Strange bedfellows: What can investors expect from Italy’s odd coalition?

Published 19 June 2018

Global Head of Research

Populism strikes again. Incensed at the state of the nation, half of voters in Italy’s recent general election opted for the two largest protest parties. Five Star Movement (5SM) took 32% of the vote, while the League surged from fringe status to take 18%. Despite their conflicting views, the parties have formed a coalition government. What can investors expect from Italy’s strange bedfellows?

Meet the partners

5SM’s left-wing economic views are unnerving markets. Indeed, the party’s rise appears to have one reason Italian equities have underperformed European and US stocks over the last five years1. And while the League may be nominally right-wing – its anti-immigration stance certainly justifies that label – its economic policies largely overlap with those of 5SM.

The coalition is founded on a series of leftist economic measures, such as scrapping a 2011 law that increased retirement ages to reflect demographic trends. Let’s put this in context: this is happening in an economy with a debt-to-GDP ratio of 131.9% in 2017, according to the International Monetary Fund, at a time when extending the working life of seniors is a priority from Japan to Canada.

Trouble ahead?

The coalition’s plans are likely to exacerbate Italy’s spending habit – at 50.2%, according to International Monetary Fund as of December 2017. Italy’s government spending-to-GDP ratio is the seventh-highest worldwide – and do little to alleviate the challenge of raising tax revenue from an anaemic national economy.

Alongside concerns about Italy’s public finances, there are fears that popular uneasiness could spill over into street protests and perhaps violence.

A potential parallel currency

A key concern for bond markets is a potential plan to issue mini-BOTs, a proposed new type of short-maturity debt aimed at raising money for the state. Because holders of mini-BOTs could use them to purchase state services and conduct various other financial transactions, the notes could become a de facto parallel currency, alongside the Euro. One imagines the EUR/USD exchange rate would not take kindly to their introduction.

Combined with fuzzier European economic data of late, bond-market concern about mini-BOTs may lead the European Central Bank (ECB) to delay scrapping its €30 billion-per-month bond-purchase program, which is due to expire in September. There are views on both sides of this issue presently, so it’s something we’ll be watching in earnest over the summer for signals of greater clarify from President Draghi and the ECB.

Three ideas for investors

Owing to ECB bond buying, Italian sovereign yields have thus far not provided much compensation for heightened political risk. But we are seeing signs of stress in several areas, including:

- Select European government debt markets, including Italy.

- Credit default swap spreads on Italian and Spanish banks; however, they remain well below the peak levels of the past five years.

- The Euro, which depreciated by 3.19% in May 2018. We see potential for further falls.

Against this unsettled backdrop, investors need to be on their guard. Below, we discuss three ideas that we think merit consideration.

1) Hedging currency risk

The risk most likely to reverberate across international investors’ portfolios is unhedged Euro exposure. Those investors not based in Euros may mitigate a source of risk in their portfolios if the Euro depreciates further. On the other hand, those investors based in Euros may seek an incremental source of return through holding a portion of their European equities in US dollars.

2) Focus on European exporters

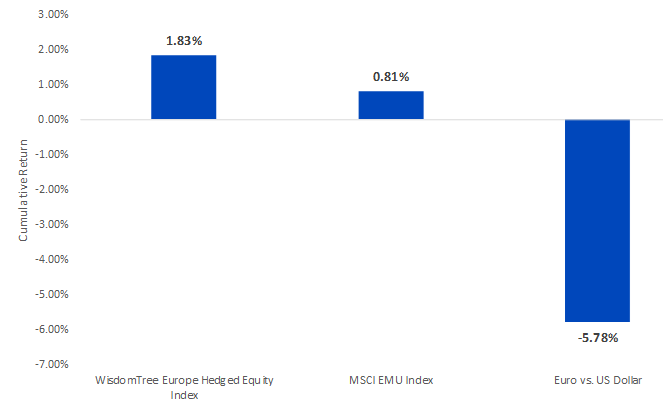

For all the concern about events in Italy, global economic growth remains robust – for now, anyway. We think this makes European businesses that sell most of their goods and services outside of Europe particularly interesting. They represent an intriguing way to potentially gain exposure to globally diversified companies.

The WisdomTree Europe Hedged Equity Index – which comprises export-oriented companies; to be included, constituents must derive over 50% of their revenue from outside Europe – was essentially flat in May. Figure 1 compares its performance to that of the unhedged MSCI EMU Index, which fell 5.52%, largely due to currency moves.

Figure 1: Exporters amidst Italian uncertainty

Source: Bloomberg. Period is from 18 April 2018 to 1 June 2018. You cannot invest directly in an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

3) Target quality

Another concept we have advocated for turbulent times is having exposure to companies with stronger balance sheets. Figure 2 shows the performance of the WisdomTree Eurozone Quality Dividend Growth Index, which is weighted toward such companies. It delivered a +2.9% return in May, versus -1.29% for the MSCI EMU Index. The difference in cumulative return between the two benchmarks year-to-date is almost 5 percentage points.

Source: Bloomberg. Data from 31 December 2017 to 29 May 2018. You cannot invest directly in an index.

Historical performance is not an indication of future performance and any investments may go down in value

Uncertain future

It is far from clear how the situation in Italy will play out over the medium to long term, even though there is now a new government. Given the uncertainty, we think that hedging Euro exposures, focusing on export-oriented European businesses, and targeting higher-quality companies are concepts worth considering.

For those concerned what Italy’s ruling coalition might do next, we would make a final observation. 5SM and the League toppled the mainstream parties against an economic backdrop that, while lacklustre by international standards, is about as robust as anything Italy has experienced for some time. Investors might regard the coalition’s current plans as economically retrograde, but they should ask themselves this: what fiscal and/or monetary policies might voters demand if economic conditions deteriorate?

Related blogs:

+ Euro depreciation: the key to unlocking value in European exporters

1 MSCI Italy, MSCI Europe, S&P 500, 5/29/2013 – 5/29/2018. Source: WisdomTree, Bloomberg.

Related products

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.