ECB strikes a balance between the doves and hawks

Published 22 June 2018

Projecting an unbiased political stance

President Mario Draghi took a bold stance at the European Central Bank (ECB) press conference on 14 June. It appears that Draghi has found the perfect balance for the hawks (scale back its net asset purchases) and doves (lower rates for longer). Not only did Draghi announce the timeframe for ending the asset purchase programme in 2018 but he also provided forward guidance on the unlikelihood of an interest rate hike until the summer of next year, subject to incoming data. Taking into consideration the occurrence of the meeting comes just weeks after the Italian political turmoil, it is likely that Draghi was trying to project the most politically unbiased stance of the ECB to the markets by ending an era of easy money. Most analysts expected forward guidance language on rates to only come at the December meeting. The ECB provided it earlier. In addition, the projected timeframe for the next rate hike is longer than investors had originally expected. The timing of the end of the stimulus triggered speculation on when the ECB will raise rates. According to the Eonia-dated contracts, it now appears more likely that the first-rate hike won’t take place until September 2019, provided inflation is sustainable. This is close to the time that Mario Draghi retires from his current position in October 2019. The market is becoming convinced this is a slight dovish set of policy changes. This sentiment is in sharp contrast to the more hawkish sentiment signalled by the Federal reserve interest rate decision in the US to raise interest rates four times this year and a further two to three times in 2019. We expect the sharp divergence of rate expectations to weigh on the Euro versus the US Dollar.

Figure 1: 1 day % return following ECB market reaction

Source: Bloomberg, WisdomTree, data available as of close 15 June 2018. You cannot invest directly in an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

Rising inflation underpins ECB plan to taper

As the ECB’s mandate remains focussed on price stability, it shrugged off a series of downbeat macroeconomic data in the euro area and contagion spreading from Italian political risks. Instead it drew attention to the sustained adjustment in the path of inflation as the core reason for ending its bond buying program. According to the latest staff projections for GDP, growth was revised lower for this year, while the outlook for 2019 and 2020 remain upbeat. While the inflation outlook was lifted higher to 1.7% from 1.4% each year until 2020. It seemed contradictory that the ECB remained optimistic on the forward growth projections despite central bank staff projections for 2018 being lowered to 2.1% versus 2.4%. It is also worth noting that the committee was unanimous in its decision to alter forward guidance should things change, and Draghi confirmed there was a desire to retain optionality should conditions deteriorate.

Figure 2: Approaching Inflation target - ECB aims to keep inflation below but close to 2% in the medium term

Source: Eurostat, Bloomberg, WisdomTree, data available as of close 15 June 2018. You cannot invest directly in an Index.

Historical performance is not an indication of future performance and any investments may go down in value.

Hedged European equities may offer an attractive advantage to benchmark indices

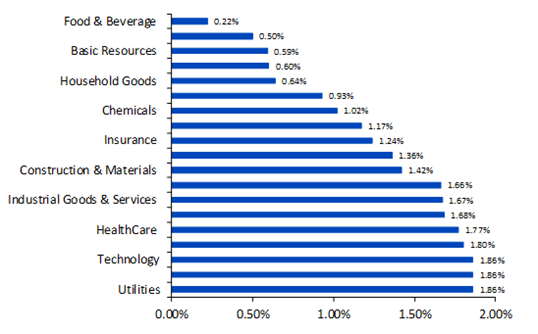

The dovish undertone coupled with greater clarity from the ECB on the interest rate path ahead seemed to resonate across the markets. The Euro dipped 1% while European equity markets closed higher by 1.23% and bond yields in Germany, Italy and Spain declined 0.45%, 2.78% and 1.35% respectively (as of 14 June 2018). After being caught in the crossfire of trade wars during the first five months of 2018, European exporters such as the automakers that caught a tailwind from the declining Euro posted among the strongest gains on the European equity markets after the ECB meeting. While we remain constructive on the Euro area, we caution investors to remain selective while allocating towards the Euro area and perhaps consider hedged European equities.

You may also be interested in reading:

+ How to hedge European fixed income amidst the ECB’s QE tapering

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.