefit of hindsight, we now know that even with Republican control in both the legislative and executive branches of the US government, it was far from easy to implement a tax bill. An infrastructure spending policy remains to be seen as of this writing. This manifested itself in many dollar bulls becoming bearish, dramatically reducing their long-US Dollar positions. At times people have characterized the dollar weakness of 2017 as flow-related—this is a good gauge to provide evidence to that view.

Macron election opened the door to euro strength

Figure 3: EUR/USD 3-month implied volatility

Sources: Bloomberg, Record, 30 Jun. 2016 to 29 Dec. 2017.

Past performance is not indicative of future results. You cannot invest directly in an Index.

One of the most influential (and in 2017 most surprising) currency pairs was the euro vs. the US Dollar. The biggest story in the first part of 2017—especially after President Trump’s election victory—was the so-called “Populist Uprising”. For markets, the most significant embodiment of that was Marine Le Pen. Her loss to Emmanuel Macron allowed investors to become a lot more comfortable with holding long-euro positions, as it was feared that a Le Pen victory would be a major turning of the tide towards euro skepticism.

The euro-US Dollar 3-month implied volatility behavior does indicate a substantial lowering of implied risk in this exchange rate, the catalyst for which was the French election. During elections through the rest of 2017, the market never quite placed the same level of risk in the concept of euro skepticism, and one could think of this as removing an impediment to euro strength, as opposed to anything specifically related to dollar weakness.

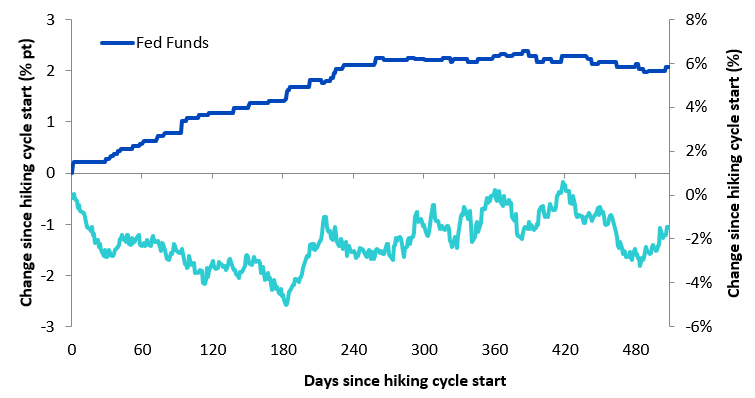

Do investors have the concept of Central Bank policy divergence incorrect?

Figure 4: USD Index during hiking cycles

Sources: Bloomberg, Record. Average of past five hiking cycles (1986 to 88, 1988 to 90, 1994 to 96, 1999 to 2001, 2004 to 06).

Past performance is not indicative of future results. You cannot invest directly in an Index.

Capital flows towards higher relative interest rates and pushes up the value of higher interest rate currencies relative to lower interest rate currencies, right? In theory yes, but in practice like many aspects of thinking about currency movements, it’s not that simple. Here, we look at the average of the past five interest rate hiking cycles at the US Federal Reserve. In general, these policy shifts have been more likely, at least historically speaking, to be accompanied by a weaker dollar than a stronger one.

An explanation of the phenomenon, especially valid in today’s markets, is that the Fed tends to communicate its intended path of policy, not wanting to spook markets. As a result, when then Fed Chairman Benjamin Bernanke started talking about tapering quantitative easing purchases in May of 2013, global markets reacted in a way that we now reference as the Taper Tantrum. Broad based dollar appreciation followed. When we began 2017 or 2018, in contrast, market participants broadly have a baseline of several expected policy hikes, and the surprise would only occur in the other direction.

When thinking about central banks, we must start from a standpoint of what might surprise markets with new information, rather than an expected widely anticipated environment of policy divergence.

Considerations for 2018 & beyond

It will be important to continue monitoring these different factors, thinking about the potential for surprises. Will weaker economic data out of the Eurozone inspire further easy monetary policy from the ECB? Are there political risks in Europe, perhaps from Italian political scenario, that cause questions about the euro area? Will US inflation surprise to the upside significantly? The answers to these types of questions, in our view, will have the potential to shift the tides in currency markets much more than what we all know and expect today.

Categories

Related articles

The world's biggest market is hiding in plain sight

Beijing Without Breakthroughs: What the Trump–Xi Summit Means for Investors

Equity Outlook catching the tailwinds respecting the headwinds

How the Iran War Is Reshaping the Macro Outlook

Geopolitics is rewiring the strategic metals and rare earth miners

Rolls-Royce, Safran, and Airbus at the centre of Europe’s defence tech future

Japanese equities embrace Takaichi victory

Inside the WisdomTree Strategic Metals and Rare Earths Miners Index rebalance

What’s Hot: What if Greenland risks were to re-escalate?

About the contributor

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.