SOYB LN

WisdomTree Soybeans

Published 10 November 2025

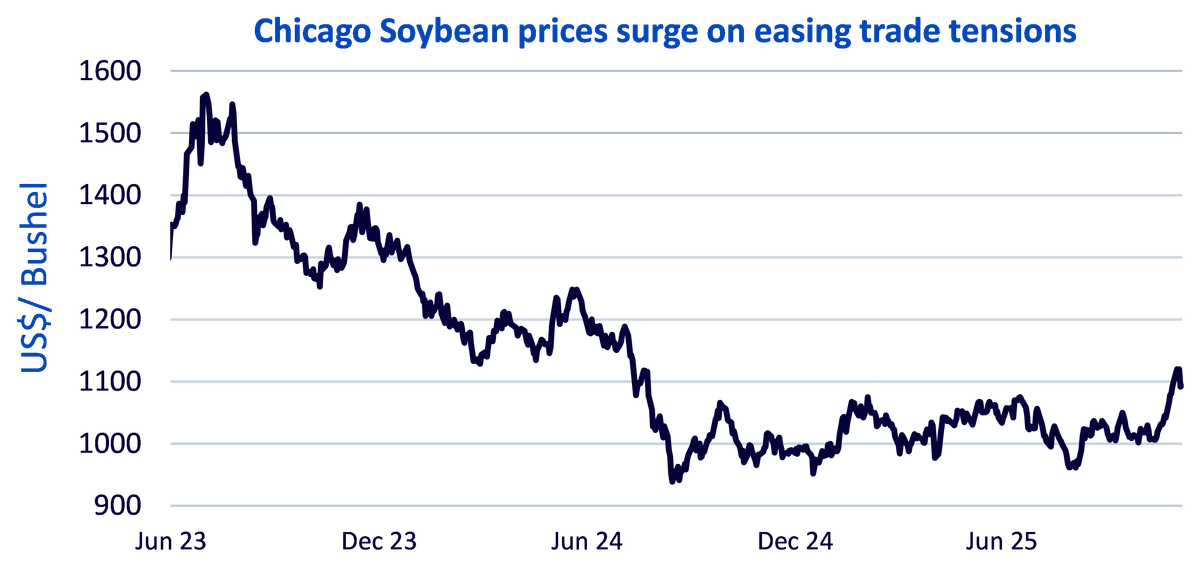

President Trump hailed his trade deal with China’s Xi Jinping to be a triumph: a “12” out of 10. The one-year extension of US-China trade truce agreed by President Trump and President Xi provided near term relief to markets. Signals from both capitals suggest a willingness to de-escalate tensions.

The White House announced pledges of cooperation on fentanyl, increased purchases of soybeans and more importantly, a one-year pause on new export controls on rare earth metals, magnets and processing technology. China, in turn, said it would remove retaliatory tariffs on selected US farm products1 while the US offered tariff relief and removed thousands of companies from blacklists. China earned tariff relief and the removal of thousands of companies from US backlists. Both sides also suspended port fees on ships made or owned by the other.

Chinese buyers had shunned US soybeans since Trump’s first trade war, leaning more on top producer Brazil to meet demand. China bought at least four more US soybean cargoes following a summit between President Trump and China’s Xi Jinping, offering some relief to American farmers2. The US administration said that China agreed to buy 12mn tons of soybeans between now and January with a further commitment to purchase at least 25mn annually over the next three years. Soybean futures notched their biggest monthly gain at 11.8%3 in almost five years as Beijing moved to boost purchases of American farm goods following a trade truce.

Source: Bloomberg, WisdomTree as of 7 November 2025. Historical performance is not an indication of future performance and any investments may go down in value.

While supportive, the headline numbers bear closer scrutiny. In the years before the trade war, Chinese annual imports of US soybeans routinely ran as high as 25-30mn metric tons or more. Thus, the 12mn ton commitment for the remainder of 2025 represents a dramatic reduction – about 32% lower than last year’s volumes, and the softest since 2018. From January 2026, the annual target rises to 25mn tons, which restores US sales to pre-tariff levels but not higher.

According to customs authority data, China's soybean imports from the US in December 2024 and January 2025 amounted to 4.3mn and 4.9mn tons, respectively. These volumes are difficult to achieve, as China has probably largely covered seasonal needs with soybeans from Brazil. However, state-owned buyers could procure additional US cargoes to rebuild reserves. Traders estimate the potential for this at around 8mn tons. Much will now depend on the details of the trade agreement, whether China will commit to purchasing US soybeans, as it did in the Phase 1 agreement at the beginning of 20204.

Brazil and Argentina—the two chief competitors to US soybean exporters continue to capture Chinese demand with cheaper and more accessible supply. Even as China renews some US purchases, Brazilian beans have been preferred for immediate shipment due to price and logistics advantages. For US farmers, the improved outlook may encourage farmers to hold beans hoping for a price rebound while others focus on the expanding role of domestic processing for biofuels and animal feed.

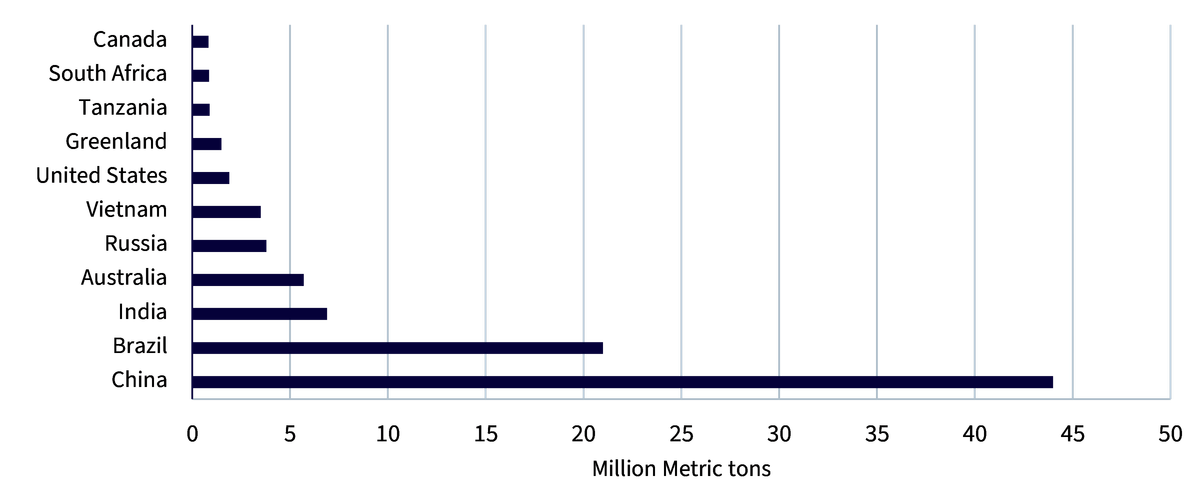

The one-year pause on new export controls for rare earths, magnets and processing technology reduces near-term policy tail risk but does not reverse the multi-year trend toward supply‑chain diversification and onshoring outside China. China’s entrenched dominance in rare earth mining, separation, and processing has become a central geopolitical risk.

Source: US Geological Survey as of January 2025. Note: Data for Myanmar, Madagascar, Malaysia and Nigeria are not available. Historical performance is not an indication of future performance and any investments may go down in value.

The allied response is accelerating, with the US, Australia and Japan co-investing to expand separation capacity, heavy rare-earth processing, magnet production and gallium refining. The US-Japan partnership announced earlier this year, adds significant momentum to building high purity processing and magnet making capabilities outside China, leveraging Japan’s technical expertise and the US’s financial support. These assets have long commissioning times which means near-term leverage still sits with China’s refining and magnet ecosystem, even as non-Chinese supply chains scale.

For investors, these developments change the role that rare earths and strategic metals can play. The sector isn’t simply a cyclical bet on global growth. It is a structural allocation to supply security, industrial policy and technological adoption. Electric vehicles, industrial automation, air conditioning, robotics and offshore wind all add to magnet demand, while data centres and grid build–out raise the call on strategic metals and rare earths.

The WisdomTree Strategic Metals and Rare Earths Miners UCITS ETF (Ticker: RARE) is positioned to capture both the build-out of Western supply chains and the current reality of Chinese dominance through its diversified exposure across metals, geographies, and value-chain segments. RARE provides rules-based exposure across the Energy Transition Metals Value Chain, rather than a single-metal bet. The index maps ten metal categories including aluminium, copper, lithium, nickel and rare earth elements, and spans six subsectors from mining to refining, smelting, chemicals, conversion, and industry. Our collaboration with Wood Mackenzie helps us attribute revenues along the value chain and to the underlying metals, which improves purity of exposure and clarity in client conversations about where bottlenecks and margins are likely to sit.

The US–China truce is a relief valve, not a reset. Soybean purchases should support sentiment but are bounded by Brazil’s competitiveness and by targets that merely return volumes to the lower end of pre-tariff norms. In critical materials, a pause on new controls trims near-term volatility but leaves the structural re-wiring of supply chains firmly in place.

1 Ministry of Finance of the People’s Republic of China as of 5 November 2025

2 Bloomberg as of 31 October 2025

3 Bloomberg, as of 1 November 2025

4 Reuters as of 5 November 2025

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.