Trade tariffs tinker with metals outlook

Published 18 June 2018

Uncertainty around trade tensions are back to the fore again. The Trump administration has confirmed it will not extend the exemptions on US tariffs that were imposed on Canada, Mexico and the EU. Now that the US tariffs on steel and aluminium products are in effect, we are likely to see retaliatory tariffs on US imports by the EU and Canada. Furthermore, it looks like the recent victory of trade agreements between the world’s two largest economies on 22 May was short-lived. Despite several trade relaxations by China, Trump has announced that tariffs and investment restrictions on China will be formalised on June 15 and 30 respectively. We believe Trump’s more aggressive stance was in retaliation to the domestic criticism he has received on being too lenient towards China recently. So far, the extent on interruption seems contained since the steel and aluminium tariffs account for less than 2% of US imports and an even smaller portion is affected since countries including Australia remain exempted. Added to that, US$50bn of Chinese imports equate to less than 2% of US imports. From a historical standpoint, the current trade wars are of a much lower magnitude in comparison to the 1929 or 1971 tariff hikes that reached 20% and 10% respectively. Although the metal tariffs cover a narrow range of imports so far, the real threat for financial markets is that a tit-for-tat spiral could widen the scope and magnitude of products and imperil global growth.

Sentiment clouds strong fundamental of base metals

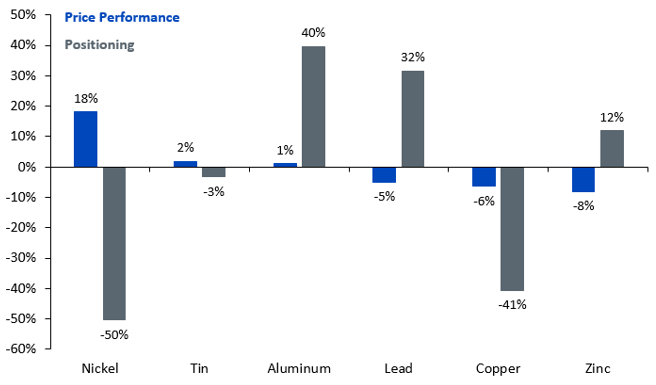

US trade announcements are rattling industrial metal markets evident from the shift in sentiment. Aluminium prices were amongst the largest beneficiaries, soaring 26%, marking a 7-year high since the announcement on April 6th of US sanctions against Russia. Fears of supply disruption were exacerbated when two of the world’s largest miners – Glencore and Rio Tinto declared force majeure on some of their aluminium contracts in Russia. The sanctions on Russian aluminium producer Rusal had a large part to play in nickel’s upward price momentum. Despite the unlikelihood of sanctions being imposed on Russian nickel producers, the anticipation of tightening supply helped trigger a substantial build-up of speculative long positioning of nickel futures.

Figure 1: Performance vs Sentiment

Source: Bloomberg, WisdomTree, Commodity and Futures Trading Commission (CFTC), London Metal Exchange (LME), data available as of close 31 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Fundamentals of base metals remain positive

While performance of the industrial metals complex has so far been subdued in 2018, we still believe fundamentals remain intact for most metals. And given their procyclical nature, industrial metals stand to benefit, as we enter the late phase of the expansion cycle.

In the case of nickel, the outlook for the global nickel market remains upbeat as the global supply deficit has been revised higher in 2018 by the International Nickel Study Group (INSG). Despite a 7% increase in supply owing to higher nickel pig iron production in China and Indonesia, the increased supply will continue to lag demand. INSG has revised its demand outlook higher owing to increased usage from stainless steel (the largest nickel consumer) and battery technology.

Copper is expected to post a moderate supply surplus of 43,000 tons in 2018 for the first time in nine years according to the International Copper Study Group (ICSG). We believe the ICSG has discounted the likelihood of any supply disruptions this year. Extension of the collective agreements at Escondida mine are up for renewal mid-year and preliminary talks so far have led nowhere. Last year, strikes at this mine caused a sizeable supply outage on the copper market. Added to that, this week the Tamil- Nadu state government in India has ordered closure of Vedanta’s 400kt Sterlite copper smelter, owing to environmental concerns. While it is uncertain if the closure is permanent, the absence of the Sterlite smelter jeopardises 1.7% of global copper supply. This alone can swing the market back in a deficit in 2018. On the demand side, ICSG expects demand to grow by 3%, driven by infrastructure development in China and India. While recent activity data in China has been mixed, China’s official Purchasing Managers Index rose to an eight-month high of 51.9 in May, signalling continued expansion.

In the case of aluminium, now that US tariffs imports are in effect, we expect further supply disruptions to keep the aluminium market on tender hooks. A market that was seen to be permanently in surplus last year is now likely to face deficits.

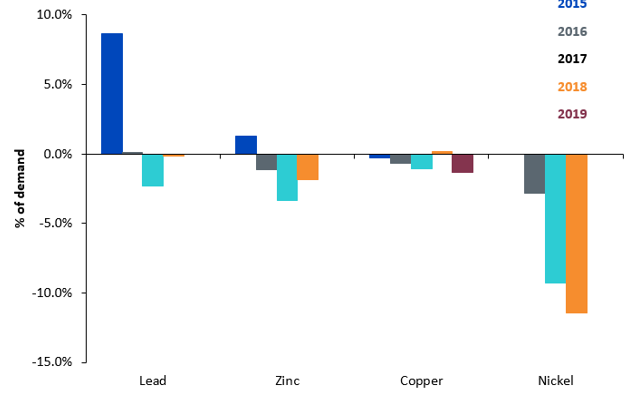

According to the latest assessments by the International Lead and Zinc Study Group (ILZSG), the zinc market is to remain in a deficit in 2018, albeit lower than last year’s deficit (evident from the chart above) owing to pro-cyclical increase in supply. Meanwhile, the supply deficit on the lead market is expected to be considerably lower in comparison to the previous year owing to a ramp up in production in both mines and smelters. Demand is forecasted to rise by 2.7% this year, with demand from batteries accounting for its highest usage despite the emergence of alternative technologies.

Figure 2: Metals supply in a deficit

Source: ICSG, INSG, ILZSG, WisdomTree, data available as of close 30 May 2018.

Past performance is not indicative of future results. You cannot invest directly in an Index.

Conclusion

The fundamental story for the industrial metals market remains intact. While more supply is coming on stream, as producers take advantage of higher prices, most metal markets continue to remain in a supply deficit. While we expect the tariff trade wars to keep volatility elevated among metals, we remain constructive on the long term growth story for industrial metals.

Categories

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.