WDEF LN

WisdomTree Europe Defence UCITS ETF - EUR Acc

Published 6 November 2025

Senior Associate, Quantitative Research and Multi Asset Solutions

Headlines about geopolitical tensions have moved from abstract to immediate, and Europe’s defence posture has reset accordingly. Since 2022, threats have shifted from theory to the front line and uncertainty around US posture has reinforced the case for greater European self-reliance. Rising budgets, renewed stockpiles and accelerating investment are powering an explicitly Europe-centred rearmament and industrial expansion cycle.

Investor interest has followed. Defence-themed ETFs have attracted over $10 billion1 of inflows year to date as allocators seek targeted exposure to the theme. The key test for investors is finding an exchange-traded fund (ETF) that delivers pure exposure to Europe’s rearmament, built around European companies and weighted by the factors that drive defence demand.

In the sections that follow, we show why a Europe-focused scope matters, how ‘Europe’ labels can mask very different portfolio definitions, how the WisdomTree Europe Defence ETF’s revenue-tilted design aims to create purer exposure than market-cap peers, and why its liquidity makes it efficient to hold.

Global defence ETFs are built to capture the average of a worldwide theme, not the centre of Europe’s rearmament. By design, they include large US primes and Asia-Pacific names whose demand cycles, budget dynamics, and programme timelines differ from those in Europe. That broad reach pulls portfolio weight away from European companies and away from revenues earned in Europe - the pulse of the continent’s procurement and capacity build-out.

Europe’s rearmament is a region-specific cycle, but most global defence ETFs are constructed around market capitalisation across regions, which naturally concentrates exposure in the largest US primes. That is not Europe’s demand centre and it underweights European primes and suppliers more directly levered to European procurement, ammunition replenishment, missile defence and industrial scaling. Even when global funds hold European companies, their weights are relatively low.

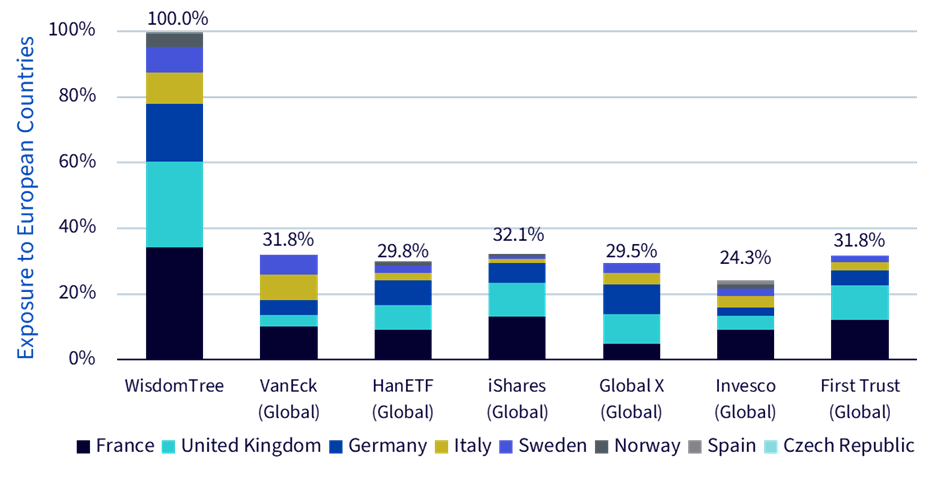

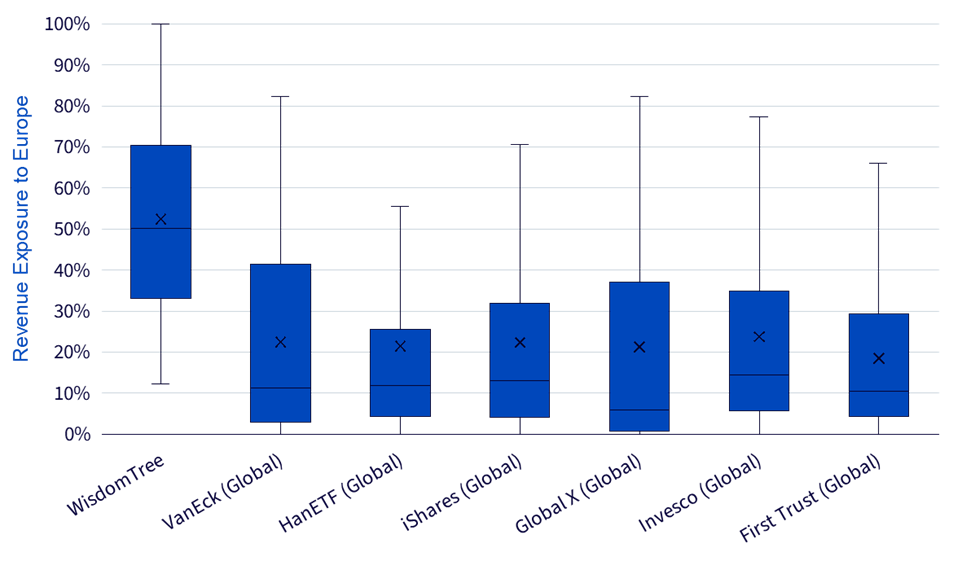

WDEF takes the opposite approach, restricting the universe to companies domiciled in Europe only. That scope choice leads, mechanically, to a heavier focus on European players and a higher share of revenues linked to European customers than other global defence ETFs. As Figure 1a shows, major global defence ETFs only allocate roughly 24–32% to European-domiciled companies. This, in turn, results in around 50% median revenue exposure to Europe for WDEF, which is significantly higher than the typical 10–15% of global strategies (Figure 1b). Global ETFs dilute Europe’s defence story. WDEF keeps it intact by concentrating both portfolio weight and revenue exposure within Europe.

Within a clean Europe-only universe, how you weight holdings determines the purity of the exposure. Plain market-cap methods favour the biggest constituents, which are not always the most tied to defence activity. WDEF incorporates defence revenue into construction, tilting weights toward companies more directly linked to defence spending. Eligible companies are assigned exposure scores based on revenue exposure to defence activities: Score 3 (>50%), Score 2 (25–50%) and Score 1 (10–25%). Higher scores receive greater emphasis, subject to liquidity and risk constraints.

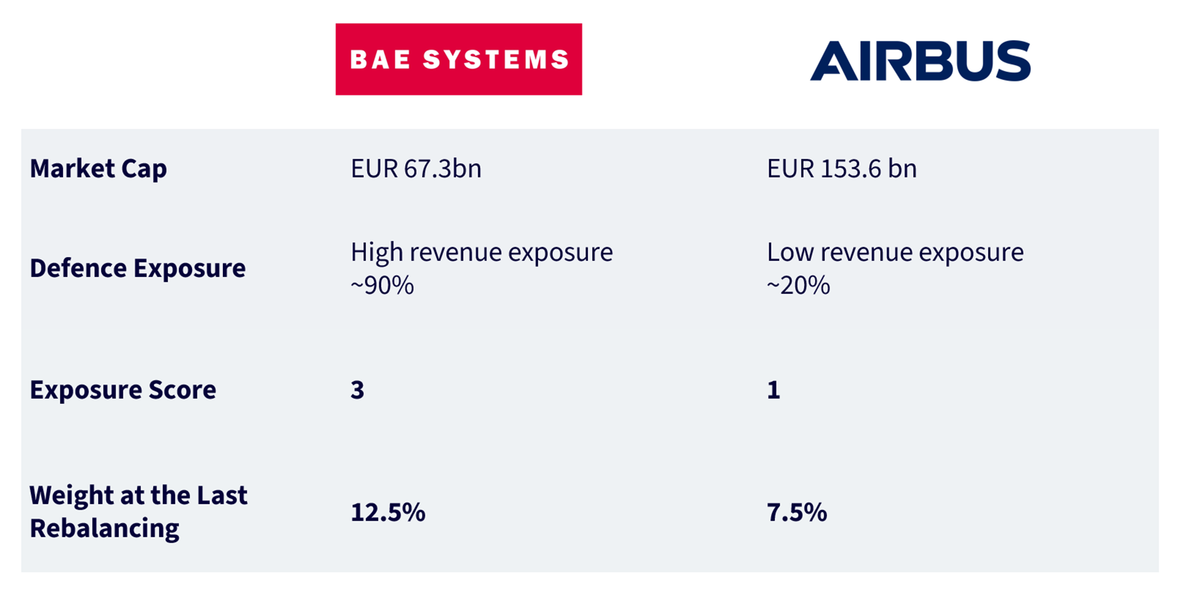

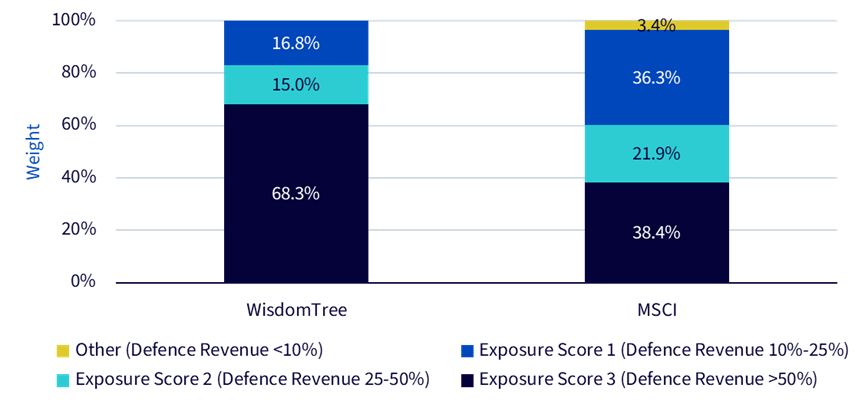

This design choice matters in practice. Consider Airbus and BAE Systems. Airbus has the larger market capitalisation but a broader civil aerospace mix and BAE Systems has a higher share of defence revenues. A cap-weighted aerospace and defence benchmark will tend to skew toward Airbus, while a revenue-aware approach places greater emphasis on BAE Systems and similar high-intensity names, lifting the portfolio’s thematic purity. As shown in Figure 2b (using the MSCI Europe Aerospace and Defence Index as a reference), Score 3 names account for around 68% of WDEF versus about 38% in a cap-weighted index.

At the group level, higher-score cohorts have shown relatively stronger sales growth and performance, supporting the case for a revenue-aware tilt (Figure 3). There remains a strategic role for lower-score names such as Airbus or Rolls-Royce. These firms supply propulsion, subsystems and services central to Europe’s rearmament; they offer liquidity and diversification, and their civil exposure can dampen programme-specific risk. The tilt does not exclude these companies; it reweights toward the pure-play part of the theme, aiming to align more closely with Europe’s defence cycle and its growth opportunities.

Exposure score | Median Sales growth | Median 1-yr total return |

|---|---|---|

3 | 16.3% | 80% |

2 | 9.6% | 43% |

1 | 5.1% | 54% |

Products with ‘Europe defence’ in the name can still reach outside Europe. Some strategies permit allocations to non-European companies in Turkey, South Korea, or Australia, for example, allowing the portfolio to hold companies such as Aselsan, whose revenues are predominantly domestic (87% from Turkey). If the goal is to align with Europe’s rearmament narrative, these inclusions dilute the signal: the demand centre, procurement priorities and budget execution are Europe-centric.

Funding support is another factor. EU initiatives such as the European Defence Fund (EDF), which promotes joint R&D and capability development, and the European Defence Industry Reinforcement through Common Procurement Act (EDIRPA), focused on joint procurement, both aim to scale Europe’s defence industrial base and can directly or indirectly benefit European companies. These programmes are intended primarily for EU-based recipients, meaning non-EU issuers are less likely to benefit directly from this policy support. In short, scope choices are not semantic; they map to the policy plumbing behind Europe’s cycle.

Good thematic design still needs good implementation. Execution costs matter as much as management fees in an ETF. Two factors drive the ‘all-in’ cost of trading: the quoted bid-ask spread and the depth available, both on-exchange and via the primary market (creations/redemptions). WDEF shows a quoted spread of 5.4 bps, the tightest in the set. On turnover, WDEF’s 1-month average daily volume is $12.82m, far ahead of the group. That combination, including tight spreads and materially higher on-screen activity, suggests greater capacity for block trades without significant price impact, which helps keep total trading costs in check even for larger tickets.

Europe’s defence rearmament is a multi-year, Europe-centred story. Suppose the objective is to capture that specific cycle - scope and weighting both matter. WDEF starts with a European issuer universe and a clear preference for European end-demand, mitigating the ‘label risk’ that blurs the theme. It then tilts by defence-revenue intensity so that exposure follows the drivers of the cycle, not just the biggest tickers. Finally, it seeks to deliver that purity in an ETF wrapper that is practical to own, with tight spreads and solid trading depth. For investors seeking a targeted sleeve that aligns with Europe’s evolving security priorities, WDEF could offer a pure-play, rules-based route into the theme.

1Source: WisdomTree European thematic monthly update, September 2025.

WisdomTree Europe Defence UCITS ETF - EUR Acc

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).